Germany: Class of its own in EU Trade

We update the import-export product groups in US-Germany trade with a lot of high value flows in both directions.

US and Germany: Struggling to Find a Fit

We look at the trade deficit history between Germany and the US and break out the top line items in the import and export mix. Lost in translation in the trade policy upheaval is any discussion of the needs of the buyers of these high value-added products, where purchases were made at arm’s length in free markets.

We don’t hear trade policymakers wondering whether the buyers have ready substitutes or where US companies can make their own decisions as they see fit. If this was the 1980s and a Democrat was making these same tariff decisions, there would be a GOP armed uprising.

The pharma, autos, and manufacturing mix in Germany-US trade make for a very challenging story and question whether trade can be economically viable with a mix of 30% tariffs and the collection of Section 232 tariffs already printed and in the queue (most notably pharmaceuticals but also semis and aircraft/parts).

German export domination has been a fact of life within the EU and Eurozone and in numerous manufacturing industries with the US. The difference between superior products and free market decisions tend to get distorted by some of the fact free and concept anorexic spin to rationalize protectionism and closer control of the economy by the White House.

The idea of losing in competition in free markets gets rebadged as “ripping off” and the US “subsidizing” other countries. As in elections, sometimes you win in commerce and sometimes you lose. The Trumpian solution is to take it out of the decision-makers’ hands by changing the rules or undermining the system. Competition is how the global trade championed by the US in the postwar world was supposed to work.

As Section 232 and “not-really-reciprocal” tariffs get slowly digested by the markets, the economics of many product lines in US-EU trade will be severely (some fatally) damaged and possibly in both directions on retaliation. The idea that all trade partners will accept what are in effect “terms of surrender” is unrealistically optimistic and more trouble lies ahead. The key for Team Trump getting the EU to fold is to exploit the division across the EU (the same for Canada with the provinces).

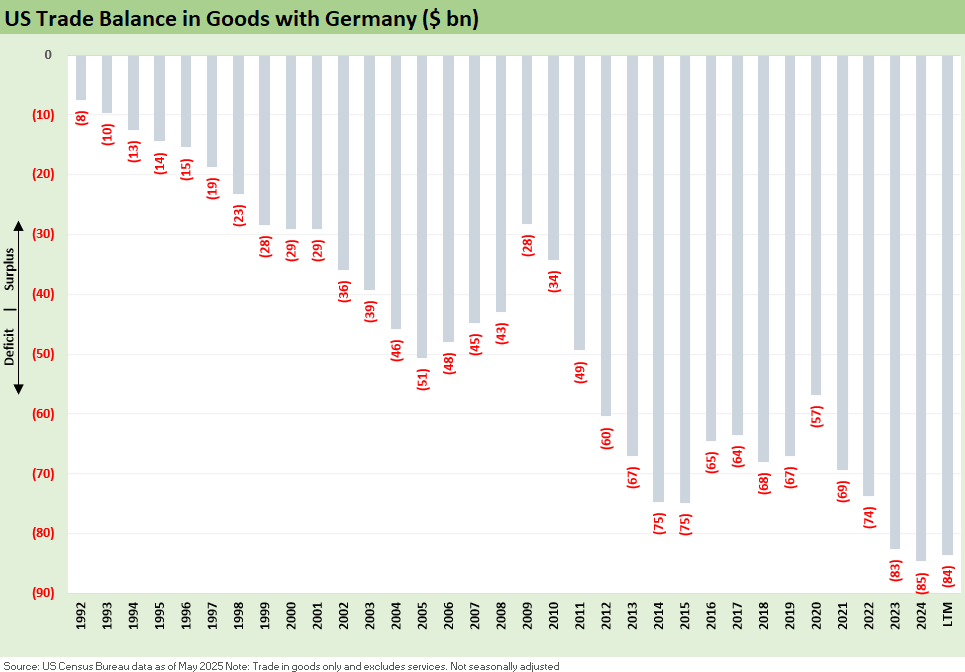

The above chart details the goods trade deficit since the early 90’s on the way to record high US-Germany trade deficits. Germany’s legacy manufacturing prowess is very much in evidence in the overall mix as we cover below. We see autos at #1 and a wide range of machinery and equipment lines joined by a tier of the supplier chains. We also see pharmaceuticals as a close #2 as Trump has already set the stage for pharma Section 232 bringing “very, very high tariffs” and potentially 200% (with a timer to relocate) as promised by Trump this past week.

