The Curve: Flying Blind?

Holiday week disruptions and the lack of major data inputs before the Dec 9-10 FOMC meeting keep the odds of a cut in a wide range.

The countdown to the Dec 9-10 FOMC action will have minimal inputs from payrolls and CPI as the decisions get made, so this will make for interesting color from the SEP report and dot plot and how Powell explains the group’s forecasts. The street is still swinging the bat to come up with estimates and the FOMC will be no different.

Unlike Trump, who never met a number he would not ignore, the employment and inflation forecasts will be especially interesting in the SEP.

The UST rally this past week rewarded bonds with all 7 bond ETFs we track generating positive returns and the same for the running YTD bond ETF returns. Life gets trickier from here with no CPI and payroll data updates for October and the macro release schedules remaining light and uncertain. CPI and Payroll cover the dual mandate, so that makes for a challenging task.

The material swings in FedWatch odds the past two weeks underscores the array of questions on potential FOMC action on Dec 9-10 and into early 2026. As we go to print, FedWatch was back up to 85.1% after being in the low 40% handles last week after a 90+% range last month.

With Black Friday ahead and various shades of black and dark gray for other days, the retail color from the industry might help. Headlines are pointing at strong expectations. The past week gave mixed news on overall consumer patterns with WMT, TJX, TGT, and HD reporting. We would score the color from those leaders on the “net favorable” side of constructive with some hedged qualifiers for the low-end shopper.

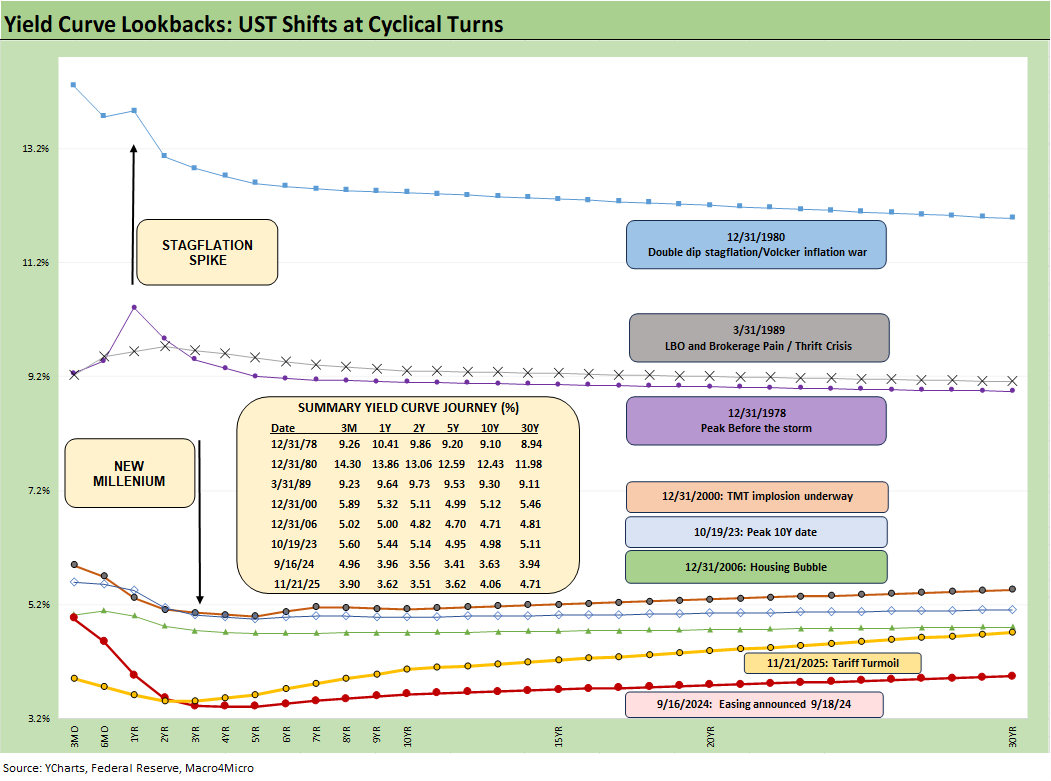

NOTE: The chart above and those that follow update our rolling review on the state of yields. We break some sections into two parts: “Recent Trends” and “Historical Context.” The historical context is more about background, memory joggers, and for new readers. The recent trends is a quick summary of the recent UST action.

Recent Trends:

The past week saw all 7 bond ETFs in positive return range (see Market Commentary: Asset Returns 11-23-25). Mortgages remain stubborn while FedWatch odds keep gyrating. At last check, FedWatch was just over 85%. In last week’s commentary, FedWatch had dropped from over 94% (10-27) to 62% and then to 45% in last week’s edition.

Data starvation remains a major challenge, and we are not sure the White House minds. CPI and Payroll will not be available for the FOMC, and we also await the 3Q25 GDP line items with the latest Personal Consumption Expenditures and GPDI Investment lines. Many data points have been MIA since August data releases with the Sept CPI and payroll the most important of the limited information so far.

We already looked at the payroll data (see Employment Sept 2025: In Data We Trust 11-20-25, Payrolls Sep25: Into the Weeds 11-20-25) and the Sept inflation data (see Simplifying the Affordability Question 11-11-25, CPI September 2025: Headline Up, Core Down 10-24-25). The signals are not clear so far as to how payroll and lagging price action from tariffs are working into the system. That takes time, but a few months of impaired vision is the reality. You certainly cannot listen to the qualitative hype from the White House.

Historical Context:

The above chart overall helps give historical context to the level and shape of the current yield curve vs. a range of market backdrops. Historical perspective always helps. The curves are plotted across some historical economic expansions and in some cases pending turns in the economic and/or monetary cycle. They are worth pondering for compare-and-contrast purposes since they mark key transition points in cycles and market risk backdrops. In some cases, the timelines include bouts of dulled risk senses and occasional valuation excess (notably 1989, 2000, 2006).

Monetary cycles, credit cycles, and economic cycles are not always on the same wavelength. The 1980-1982 double dip was a painful restructuring of the US industrial sector, but the credit markets were very underdeveloped. We have seen multiple credit cycles across the timeline from the 1980s implode-a-thon after the 1989 peak of the credit markets on through the other timelines detailed.

