US-Trade: The 50% Solution?

Trump goes off concept script again but with a 50% tariff tied to “coup bro” accountability and not economics.

Time for decaf in the White House trade planning meetings?

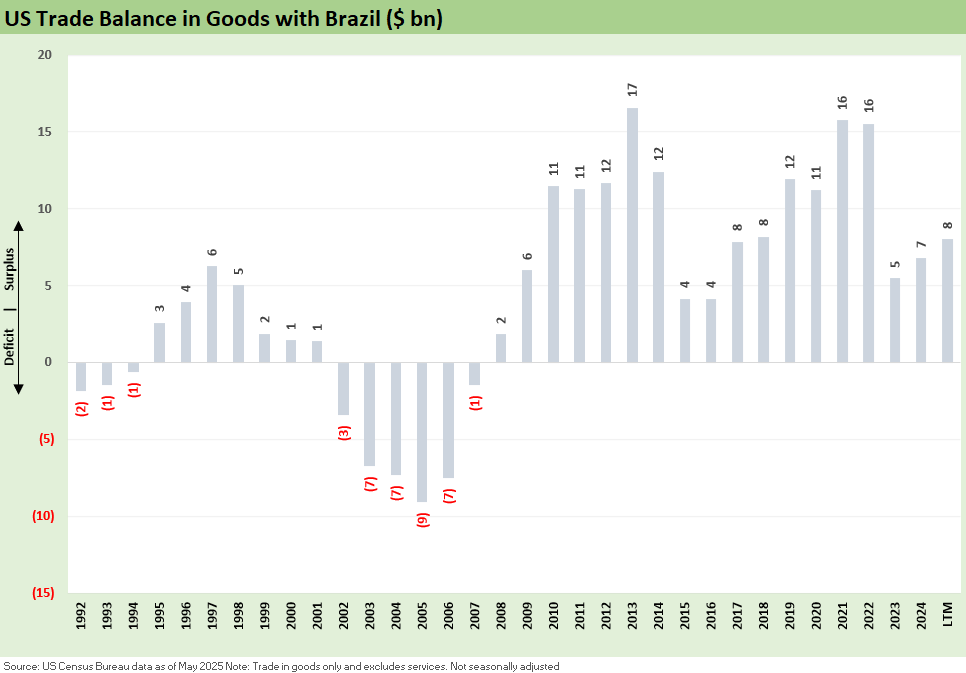

Brazil gets slammed with a 50% tariff even though it was not on the Liberation Day chart given the goods trade surplus that the US runs with Brazil (Reciprocal Tariff Math: Hocus Pocus 4-3-25,Reciprocal Tariffs: Weird Science Blows up the Lab 4-2-25). Trump also threatened to open a Section 301 unfair trade investigation as well given the move by Brazil to restrict online misinformation and propaganda by right wing extremists.

As economic policy goes, this latest tariff move is a strange one in strange times. In the mix of US trade partners, Brazil is the #1 export market and #1 importer for the US in the South/Central America region. US exports to Brazil were running YTD at almost 14% higher and imports over 8% higher, so the total trade volumes and US trade surplus was actually growing.

When Brazil retaliates as they promise, this could effectively turn into a two-way economic embargo based on the scenarios of more retaliation from Trump and Brazil matching it. China will naturally smell opportunity given the heavy commodity bias in Brazilian exports (and commercial aerospace) and give a fresh motivation catalyst for the BRICS initiative on currency.

The ability of the market to price this risk gets back to the challenge of putting a price tag on erratic, unilateral tariff assignments and how they can now be tied to political whim and interference with other nation’s politics. The rule of “when I see it, I will believe it” has been the norm in tariff news. In this case, the underlying reason is very abnormal but not way outside the tariff actions we have seen to date on much bigger trade partners

Any shifting risk premiums to factor in this latest change in behavior is more speculation than science, and the usual import vs. export cost frame of reference shows a YTD annualized import volume of $44 bn from Brazil. That is a tariff the US buyer pays customs by law (Trump is still saying the 180-degree opposite, which is false).

The above cut-and-paste excerpt from the White House covers the main deviation from the typical tariff form letter and captures Trump’s main gripe with Brazil. Election denying and attempted coups struck a nerve apparently. Trump has decided he now sets Brazilian law. Maybe he can move to export SCOTUS to Brazil to cover the appeal. They will be tariffed by Brazil at 50% now.

The idea that coming to the aid of a “coup bro” dictates trade policy with Brazil is hard to fathom. That would normalize the use of tariffs when non-US election and domestic policy inside trade partner’s laws dot meet approval of Trump. Using the US economy as leverage over non-US sovereigns and dictating trade partners’ domestic laws and policies is way off the reservation.