The hostility of Trump to the EU (“created to screw the United States” etc.) is well known, but the 30% tariff rate proposed has already been tagged by EU leaders as essentially a step in the direction of a de facto economic embargo given the economics of these product lines. With the tariffs proposed on steel and metals, autos/parts, and downstream integration of US transplant operations with German supplier chains, a lot of damage is in the works from manufacturing costs to potential all-in pricing dislocations with the “buyer/importer” (not the seller) paying the tariff.

With Daimler and BMW both big players in the US in the premium vehicle market and some transplants investing in Mexico or buying components south of the border, North American auto production chains are under siege by tariffs. We also see Daimler and Volvo as leading commercial vehicle players in the US and the world, so the supplier chain noise will see the volume turned up to “blast” in how Germany and EU nations are supposed to deal with the US tariff attacks.

EU truck leaders (commercial vehicles) have been investing heavily in the US for decades going back to the early 1980s (e.g., Volvo and White Motors back in the 1980-1982 double dip). The Class 8 truck market is more a North American regional market, but the supplier chain can still be global. In commercial vehicles, iconic brands such as Mack Trucks (first Renault/later Volvo), Freightliner (Daimler), and Navistar’s iconic International brand (acquired by VW’s Traton Group) all saw EU corporate control. The International brand goes back to International Harvester, so that is a lot of US history.

In later years, BMW and Mercedes built transplant light vehicle operations that have also seen a greenfield boom in the US (primarily in “red right to work” states). Add in the buildout of massive assembly and supplier chain operations in the US with growing dealer operations by BMW and Mercedes (Daimler), and there is a lot more to the US-centric operations than just a trade deficit that gets fed a lot of equipment from German imports.

There will be plenty of questions on what the tariff impact will be in unit costs for these autos and truck operations from offshore or “home team” component suppliers (e.g. engines, powertrains, etc.) vs. US suppliers. BMW is also the largest auto exporter of light vehicles by value in the US. Are Daimler, Volvo, BMW, and VW operations essentially being required to buy only US equipment? Is that even possible? How does one start an operation here and be instantly 100% US sourced?

The above is a long version of saying “Germany has succeeded in rebuilding and revamping operations that might have otherwise struggled or failed.” Before acquisitions by German and some EU operations (Sweden, France), some (not all) of those companies might have failed, some were failing, or were struggling. Some did not exist (the light Mercedes and BMW vehicle transplant operations). Those of us covering these old truck companies (or having employers as lead creditors) saw entire brands saved by German and EU acquisitions.

The above chart details the leading imports from Germany. Away from the fact that Team Trump wishes all these imports were made here, the obvious questions include items such as the following:

Why were these purchases made?

Was the purchase made on the basis of quality, cost and specific needs?

Was the relationship long established and successful?

Are there substitutes readily available in the US at the same cost that is equivalent in quality?

If no alternative is available, what damage is done to the US buyer if the importer needs to pay the higher cost? (After all, the buyer pays the tariff at customs). Will these barriers deter investment?

Was the purchase made to supply a German multinational that has invested in the US and set up manufacturing operations using established suppliers?

Is the rule going to be that all German manufacturers that set up operations in the US must be 100% vertically integrated within the US? If so, will that undermine economics and risk future operations from planting the flag in the US without factoring in the high tariff structure and inflexible supplier chain options into project economics? How does that shape risk vs. reward?

Will the tariff penalties for buying from non-US suppliers discourage German investment in the US and make it easier to simply wait for the next administration? Can the next President just say “ the emergency is over”?

You get the idea. The lack of granular analysis across product lines has been a problem since all decisions are made looking through a few narrow lenses and continued thought exercises that are divorced from the economics of a business. Even just in framing “reciprocal tariffs,” it is clear only minimal work was done. That “reciprocal” misnomer has now more openly been transformed into “trade deficit elimination” while failing to be honest about the risks and potential unintended consequences. Trump was bragging about the first $100 bn of revenue from tariffs but denies the US buyers paid. He says they are “taking in money” from selling countries.

As with his de facto neutering of Congressional GOP leaders, Trump’s game plan depends on the cowardice and fears of the weak links (or blindly self-interested constituencies) in the EU and Canadian provinces. It has worked for him so far in the US. China called him on it, and he backed down since Xi was on an autocratic level playing field with Trump’s de facto strongman rule. That is not the case in the EU bureaucracy or in Canadian provincial relationships.