The tech bubble of 1999-2000 saw a default spike and market plunge but set against the most muted recession across the decades. The systemic crisis of 2008 drove the worst (and longest) economic downturn since the Great Depression. In this current market, it is much easier to see low growth and modest stagflation than a sharp recession. The tariffs and extremely poor budget governance do not help.

Highlights across monetary journey…

The last time a stagflation threat had to be considered was after the Carter inversion of 1978 indicated above. The stagflation threat then showed up in force by the Dec 1980 curve after a peak Misery Index of 22% in June 1980 and Volcker was in full swing trying to break inflation.

Another useful period to ponder is the TMT cycle faltering in 2000 on the way to a massive Greenspan easing in 2001. The current cyclical tech boom and valuations cannot escape looking back at the late 1990s. That period saw credit markets under pressure in 1999 and creeping up on 6% HY default rates, but that did not stop the NASDAQ from printing an 86% total return year in 1999 on the way to a March 2000 peak (see UST Curve History: Credit Cycle Peaks 10-12-22, Greenspan’s Last Hurrah: His Wild Finish Before the Crisis 10-30-22, Yield Curve Lookbacks: UST Shifts at Cyclical Turns 10-16-23).

The late 1990s period offers another case study in excess across equity and credit markets with the peak in 1999 (credit) and NASDAQ (2000). The TMT bubble bursting soon led to excessive easing by Greenspan in 2001 and then into early 2004, in turn setting the table for the housing bubble peak in 2006. During the 2004 to 2007 period, leveraged derivative exposure and structured credit was out of control and counterparty risk was soaring. The good news is that currently the credit markets and banking/dealer systems are sound unlike 1999 and 2007.

Private credit and rating agencies “working hard for the money” will bring some scrutiny, but the investors still face the obvious obligation to conduct their due diligence. As an analyst who started in private placements at Prudential in the early 1980s, there was plenty of focus on due diligence and covenant structure. Many of those analysts on the “privates” team migrated to HY bond business lines.

The current credit cycle is getting gut-checked right now despite the very low default rate expectations. “Private Credit” as a concept thus is not new but is traveling a different structural path now with new participants and AUM gathering. The lack of transparency leads many to assume the worst on marks, but the main asset gatherers/originators do include some of the best credit people in the business. Some will flunk the “revenue maximization vs. prudence and diligence test” but most will do fine.

The private credit players want the market to grow (by trillions) and being extra vigilant about it in due diligence now makes more sense than not. Assuming a cockroach festival still seems like extrapolation run amok. As always, there will be dogs and likely some ticks. That is intrinsic to the process.

Passing across the distortion years…

The chart above jumps from 2006 to 2023, which takes the market beyond the crisis period and the ZIRP years and COVID. Both the post-credit crisis period and later COVID crisis prompted the Fed to deliver a wave of market liquidity support and confidence building programs that helped save the capital markets, reopened the credit markets, reduced refinancing risk anxiety, and reduced the contingent liquidity risk profile of the banks.

The credit crisis period from late 2008 to COVID in 2020 brought plenty of QE and normalization distortions to the yield curve shape. The Fed’s dual mandate made that possible. The market could soon face new legislative threats to the Fed in 2026 that seek to reel in the dual mandate. In addition, the new “Fed head” in 2026 is likely to do whatever Trump demands. That topic of sweeping regulatory change at the Fed is based on commentary from Bessent and mirrors plans discussed in Project 2025 (see Chapter 24). That will be a topic to tackle as we get closer to those ideas coming into play.

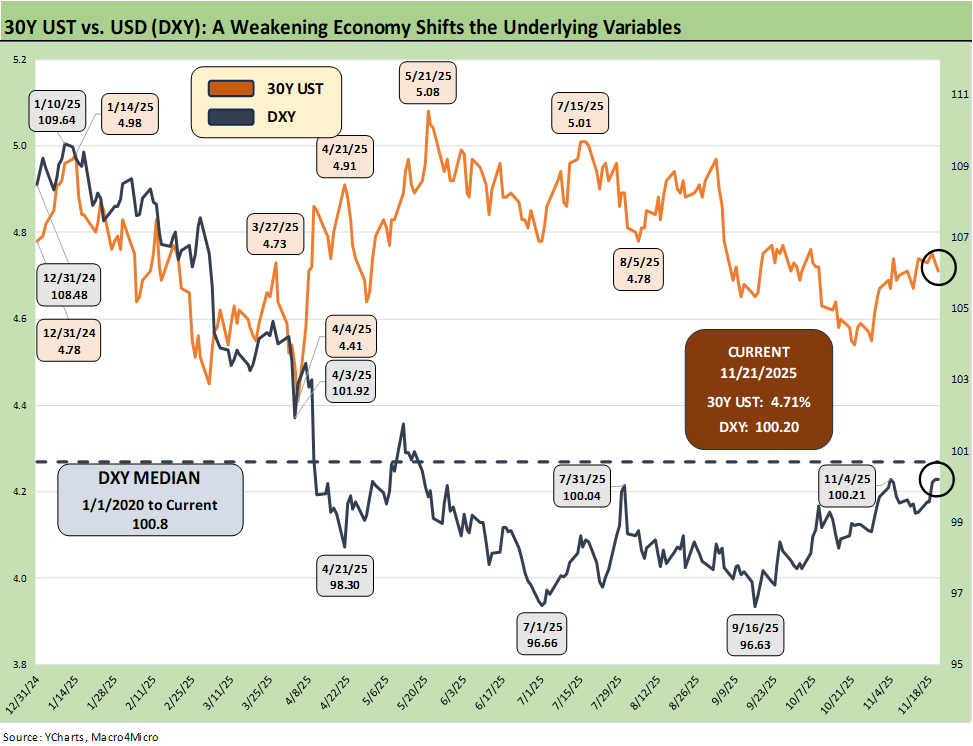

Recent Trends:

The above chart plots the recent trends in the 30Y UST vs. the dollar index (DXY) as the US dollar weakness throws another risk variable into the picture and poses a major risk factor for non-US buyers of UST.