Anyone who does not see this as outside the acceptable trade policy strike zone is blindly partisan. Such actions can have the opposite effects of what is intended. It is like Trump, Musk, and Vance attacking Germany over the AfD. This can set a trend that can spreads globally and go both ways. Trade is no longer governed by the economics in the US, and that is getting more evident.

Brazil Imports vs. Exports…

As detailed in the above chart, the Trump action has nothing to do with trade balances. The US also had a goods trade surplus with the UK. Those are unusual when it comes to major economies. The US almost always has a deficit. We look at the product groups in the top import vs. export list below.

A notable highlight of the letter (not shown in the above excerpt) was Trump stating he needed to cut the unsustainable trade deficits like Brazil’s since they are a threat to national security. The fact that the US has a trade surplus – not a deficit – with Brazil is either a tribute to administrative incompetence or excused by the fact that Musk might have “DOGED” the proofreaders.

The import mix above faces the tariffs, and – contrary to constant Trump repetition – the US importers/buyers pay the tariff to customs. Some of these import lines (e.g. steel) were already doomed by other product tariffs while some will now see higher tariffs given the Trump move to 50% (and potential to retaliate to 100% if Brazil matches).

Team Trump has been making unofficial statements that the new “reciprocal tariffs” will not be stacked, but we have not seen that on Brazil yet. Of course, “reciprocal” is a misnomer even if “trade deficit elimination tariffs” does not roll off the tongue. Brazil tariffs are specially difficult to label given the noted history of US trade surpluses. Trump included the threat of Section 301 tariffs in his letter. The 301 use was a standard go-to tariff strategy used against China in Trump 1.0.

The mitigating good news for Brazil is they should be able to find alternative markets for most commodities. There could be a growing supply of new buyers who are also being treated badly by Trump. Changing sourcing from the US to Brazil could be seen as a way to retaliate against the US by other means (i.e. buy from Brazil instead of the US).

The export mix from the US to Brazil is led by Aerospace and Refined Petroleum products. Aerospace is a tricky one since the main Embraer competitor is Bombardier, and Trump treats Canada badly also (Airbus has some A220 operations in the US). Canada also still has some material trade war risk that could escalate.

Embraer is looking at expansion into larger aircraft, and the potential for alliances with Europe and China will make for interesting scenario spinning. That is for another day. Boeing had come close to acquiring Embraer before COVID, so it is a prime asset in the space for the right strategic investor with a plan to navigate the US tariff aggression. The declaration of trade war on the Brazilian economy by the US (read “Trump” as the US) will open up a lot of speculation.

The above chart offers a reminder that total US-Brazil trade has risen steadily from both imports and exports, and that means more economic activity in the US and Brazil. The idea of multiplier effects has never worked its way into the Trump trade rap (or conceptual thought process), but is pretty basic in economic principles (see The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25, Tariffs: Questions to Ponder, Part 1 2-2-25). After all, Trump cannot even accurately state who pays customs the tariff.

Brazil’s annualized total trade volume (exports + imports) was on track to get close to the $100 billion line this year, which would be close to the Top 15. That will now go off the rails. This is right about the time China is supposed to “propose marriage” to Brazil. China would be a natural end market for Embraer products and technology and also the waves of dollar-based commodities looking for a new currency in the BRICS initiative. Similarly, Brazil would be a natural end market for China aerospace and defense initiatives. We assume Xi is not staying up late at night worrying about Bolsonaro.

Tariff related:

Tariff Man Meets Lord Jim 7-8-25

South Korea Tariffs: Just Don’t Hit Back? 7-8-25

Japan: Ally Attack? Risk Free? 7-7-25

US-Vietnam Trade: History has its Moments 7-5-25

US Trade in Goods April 2025: Imports Be Damned 6-5-25

Tariffs: Testing Trade Partner Mettle 6-3-25

US-UK Trade: Small Progress, Big Extrapolation 5-8-25

Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25

Trade: Uphill Battle for Facts and Concepts 5-6-25

Tariffs: Amazon and Canada Add to the Drama 4-29-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

Tariffs: Some Asian Bystanders Hit in the Crossfire 4-8-25

Tariffs: Diminished Capacity…for Trade Volume that is…4-3-25

Reciprocal Tariff Math: Hocus Pocus 4-3-25

Reciprocal Tariffs: Weird Science Blows up the Lab 4-2-25

See also:

Footnotes & Flashbacks: Credit Markets 7-7-25

Footnotes & Flashbacks: State of Yields 7-6-25