Ships, Fees, Freight & Logistics Pain: More Inflation?

We look at the recent Trump port fee gambit as China’s shipbuilding and maritime prowess gets elevated as a topic.

Trying to avoid the port fee?

Last night the USTR reached its decision on port fees for China-based ships, Chinese operators, and non-Chinese operators of Chinese-made ships. The fees will phase in gradually and move higher over time. China delivered a caustic response on the news which basically said they would protect their rights and their belief that these measures would fail to revive US shipbuilding anyway.

A lot of details were provided from the USTR on China’s ambitions in shipping in a Section 301 Investigation report. The investigation began under Biden in 2024, but the assigned port fees and related hearings come at a time of escalating trade retaliations between US and China.

The substance of the fees in moving the needle on China maritime leadership adds up to very little in substance, and the costs will be borne by shippers and their customers. “It is the thought that counts” and the fees make a statement.

As with tariffs, someone somewhere will feel the economic effects of the fees in price or in surcharges or in terms of secondary effects on shipping capacity (supply-demand) and how that flows into rates to and from regions (and select ports).

The reality of Chinese maritime dominance will not change any time soon (based on many massive barriers to entry). For trade purists, this is like major league baseball charging ballpark fees on the 1927 Yankees. Ruth, Gehrig, and “Murderer’s Row” would have still been hitting plenty of home runs and scoring a lot of runs. Ticket prices just would have risen. The overall plan offers another means of annoying China and will keep the tit-for-tat going.

The above chart plots some useful stock trend lines to remind us how badly freight and trade-sensitive benchmarks are doing. We include the Dow Transports line and a Maritime ETF (BOAT), but the same ugly performance applies to Dow Jones Trucking and many single names that derive their revenues and earnings from trade volumes.

Quoting the “transports” in stock commentary went out of style over the decades, but transport ETFs (e.g. XTN) have been getting pounded for a reason. The tariffs and threats of port fees are just the latest worry. The larger tariffs and ongoing retaliation risks are still the main events.

The World Trade Organization also released their World Trade Outlook this week, and the numbers were not pretty. The WTO expects -12.6% for North American Exports in merchandise (no other region is negative) and -9.6% for North American Imports. Again, no other region was negative for imports. The WTO admitted to the challenges of forecasting with so much uncertainty around what the final policies and retaliation will be. Empty containers piling up and cancelled sailings in the trade war between the #1 and #2 economies is not exactly arguing with the WTOs directional view.