This past week saw the dollar index (DXY) strengthen to 100.2 from 99.27. Lower rates have been a contributing factor to weakening in 2025 as was the continued government shutdown. The end of the shutdown and some balanced macro color in earnings season has supported the dollar. Recent dollar action and commentary are not signaling a hyper easing move yet – at least until Trump gets “his guy” in the Fed seat in the spring of 2026 and more like-minded people in leadership positions.

Inflation trends and a more visible hawkish element in the FOMC are also diluting Trump’s aggression against Powell. This week’s “I’d like to fire his ass” did not elicit much of a reaction since the market does not look to Trump for rational or honest economic commentary – or anything numerical for that matter. The market is also pushing back on the idea that inflation or stagflation does not remain a real threat.

Historical Context:

Team Trump loves to speak of record tariff revenue as if the word “record” makes it a good thing when it comes out of US consumer and corporate pockets. If you want to create a recipe for stagflation, that would be the easiest recipe book to pull from. Just add record deficits and a weaker dollar from the spice rack that makes the tariff even higher at the border. We continue to see very negative color on tariffs from small business trade sources.

Tariffs hit prices or profitability – there is no hiding from the tariff expense paid to customs by the buyer/importer. Resulting expense offsets are likely causing layoffs or slower hiring and potentially reduce expansion by companies who get hit on the cost line. “Tariff cost mitigation” actions are a new part of many earnings calls.

The currency challenge…

The dollar has gone through its worst pounding in 2025 since the 1970s during the dark days of stagflation and multiple deep recessions. Lower rates could be a catalyst for more dollar weakness while political risk factors and governance quality should now be factors in the US sovereign credit quality assessment. The flip side is that rates and inflation metrics may not cooperate with baseline scenarios. In a world where everyone is a borrower, someone has to be the lender.

Record forward-looking deficits and the optics of political instability adds a negative element to the sovereign risk profile of the US that no rating agency would have the courage to flag. The latest assault on free speech and Trump’s threat to arrest people who accuse him of being against free speech is not without its humor and twisted irony (“Call me a fascist and I will arrest you”?!?). Tossing around the Insurrection Act is anything but reassuring to political stability and broader economic confidence. Demanding Federal monitors of select Blue state elections handpicked by Trump is not a Founding Fathers moment. States run election rules – not the White House.

The latest shutdown handily beat Trump’s 2019 record, and the headlines around the Epstein files added to the dysfunction of Washington functionality. The political goal could be to inspire more “Hatfields vs. McCoys” division and “team loyalty” and head off a full and complete release of the Epstein files. “Scrubbing” conspiracy theories are already making the rounds.

The drama can be interpreted as distractions from Epstein with each week looking to further dull the senses. This week was Trump calling for the death of Congressional leaders with 5 of 6 veterans and a mix of Reps and Senators. Hegseth ordered the Pentagon to investigate Senator Mark Kelly – a decorated war hero and astronaut. We suspect there is no truth to the rumor that Hegseth dialed in the order from the “Deus Vult Pub” before heading to the “Wrath of Jesus” tattoo parlor.

Politics, Policy, Economics…

The recent shutdown has been one more case of “politics = policy = economics” as services and payrolls can be decimated. It also blurs performance attribution in framing and evaluating Trump macro policies (notably tariffs). Construction projects get delayed, investments stall, and both federal and private sector payrolls can get hit. To add to the problems, this latest shutdown came at a time when economic data was critical.

With health care costs soaring (notably ACA premiums) and SNAP recipients essentially thrown under the bus during the shutdown, the lower income consumer and subprime quality could be in for a very ugly period ahead. The “K Recovery” could be uglier in the lower section of the “K.”

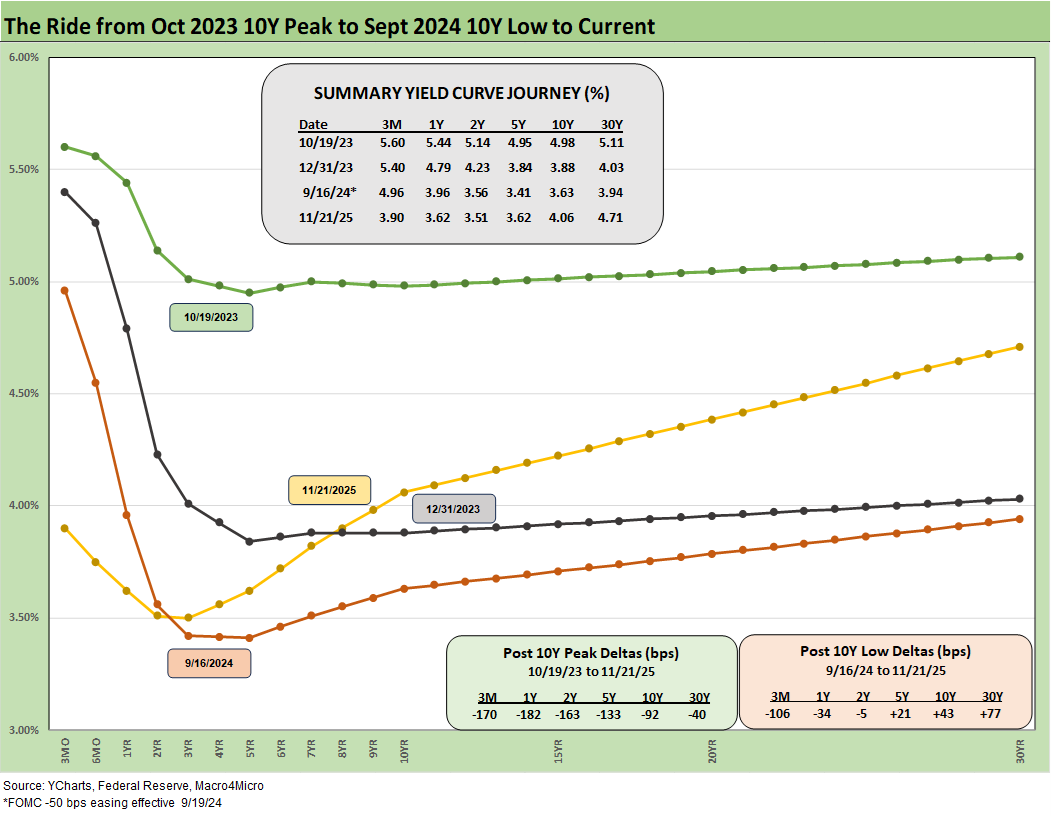

Recent Trends:

The above chart updates the post-easing shift and gives some context to the last major easing in Sept 2024. The current curve has not yet followed the Sept 2024 shift into a bull flattener with the lower fed funds, but we saw some intermittent signs of a rally in the 10Y UST to below the 4.0% line (well above the 3.6% lows of Sept 2024) before the10Y moved higher again across the 4.0% line.