The above chart does the same exercise for exports to Germany. It would be interesting to know how many of the Autos and Light Vehicles exported to Germany from the US are German badged vehicles manufactured in the US transplant belt.

We see a high value-added mix with Pharma, Aerospace, and Autos in the top 3 export lines. The list does not match up to the German-US import list in depth, but there is room for more than a little damage in retaliation. Germany also factors in the EU-wide trade bloc retaliation power if they get on board. Pharma and Aerospace exports to the EU really add up even if much lower than EU pharma into the US (see US-EU Trade: The Final Import/Export Mix 2024 2-11-25). Even without factoring in the company-level impacts, there is always the issue of damage done to those US households that need the medication and the threat to either their physical health or household finances in the face of Medicaid cuts.

The above chart details the import and export time series from the early 1990s through LTM. The import line into the US reflects the sheer size and health of the US economy during a period when there was a great deal of structural change unfolding in Europe from the pre-eurozone years across the financial crisis and then COVID years. It was also a period of secular change in the US toward more services and less manufacturing tied to NAFTA and the rise of China. So the US looked to where they could fill their needs from Germany, who had to compete on price and quality in manufacturing machinery and equipment and transportation equipment.

Germany expanded in the US in light vehicles the way Japan did. Both Germany and Japan excelled and invested billions in capital and added millions in jobs along the transplant ecosystems including dealer networks and F&I products downstream and OE supplier and materials investment upstream.

The question of how to reverse that trend by attacking German manufacturing is unclear to say the least. The end result could be a stall/decline and simply higher costs in many of the product lines. Once again, those costs are paid by the buyer – the opposite of what the White House represents.

The US may need to be able to compete head-to-head in some of these businesses. The US failed to do so in autos when Ford and GM were major light vehicle manufacturers in Europe – including on the ground in Germany for decades in scale. The history of GM and Ford in Europe in recent decades has been failure, closures, and major asset sales. Auto OEM consolidation in Europe is a separate story. The Trump refrain of “they don’t buy US autos” ignores this factual history. It was not unfair trade. Rather, it was inferior performance.

Germany is the #3 economy in the world after edging past Japan even though it is a distant #3 behind the US and China. Germany can do some damage if the EU fight back when taken in tandem with France and some other major EU economies. The EU bloc was designed in part to collectively protect the EU nations even if Trump said it was to “screw” America. The other view in the EU is to protect the European countries from getting screwed by America (after all, who would do a thing like that?!). One way or the other, the clock is ticking.

Markets:

CPI June 2025: Slow Flowthrough but Starting 7-15-25

Footnotes & Flashbacks: Credit Markets 7-14-25

Footnotes & Flashbacks: State of Yields 7-13-25

Footnotes & Flashbacks: Asset Returns 7-12-25

Mini Market Lookback: Tariffs Run Amok, Part Deux 7-12-25

Mini Market Lookback: Bracing for Tariff Impact 7-5-25

Payrolls June 2025: Into the Weeds 7-3-25

Employment June 2025: A State and Local World 7-3-25

Asset Return Quilts for 2H24/1H25 7-1-25

JOLTS May 2025: Job Openings vs. Filling Openings 7-1-25

Midyear Excess Returns: Too little or just not losing? 7-1-25

Recent Tariff commentary:

US-Canada Trade: 35% Tariff Warning 7-11-25

India Tariffs: Changing the Music? 7-11-25

Taiwan: Tariffs and “What is an ally?” 7-10-25

US-Trade: The 50% Solution? 7-10-25

Tariff Man Meets Lord Jim 7-8-25

South Korea Tariffs: Just Don’t Hit Back? 7-8-25

Japan: Ally Attack? Risk Free? 7-7-25

US-Vietnam Trade: History has its Moments 7-5-25

US Trade in Goods April 2025: Imports Be Damned 6-5-25

Tariffs: Testing Trade Partner Mettle 6-3-25

US-UK Trade: Small Progress, Big Extrapolation 5-8-25

Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25

Trade: Uphill Battle for Facts and Concepts 5-6-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

Tariffs: Some Asian Bystanders Hit in the Crossfire 4-8-25

Tariffs: Diminished Capacity…for Trade Volume that is…4-3-25