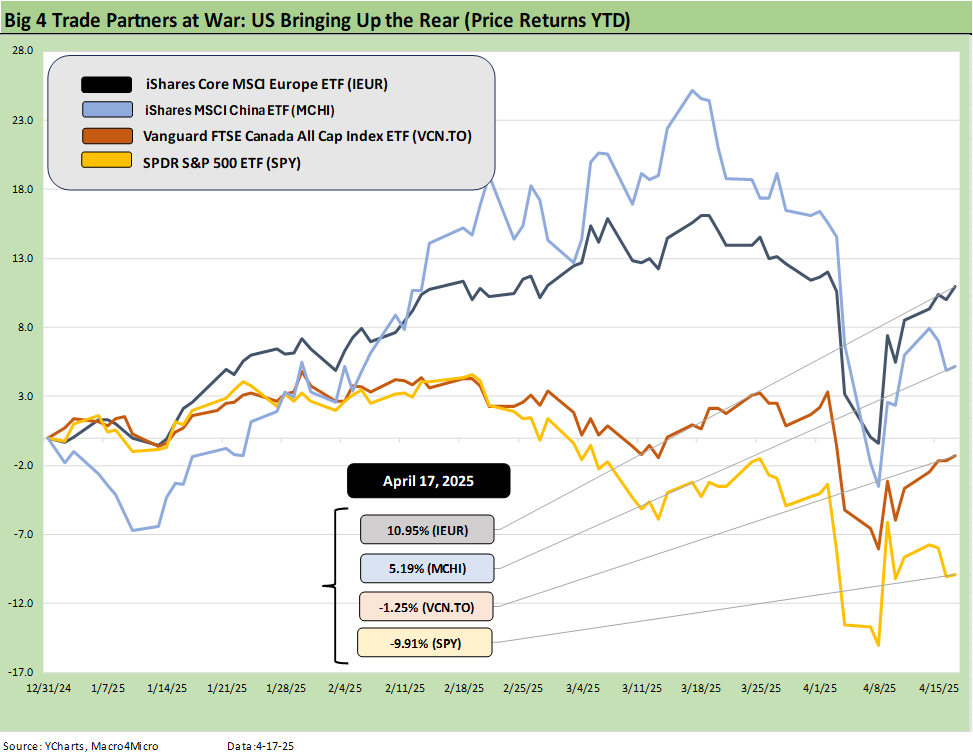

Many (not all) freight exposed names are getting hammered for a reason, but the broader benchmarks capturing the relative performance of the “Big 4” trade partners tells a story and is updated above. The numbers YTD do not reflect well on the US. The S&P 500 is the worst performer of the group by a meaningful margin vs. the Trump Tariff targets.

New Port fees add China tweaks, freight costs, and route disruptions…

To avoid burying the lede, the US Trade Representative’s Office finalized their plans to charge port fees on Chinese-owned vessels, China shipping companies, and non-China owners of Chinese made vessels. They also added some tariffs on major freight equipment. There were extensive hearings on the port fee issues with Day 1 and Day 2 in March unveiling a lot of pushback on the basis that many ports would be hurt and importers, exporters and customers would have suffered. That certainly rings true to the basic economic realities of higher costs that always cause a reaction somewhere in costs and thus on pricing or profits (just like tariffs).

A major change was that the fee would be assigned by trip to the first port (not the second or third ports visited, etc.) since the original policy would have threatened secondary ports and spiked freight costs even higher while hurting ports revenues and investment. The cap on fees was taken off according to what we read, and that could mean a higher absolute fee on the first stop based on tonnage. There were a range of carveouts and exceptions based on objections to the earlier proposal to ease the damage on the US side.

The main takeaway on the port fees is that the proposal is a subset of the claims made by USTR on maritime trade. The port fees have direct relevance to freight costs, shipping rates, and thus inflation risk. The original Section 301 investigation announcement back in April 2024 (that was under Biden and is not just a “Trump thing”) included the following two claims about China behavior:

“Controlling shipping freight rates and capacity allocations.”

“China threatens to discriminate against U.S. commerce and disrupt supply chains.”

Those two capabilities are exactly why China can retaliate above and beyond the ability to tariff US exports to China. The tariff wars are underway, and trade tactics can escalate with weapons beyond a % tariff targeting industries (note Boeing headlines this week on suspending deliveries). The restrictions on supplies such as strategic metals are already in the headlines, but the ability to tax or restrict more key China exports to the US includes a very long laundry list.

Dr. Scott Gottlieb (Pfizer board, Former FDA Commissioner, and leading expert) was on CNBC the other day delivering a scary set of scenarios around how China could disrupt the supply of intermediates in a materially damaging way to supply-demand and price trends and notably in generic drugs. That is not a new war game scenario, but that would most definitely be highly inflationary for the health care commodities line of CPI.

To pile on sports metaphors, picture a scouting report on a boxer (being from Brockton, MA I can’t help it.): “Sharp snapping jab and a brutal right hook.” This is where the US Trade Representative tells the boxer to “kick him in the shins and drop your gloves to your waist.” Not the best plan. Everyone will praise your manliness, but you may end up with an eight count – or worse.

Containers were part of the COVID pain and will be again…

The main takeaway is that the inflation” bucket” from the maritime supply-demand dynamics is a simple memory exercise to think back to all the port imbalances experienced during the COVID crisis. The market saw empty containers piling up and massive spikes on freight rates and delays were rampant. Many container shipping operations saw multiple record profits increase by 10-fold. Someone has to pay for the imbalances. The shipper always wins eventually in a market with chaos. Rates will be volatile, but they will get their pound of flesh.