We saw the entire curve move lower this week. The 30Y has held up and declined less across the bull steepening of 2025. The long bond (30Y) chaos in various countries has kept global investors on edge since the supply-demand concerns for UST funding are not going away.

Historical Context:

The above chart frames today’s rates amid the wild ride from the Oct 2023 peak (10Y UST) down across the bull flattener into year-end 2023 and then into the easing actions and rally of Sept 2024. Then came the ensuing bear steepener that is evident in the journey to November 2025. We break out some numerical UST deltas in the box.

Since 2022, we watched the 10Y move from sub-1% across sub-2%, sub 3%, sub 4% and just miss the 5% line. We are now hanging around the 4.0% line with prospects for a record deficit ahead and uncertain inflation with little in the way of useful, distortion-free data.

The UST experience in the period after Sept 2024 and the -50 bps in cuts (followed by another two cuts in 4Q24) will loom large in memory banks. This chart reminds us that the “ease and flatten” shapeshifting pattern is hard to rely on in a market where the supply-demand of UST is tenuous, and tariff impacts are hard to predict.

Fed easing and the flattener vs. steepener debate…

There was a lot of bear steepener action from the end of 2023 into the summer of 2024 and fresh bouts of the same after the big rally in the fall of 2024. The Sept 2024 easing gyrations will make it hard to take much for granted this time after Sept 2025 easing and likely Dec 2025 easing with much higher, sweeping tariff policies and an ongoing debate over a cyclical slowing in the mix of variables. Payroll weakness, slower consumption, and softer demand would help the short end, but the 10Y UST move is more complicated. We still expect 2026 to bring a 3M to 10Y steepener with a lower short end and a stubborn long end.

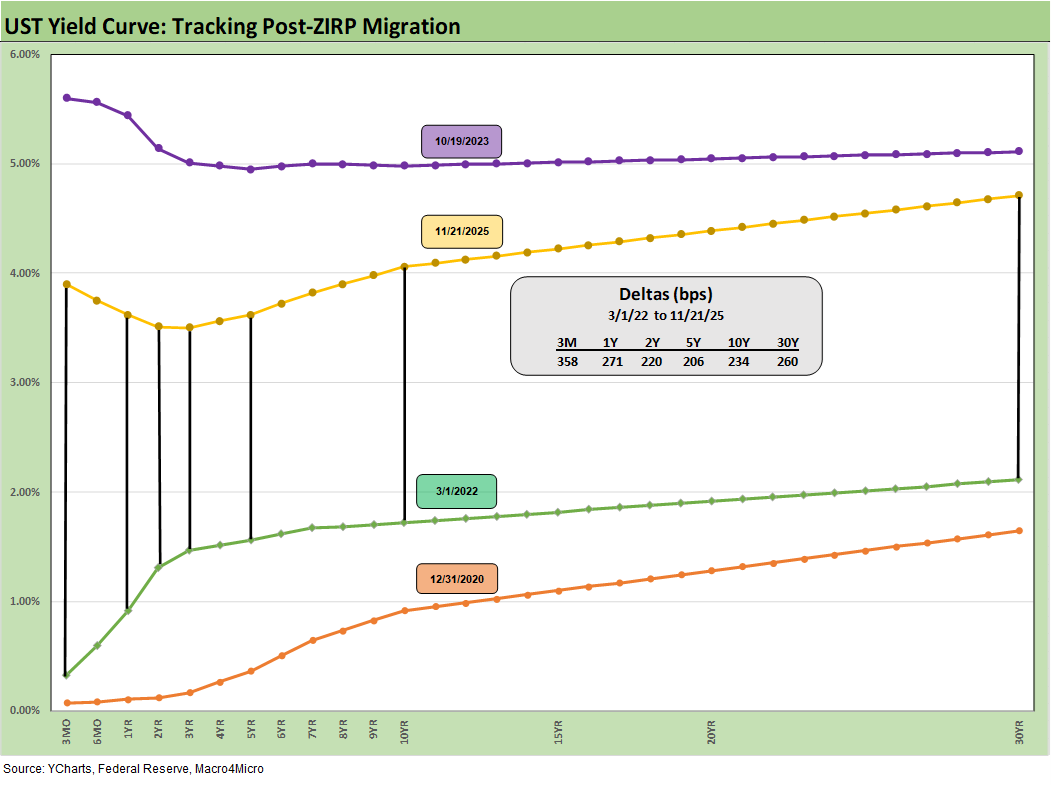

Historical Context:

The above chart just updates where the current UST curve stands relative to the Dec 2020 UST curve on the low end and the 10-19-23 highs after the tightening cycle went into effect in March 2022.

