Retail Sales Jun25: Staying Afloat

Consumer demand stabilized in June, reflecting normalizing behavior after a period of tariff-fueled uncertainty just as those concerns show signs of materializing.

I feel better. I think I’ll go shopping.

Headline retail sales increased +0.6% MoM, recovering from a -0.9% drop in May. The front-loaded reaction to the tariff news was much quicker than the slow rollout of eventual pain as the slow burn of inflationary effects will begin to appear in working capital cycles after the new wave from the Aug 1 date.

Core retail sales saw similar growth at +0.5% in June as spending among discretionary line items supports consumers’ willingness to spend. With only two more weeks until the new tariff start date, consumers are once again faced with prospects of budgeting amidst rising prices and what tradeoffs will need to be made. The Aug 1 start date sees outsized tariffs targeting countries representing 70% of US trade before considering additional Section 232 actions.

The resilient consumer seen in these retail sales results continues to show how hard it is to slow the consumption machine, as consumer sentiment recovered off the tariff lows with UMich and the NY Fed see easing inflation expectations in survey data. Bank earnings this week have echoed similar themes, as delinquencies remain anchored and loan loss provisions remain stable, as the employment picture supports consumer stability.

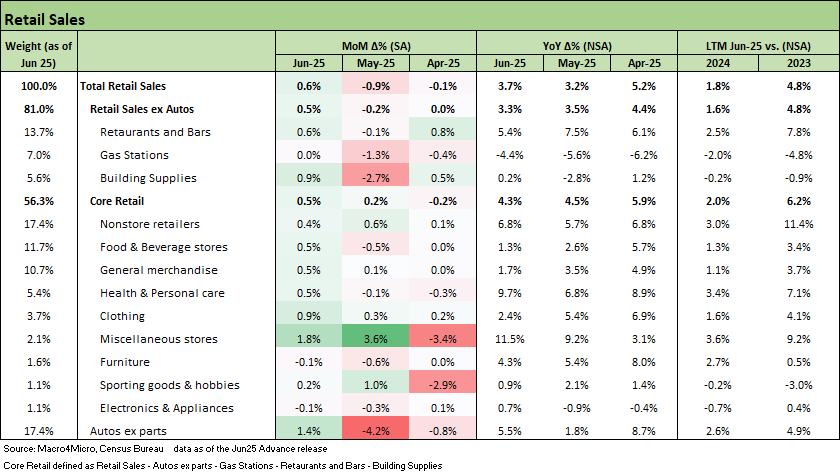

The above month-over-month changes for headline retail sales highlights the stabilization and recovery this month after the uncertainty of tariffs led to a pull-forward effect causing volatility in consumer demand patterns. The recovery in June is broad and not just across those weaker categories such Autos and Building supplies but included increasing discretionary demand in areas like restaurants, bars, and clothing stores. This supports a read that the past few months have been more of a whiplash than true sustained deterioration.

Consumer health is a natural focus when they are a key piece of how the increases from tariffs will flow through across higher prices or lower margins but for now the signal is still stable at least. UMich sentiment numbers have recovered as the inflation expectations have come down from the peak after the Liberation Day news, and that recovery is consistent with normalizing consumer spending. In addition, Q2 bank earnings kicking off this week show they see similar behaviors with delinquencies still stable though there are signs of more disciplined use of revolving credit. JPM and Wells Fargo acted on confidence in consumer credit, leading to lowering loss provisions.

The reality of backwards looking data and patterns is that the largest of the effects is still yet to come and the extent and breadth of the impact of such an unprecedented trade policy still lurks. Simply continuing to say that the “seller pays” does not eventually manifest it as a reality and there will be a burden on to the consumer. As we saw in the CPI numbers earlier this week, the pass-through effects from tariffs may still be in early innings. Though the full extent of eventual impacts is hard to gauge given the unpredictability of the trade “deals,” those impacts are materializing.

The above chart shows the line item details underlying the headline retail sales number as well as the key ‘ex-Autos’ and Core retail lines. The takeaway this month is that the recovery was broad with only the smaller Furniture and Electronics & Appliances categories continuing to trail. The largest winners this month come from the lowest starting points, with Autos, Building Supplies, and Food & Beverage stores all seeing large positive swings back.

We highlight here that though June is a slower month, the strongest signal in subduing doubts around the consumer is the rebound in discretionary spending categories such as food and clothing. The next few months are in focus as to whether this is the start of an acceleration (less likely), or another sign that the consumer was largely stable and plodding along as it was heading into the year given such a strong labor market.

It takes a lot to destabilize the consumer, but the most recent tariff actions may still tip the scales. The reality of trade war risk is not gone with higher risk clashes ahead with the EU, Canada, and Mexico still a risk. We will see more flowthrough effects on pricing along the way as working capital cycles feel the transaction level effects. These headwinds will play out across months and seasons including back-to-school and holiday retail numbers. We will get a preliminary read on 2Q25 GDP and PCE lines later in the month and a fresh set of PCE inflation, income and outlays numbers. For now, the consumer is “holding serve” after some recent setbacks.

Markets:

June 2025 Industrial Production: 2Q25 Growth, June Steady 7-16-25

CPI June 2025: Slow Flowthrough but Starting 7-15-25

Footnotes & Flashbacks: Credit Markets 7-14-25

Footnotes & Flashbacks: State of Yields 7-13-25

Footnotes & Flashbacks: Asset Returns 7-12-25

Mini Market Lookback: Tariffs Run Amok, Part Deux 7-12-25

Mini Market Lookback: Bracing for Tariff Impact 7-5-25

Payrolls June 2025: Into the Weeds 7-3-25

Employment June 2025: A State and Local World 7-3-25

Asset Return Quilts for 2H24/1H25 7-1-25

JOLTS May 2025: Job Openings vs. Filling Openings 7-1-25

Midyear Excess Returns: Too little or just not losing? 7-1-25

Recent Tariff commentary:

US-France Trade: Tariff Trigger Points 7-17-25

Germany: Class of its own in EU Trade 7-16-25

US-Canada Trade: 35% Tariff Warning 7-11-25

India Tariffs: Changing the Music? 7-11-25

Taiwan: Tariffs and “What is an ally?” 7-10-25

US-Trade: The 50% Solution? 7-10-25

Tariff Man Meets Lord Jim 7-8-25

South Korea Tariffs: Just Don’t Hit Back? 7-8-25

Japan: Ally Attack? Risk Free? 7-7-25

US-Vietnam Trade: History has its Moments 7-5-25

US Trade in Goods April 2025: Imports Be Damned 6-5-25

Tariffs: Testing Trade Partner Mettle 6-3-25

US-UK Trade: Small Progress, Big Extrapolation 5-8-25

Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25

Trade: Uphill Battle for Facts and Concepts 5-6-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

Tariffs: Some Asian Bystanders Hit in the Crossfire 4-8-25

Tariffs: Diminished Capacity…for Trade Volume that is…4-3-25

Reciprocal Tariff Math: Hocus Pocus 4-3-25

Reciprocal Tariffs: Weird Science Blows up the Lab 4-2-25