If Bessent can say “the surplus trade partner always loses” he is missing the maritime freight volatility and supply imbalances in the real economy by critical product group. Don’t forget the shipping lines. If you believe that China can control capacity and rates as charged in the Section 301 investigation, then kicking them in the shins with port fees might elicit some payback. It will be something to watch.

Shipbuilding: China rules this massively capital-intensive sector. That will not change…

There are a lot of deep dives one can do about the relative competitiveness (or utter lack of) in shipbuilding and shipping (notably commercial but also in the area of naval or specialty ships such as icebreakers), but that is not the topic.

The immediate issue is more about a hike in the cost of freight and logistics as a result of port fee actions. The fees will not change the immediate status quo (in this case not even over a 5-year horizon) around who controls the maritime sector or who controls the balance of power in naval rivalries. China rules commercial shipbuilding, and they are the dominant player in maritime freight services. The China-US naval arms race is a separate topic for another day (e.g. Huntington Ingalls and General Dynamics, etc.). The White House put a Fact Sheet out on the topic (April 9) that covers some of these maritime topics.

Shipbuilding issues are not new in history. England dominated the seas, but Germany ramped up in shipbuilding before WWI. That made others nervous. Then Japan ramped up after WWI while the US went isolationist on the way to a depression. Now we have China and the obvious Taiwan worry. None of this is “new news,” but shipbuilding takes on a bigger significance with the trade war and port fee threats as well as a lagging US Navy.

Logical expansion of China while the US lagged in commercial…

Here is one mini checklist of ideas on how we got here in shipping with China. It is so simple and has been so obvious for decades. I remember when the Quincy Shipyard near my hometown closed in the 1980s and dislocated thousands of employees along the way. The shipyard was originally owned by Bethlehem Steel (also long gone) and then General Dynamics.

As far as the threat of China shipbuilding, there are obvious reasons China is so large:

China is the #2 economy in the world: Big economies have lots of trade, so ships, rails and trucks come in handy (seems obvious right?) China focuses on exports, so they needed the ships. No econometric wizardry needed to figure that out. While Russian built nukes and missiles and submarines, China built ships. That is a generalization, but that is what the world is looking at today. It is not exactly an unfair trade practice to invest in infrastructure. Punchlines like the “million-man swim” to retake Taiwan is now a distant memory. China has a massive Navy on the other side of a rather large ocean and built commercial ships alongside.

China is on the water: That tends to support a robust shipbuilding industry (that is a literal factor with a touch of sarcasm). The US has two big oceans yet here we are. In the “old days” industrial policy would be considered socialism – especially during the 1980s. Well-run ports promote trade (in both directions), and shipbuilding was a national strategic priority for China. So was ordering planes. Soon China will be building its own aircraft on a large scale. China has an easier time with a command economy focused on building out infrastructure and trade capacity.

China has built out port infrastructure: Like South Korea, Japan, and Singapore, who all “do the port thing” quite efficiently, China has had success in the booming pan-Asian trade and on the bigger global stage. That is how Li Ka-shing and Hutchinson Whampoa ended up with a strong position on the Panama Canal before their recent sale news. They were good at it (that tends to help). China dominates the largest ports lists in capacity ranking and in total ports.

The bottom line is that China did not sneak up on the world. They have been focused on shipbuilding for decades. That includes Trump 1.0. Where was the shipbuilding policy back then?

A big topic, a massive capital need, and few takers…

Either way, addressing shipbuilding would take a massive fiscal effort unless you can find a lot of bottomless pocket private sector businesses with a thirst for debt and losses. The supplier chain to even build out such capacity just soared in cost based on the current tariff binge. The shipbuilding drama starts to take on the flavor of political theater for a common-sense goal that would break any budget.

The Trump solution in advance is usually the same: when in doubt, slap fees and/or tariffs, and disrupt businesses as if there will be no economic reactions or multiplier effects. There is no budget for the massive scale of such shipbuilding needs, so we will add some tariffs and fees and issue some Fact Sheets.