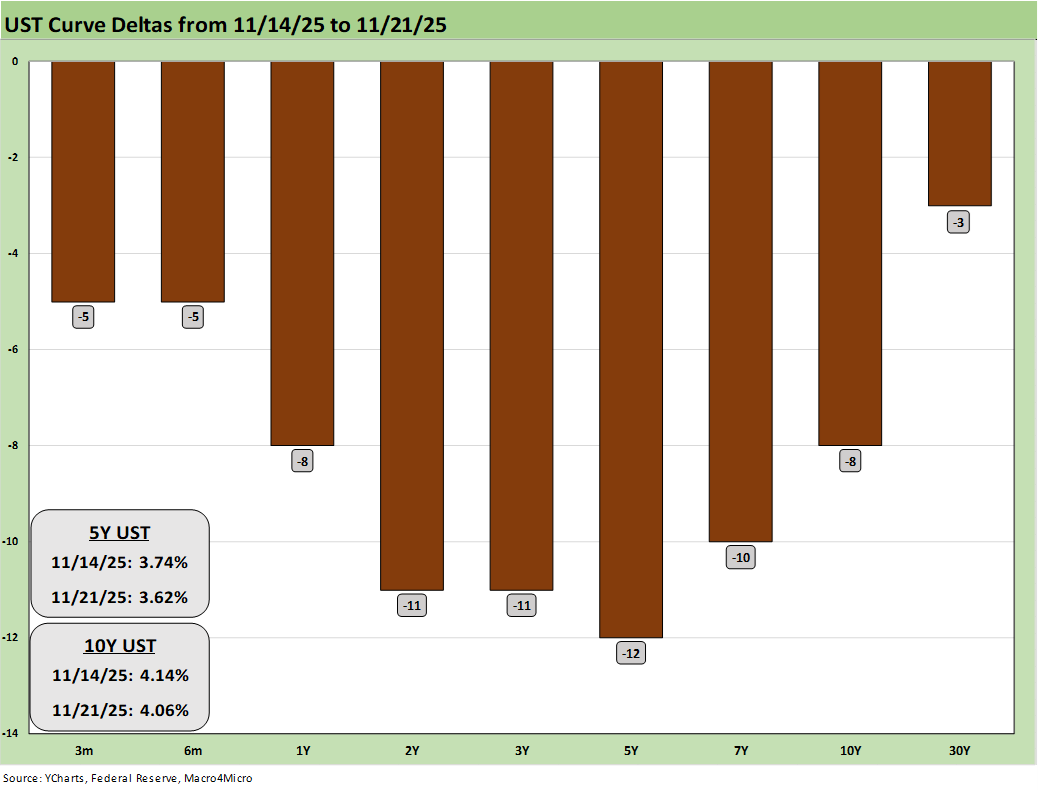

Recent Trends:

The above chart updates the 1-week UST deltas, and we see the UST curve post up a mid-section heavy rally across the UST curve with a muted move in 30Y.

Only time will tell how the lack of macro data and decidedly mixed FOMC will move in the Dec meeting. As discussed above, the plunge in the odds of a Dec 2025 cut last week at FedWatch ahead a of a major bounce-back underscores how small signals can drive rapid shifts in the odds. However, the substance is that the 10Y UST that drives mortgages has been in a very narrow range.

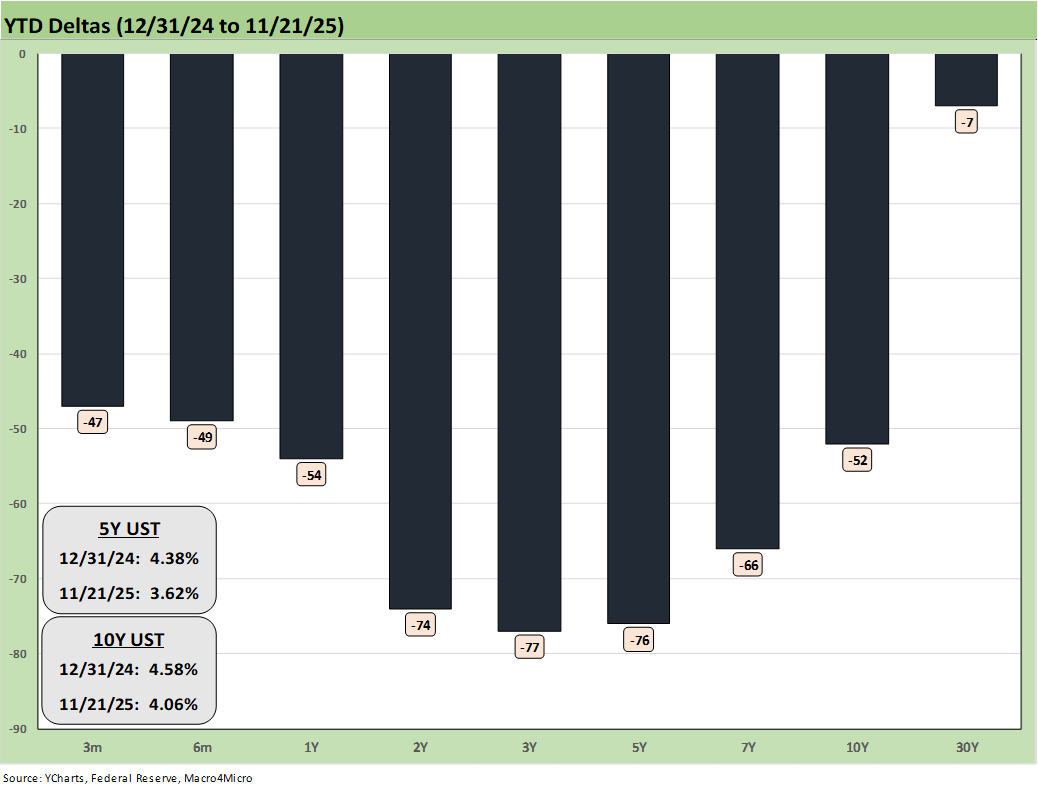

Recent Trends:

The above chart updates the YTD UST deltas. We see how the bull steepener has paid off for bond returns in YTD 2025 with the 7 bond ETFs we track all in positive return range YTD (see Market Commentary: Asset Returns 11-23-25).

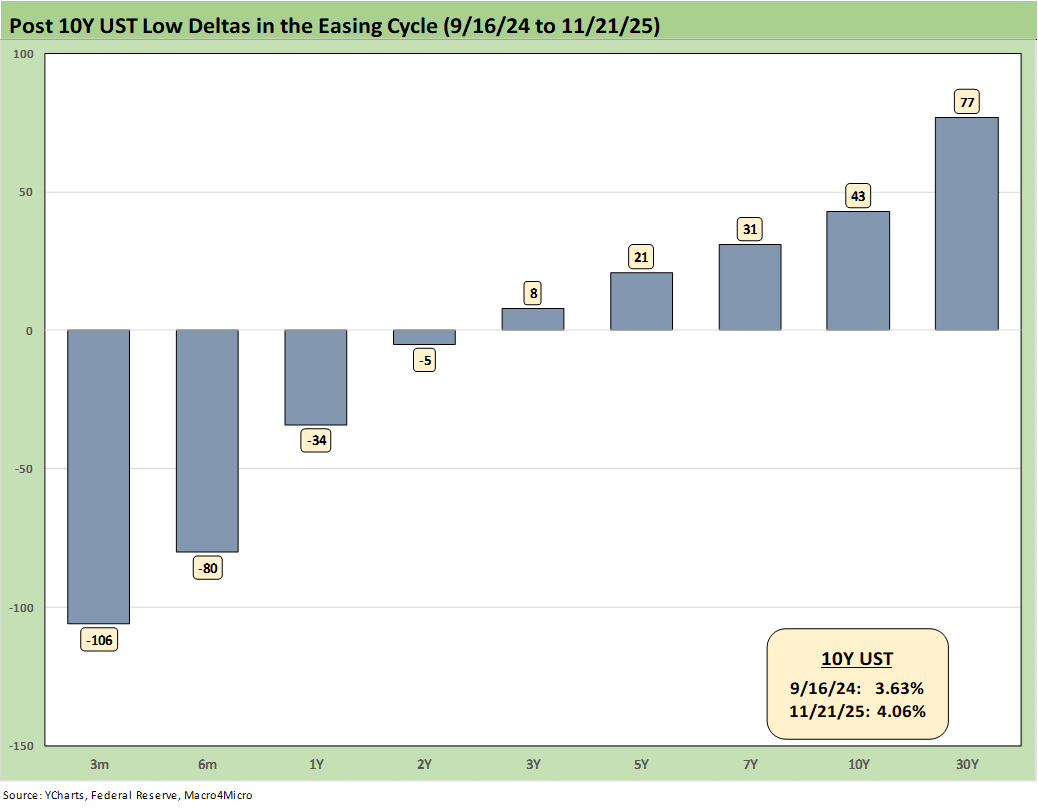

Recent Trends:

The above chart updates the running UST deltas from the recent low point in the post-tightening cycle reached in Sept 2024 (9-16-24) when the 10Y UST (10-19-23) dipped to 3.6% around the first -50 bps easing. At the very least, the 3.6% on 10Y UST (after the Sept 2024 easing) offers some hope to the UST flattening bulls. Of course, that flattening did not last.

The 4.06% from the Friday close (4.03% Monday) again shows the stubbornness of the long end. The expectation of weaker payrolls is still in place with the on-off color from ADP. The Sept payroll numbers were uninspiring and again below median as we have seen every month in 2025 (see Employment Sept 2025: In Data We Trust 11-20-25).

3Q25 earnings did not rattle the fundamental economic story in the large cap corporate sector. The small business sector remains a wildcard in the age of high tariffs, and that requires more data.

Historical context:

The biggest difference between the current backdrop and Sept 2024 is the radically different tariff policies and the slowing GDP growth. There is no question the economy has been posting weaker growth in 2025 than 2024 when getting under the headline numbers. For example, the PCE line in GDP is weaker and so is GPDI. The investment line under GPDI should recover based on the proposed investment “promises.” Those are not in the GDP numbers yet even if investment in IP remains very strong (see 2Q25 GDP Final Estimate: Big Upward Revision 9-25-25). Some 3Q25 GDP data would be helpful at this point.

Lead times on projects vary materially, and a promise from a trade partner is not a contract with the crews ready to break ground. We assume the loosely defined investment promises are subject to market conditions and to final, inked trade deals. As of now, new ironclad and rigorously documented trade deals are lacking with the EU, Mexico, Canada, and China. That is, deals are lacking for the majority of US trade, which is dominated by those four. There are a lot of “frameworks” with the White House. We already saw some hostile commentary recently on the status of the EU framework implementation.

GDP Jedi Mind Tricks…

The recent shift by Team Trump (notably Bessent, Hassett) to emphasize the 2Q25 headline GDP of 3.8% after instructing their audience to ignore the revised 1Q25 headline number of -0.6% as distorted is almost funny.

The key here is to understand how the major tariff-related distortions in net exports/imports and “change in inventories” lines impact the headline GDP number. This is not necessarily intuitive.

Headline GDP for both 1Q25 and 2Q25 is materially distorted by the import line. In 1Q25, higher imports, as part of the pre-tariff import spike and inventory build, generated a -4.7% hit to GDP. In 2Q25, dramatically lower imports generated an additional +5.0% to headline GDP. That +5.0% decline in imports gets netted against a -0.2% decline in exports for a net addition to GDP of +4.8% in 2Q25.

Bessent and Hassett want you to adjust for the negative distortions for 1Q25 to make the number higher. Then they want you to ignore the positive distortions from decreased imports in 2Q25. That is a tad self-serving – and intellectually dishonest.

Beyond the net exports/imports line, the “change in private inventories” is also a major distorting variable. In 1Q25, change in private inventories adds +2.6% to GDP while in 2Q25, it deducts -3.4%. In other words, imports in 2Q25 “artificially” boosted GDP and you can net that +5.0% against -3.4% from inventory.

On a darker note, the huge decline in imports can also be construed as a sharp decline in companies’ low-cost sourcing capabilities and in turn higher expenses. That gets back to the debate of how companies can sustain profit margins via price or alternative cost cutting. Or companies simply can accept lower margins. Nothing comes for free under the laws of economics or double-entry accounting.

If you want to make the case that declining imports, declining exports and lower investment in inventories is a good thing in 2Q25, just don’t bring it up in macroeconomics class or ahead of your bonus review.

Headline GDP numbers are part of the exercise, but the value-added focus should always be first and foremost on the PCE lines and various Fixed Investment lines. That is where the cyclical stories can be found.