I guess a question is “How many ships did Trump build during Trump 1.0? Biden? Obama? Bush? How are we doing on those Ice Breakers? There is a reason. Cost, capital, and competitiveness. But the show must go on. Political gestures need to be made, but they cost consumers money.

Freight and logistics players are nervous enough already…

The cover story last week for the Journal of Commerce was entitled: “The Big and Beautiful: Trump’s Plan to Restore US Shipbuilding Would Upend Supply Chains.” That title maybe skips the fact that the upending of supply chains is already happening, but the shipbuilding solutions might make it all worse.

Everyone wishes that the US had a robust shipping industry. That helps local economies, unions, multiplier effects abound, jobs multiply, and the waves of supplier revenue (notably steel) that feed shipbuilding rises. To get ‘there from here” is always tricky, however, and ignoring the costs and relative risks is typical. The fee plan initially included high port fees and even the scaled back one will add up.

The trade rags certainly paint a bleak picture of the cost and the ability to get the scale to compete in shipbuilding. High fixed costs and few units make for bad unit cost math in shipbuilding. I thought about not saying “that ship has sailed.”

Freight as the ultimate macro gut check. Some useful resources…

The material in Journal of Commerce routinely underscores the complexity and intertwined nature of the freight and logistics markets. I used to get the hard copy version long ago when we started CreditSights in 2000 since transportation sectors offered a good cyclical guide to economic activity. It made global macro work easier. The freight and logistics industry has exploded in the services sector (and also in tech tools) since then along with the WTO and China expansion.

Freight as a topic offers an easy shorthand guide on the direction of the economy. For source materials, we like Inside Trade (pricey service but with great content and high utility links to hearings and papers). We like Journal of Commerce while FreightWaves and Supply Chain Management Review are useful. Peterson Institute does great work.

Assessing failure objectively is a good idea…

Away from the potentially insurmountable barriers to becoming a major player in commercial shipbuilding within a decade (capital, costs, supply chains, etc.), the boom in global low-cost sourcing (lean manufacturing and the leaning of the supply chain) also added to the scale of information needs. The Section 301 investigation even includes a comment on the “information” piece of the puzzle in its complaint about Chinese activities. They accuse China of the following:

“Creating a Chinese network of suppliers, foreign ports and terminals, shippers, and equipment and logistics software that allow advantageous use of information…”

In the tech, data and information game, China is beating the US. The US is great at so many things, but every now and then we lose on the competitive playing field. Trump does not believe he ever loses elections (the 7 million vote loss in 2020 must be fraud even if zero evidence). Trump also believes that if the US loses in trade or economics it must be rigged (think German luxury cars). Recall how quickly Lexus broke into the luxury ranks against the Germans. Any subpar competition is part of a conspiracy and cheating as opposed to just poor performance.

Sometimes you just lose. Sometimes you get your ass kicked. Sometimes you fail to invest and prepare. Shipbuilding is one of those times. Effort and resource commitment were certainly not there. Top-down planning was MIA. Ford and GM did not execute well in Europe. The US integrated steel companies and many operations were blown up in the 1980s and 1990s. Defense and Aerospace saw the US become a juggernaut. France et al ate into Boeing’s franchise with Airbus, and Europe will now set its aim on defense. In the end, you have to win in the marketplace. Part of that reality is competing with command economies. We can’t pretend they don’t exist.

The US abandoned shipbuilding long ago as a priority since the Navy was stacked with top technology, carriers, world class submarines, and nukes. If the US is serious about shipbuilding it would have been in the current budget with a more balanced tax revenue plan. It isn’t.

The list of promises across icebreakers, strategic metals (ocean floor, Ukraine and Greenland, etc.), record drill, drill, drill and LNG all are out there. Where there are private sector economics, it will make progress. Fact Sheets mean little. When in doubt, talk about annexation. Ports and shipbuilding assets are across the Pacific. The Chinese built those shipbuilding capabilities the old-fashioned way: planning, budgets, resource commitment. Not with big talk.