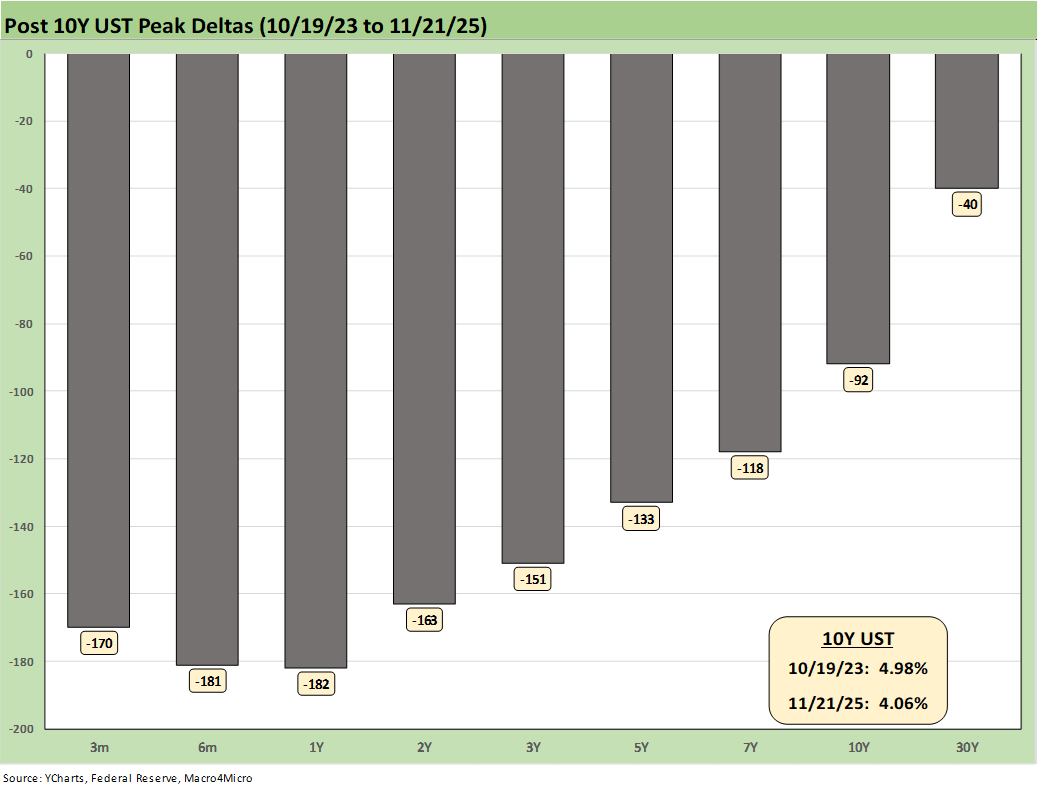

Recent Trends:

The above chart updates the running UST deltas from 10-19-23 through Friday. At the very least, it offers a reminder of what could go wrong if we get adverse inflation outcomes from tariffs. The politics of inflation have always been a death knell for reasonable discussion based on facts (e.g., “seller pays” vs. “buyer pays,” etc.). Trump has signed Executive Orders to eliminate tariffs on a range of products to help lower inflation, effectively admitting that the “buyer pays” and that they’ve been lying (“politically enhancing reality”?) to the American people all along on tariff economic effects.

As we’ve been discussing along the way, the belated Sept CPI numbers underscore stubborn inflation in Services and rising inflation in Goods. The Fed’s 2% target for inflation is almost a full point below where both CPI and PCE had been hovering. If jobs stay weak and inflation numbers get uglier, there is every reason to expect intervention by the White House in the BLS and BEA process (see Happiness is Doing Your Own Report Card 8-1-25).

Historical Context:

We now live in a world where votes and economic data get rejected, and the lemmings fall right into line and join the disinformation chorus. The data sets do struggle in payroll, and the need to use better model assumptions and improve survey utility have been picked over ad nauseum. When Trump piled on the “get rid of quarterly reports” bandwagon (in the age of AI and streamlined data delivery), the “intent” to mask any negative trends in the economy started to get more transparent in terms of motives.

The explicit Project 2025 ambition (Chapter 21, 24) is to consolidate data and information and unify control – not to assure better and more comprehensive data. That has been evident in an array of actions that we have covered in other notes. Ambitions for better data require more investment, more tech, and more public-private alliances. That dilutes control – and closer control is the point for the White House.

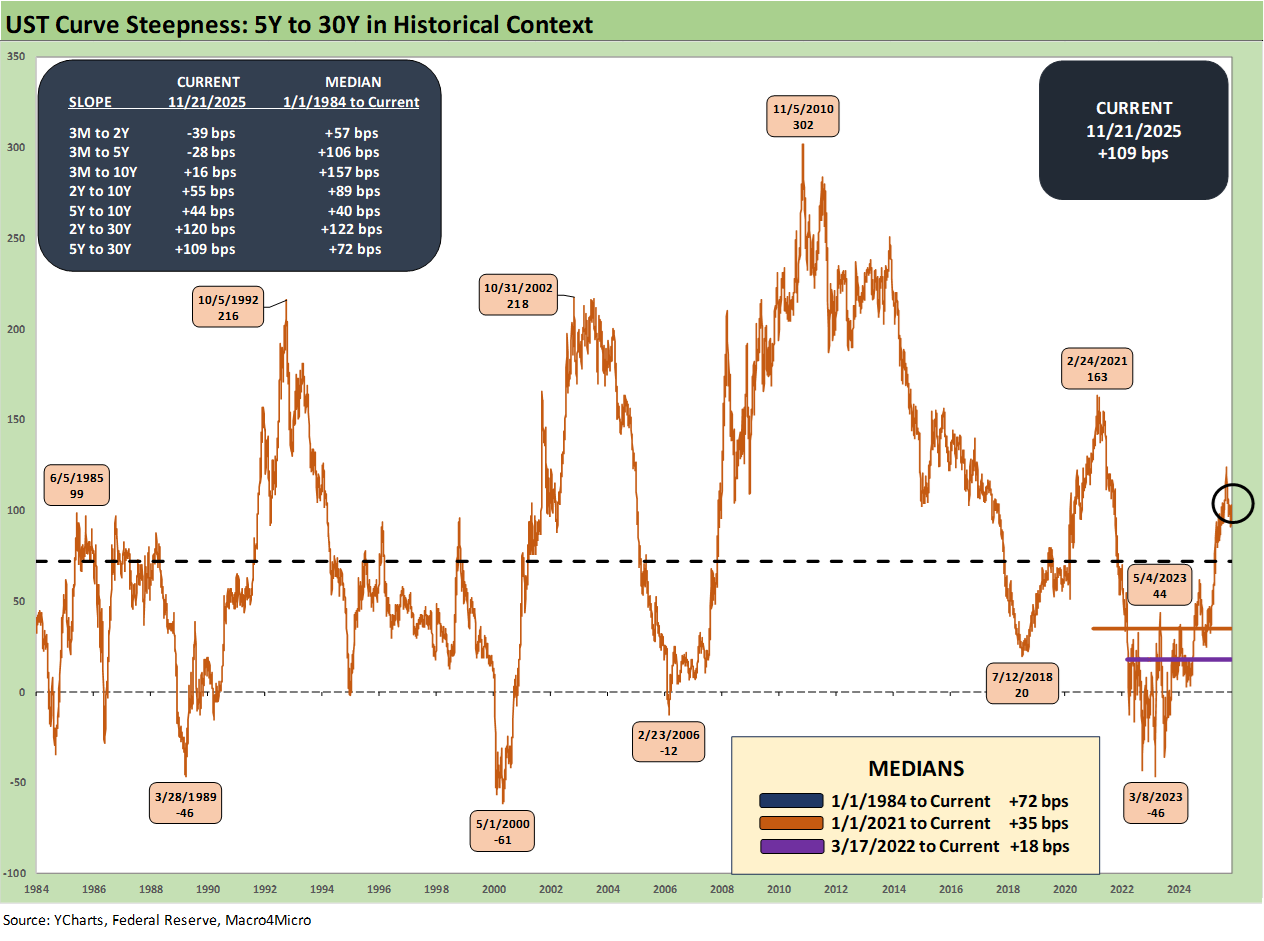

Recent Trends:

The above chart plots the 5Y to 30Y slope from 1984 for a read on the current shapeshifting potential ahead. For the 5Y to 30Y, the current +109 bps is well above the long-term median of +72 bps as the 30Y move of -7 bps has lagged the 5Y move of -76 bps during 2025 as detailed in earlier charts. That relationship shows room for flattening from current levels in theory, but FOMC easing could drive even more steepening subject to the ability of the 30Y to move higher if inflation remains a challenge.

A more sustained rally in the 30Y might end up as more of a “wish list” item than a likely reality given the noise around 30Y bonds on a global scale. The UST shifts with FOMC actions, but UST rallies have struggled with the 10Y to 30Y in relative terms.

We include a box within the chart above that details the other UST curve segment slopes that we watch along with the long-term medians. The front-end inversion from 3M is still the most anomalous part of the curve when you consider the fact we have been in an economic expansion since spring 2020 after a very brief 2-month COVID recession per NBER.

Historical context:

Bear steepening moves have been common in the 2024-2025 timeline, and the next move could be more of the bull steepener from the front end as the FOMC moves down. That may await a new Fed Chair more inclined to do whatever Trump says and regardless of the merit of any such move. The days of Fed independence are numbered. The tariff topic is one more force that keeps the “good vs. bad steepener” debate on the front burner. Reality is setting in.

The economy had been slowing in 2025 with PCE inflation still inside the 3.0% line as of the last read in August (see PCE August 2025: Very Slow Fuse 9-26-25). We are seeing plenty of inflation pressures across select product lines and numerous major lines are running higher in Sept 2025 than in Dec 2024. All you have to do is turn off the sound on the TV and look at the numbers (see CPI September 2025: Headline Up, Core Down 10-24-25). Trump recently stated that energy inflation was much lower now. Actually, total Energy has risen in 2025 (see Simplifying the Affordability Question 11-11-25).

See also:

Market Commentary: Asset Returns 11-23-25

Mini Market Lookback: FOMC Countdown 11-23-25

Employment Sept 2025: In Data We Trust 11-20-25

Payrolls Sep25: Into the Weeds 11-20-25

Credit Markets: Show Me the Data 11-17-25

The Curve: Slopes Can Get Complicated 11-16-25

Mini Market Lookback: Tariff Policy Shift Tells an Obvious Story 11-15-25

Retail Gasoline Prices: Biblical Power to Control Global Commodities 11-13-25

Credit Markets: Budget Armistice or GOP Victory Day? 11-12-25

Simplifying the Affordability Question 11-11-25

The Curve: Back to the Future 11-9-25

Market Commetary: Asset Returns 11-9-25

Mini Market Lookback: All that Glitters… 11-8-25

Mini Market Lookback: Not Quite Magnificent Week 11-1-25

Synchrony: Credit Card Bellwether 10-30-25

Existing Home Sales Sept 2025: Staying in a Tight Range 10-26-25

Mini Market Lookback: Absence of Bad News Reigns 10-25-25

CPI September 2025: Headline Up, Core Down 10-24-25

General Motors Update: Same Ride, Smooth Enough 10-23-25

Mini Market Lookback: Healthy Banks, Mixed Economy, Poor Governance 10-18-25

Mini Market Lookback: Event Risk Revisited 10-11-25

Credit Profile: General Motors and GM Financial 10-9-25

Mini Market Lookback: Chess? Checkers? Set the game table on fire? 10-4-25

JOLTS Aug 2025: Tough math when “total unemployed > job openings” 9-30-25

Mini Market Lookback: Market Compartmentalization, Political Chaos 9-27-25

PCE August 2025: Very Slow Fuse 9-26-25

Durable Goods Aug 2025: Core Demand Stays Steady 9-25-25

2Q25 GDP Final Estimate: Big Upward Revision 9-25-25

New Homes Sales Aug 2025: Surprise Bounce, Revisions Ahead? 9-25-25

Mini Market Lookback: Easy Street 9-20-25

Home Starts August 2025: Bad News for Starts 9-17-25

Industrial Production Aug 2025: Capacity Utilization 9-16-25

Retail Sales Aug 2025: Resilience with Fraying Edges 9-16-25

Mini Market Lookback: Ugly Week in America, Mild in Markets 9-13-25

CPI August 2025: Slow Burn or Fleeting Adjustment? 9-11-25

PPI Aug 2025: For my next trick… 9-10-25

Mini Market Lookback: Job Trends Worst Since COVID 9-6-25