PCE Income & Outlays Dec 2025: Inflation Reversal?

On a day when GDP was a mild disappointment, the PCE inflation story got a little worse.

FOMC planning session.

The market had a PCE price index setback to end 2025 just as Fed independence had eased out of the headlines. Warsh will get his test soon enough.

With the headline PCE price index rising to 2.9% from 2.8% and Core PCE prices moving to 3.0% from 2.8%, life is going to get tricky at the Fed unless payroll trends offer more excuses.

Food inflation in PCE ticked higher to 2.1% YoY in Dec 2025 from 2.0% in Nov 2025 while Energy Goods and Services ticked lower to 2.2% in Dec from 4.4% in Nov 2025. That energy number is still well above the recent deflation (including -3.8% in May).

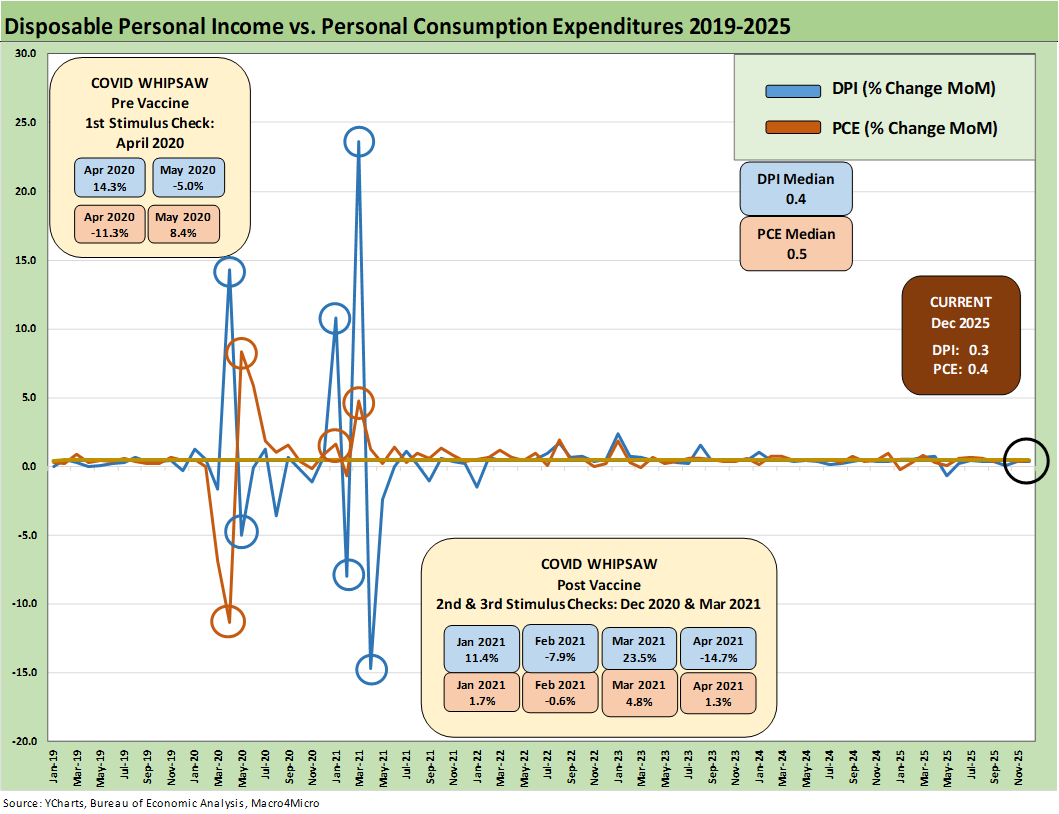

Personal Consumption Expenditure growth ran ahead of Disposable Personal Income Growth, so the consumer remains in the game.

The combination of higher PCE inflation on a mediocre 4Q25 GDP reporting day keeps the market tone mixed with the end of IEEPA raising questions on what comes next (see 4Q25 GDP (Advance Est.): Less Distortion This Time 2-20-26).

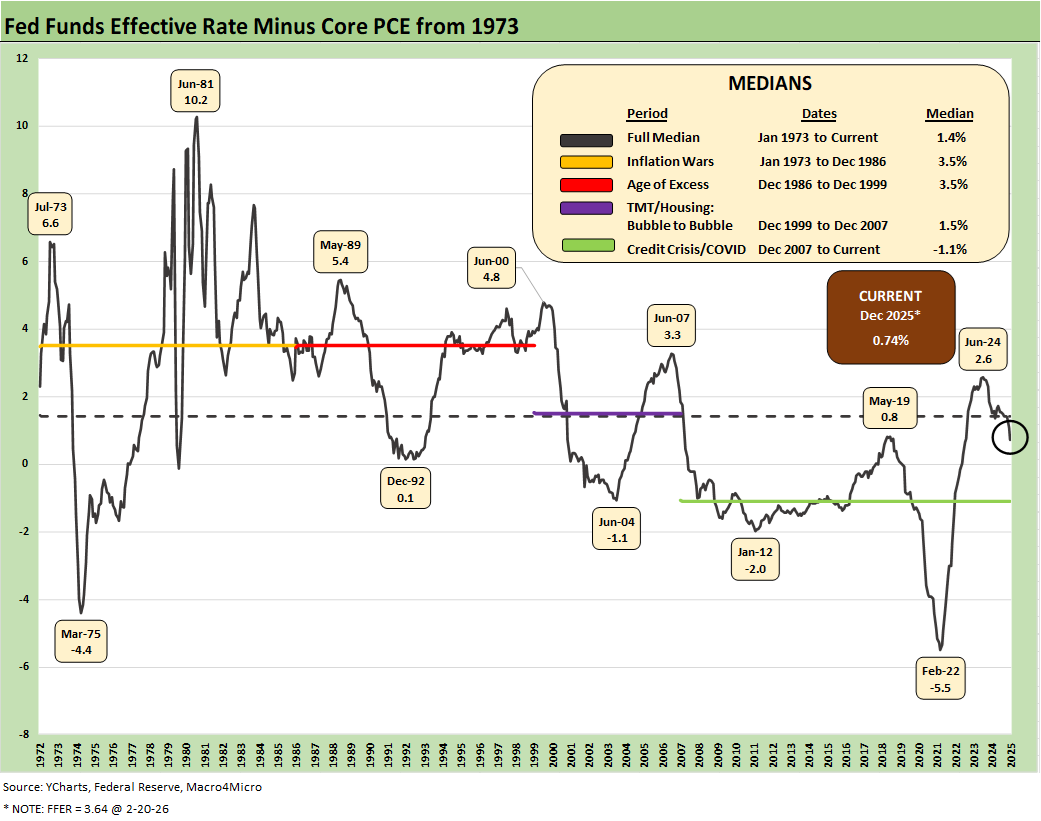

The above chart updates the time series for “fed funds minus core PCE.” The PCE inflation metric tends to be a focal point for the FOMC and economists, but the pressure on energy costs (notably electricity and utility piped gas) and food inflation are attracting household finance focus and influencing consumer moods in a midterm election year.

The long-term median on the FFER vs. PCE differential is 1.4%, but recent easing has cut that almost in half. In a range of comments, Trump has demanded an immediate move to negative real fed funds rates by the Fed. That is easier said than done with inflation well above the Fed target and the economy doing better than earlier in 2025. Today’s PCE release will not help with headline PCE price inflation higher at 2.9% in Dec vs. 2.8% in Nov and 2.5% as recently as May. Core PCE rose to 3.0% YoY in Dec from 2.8% in Nov 2025.

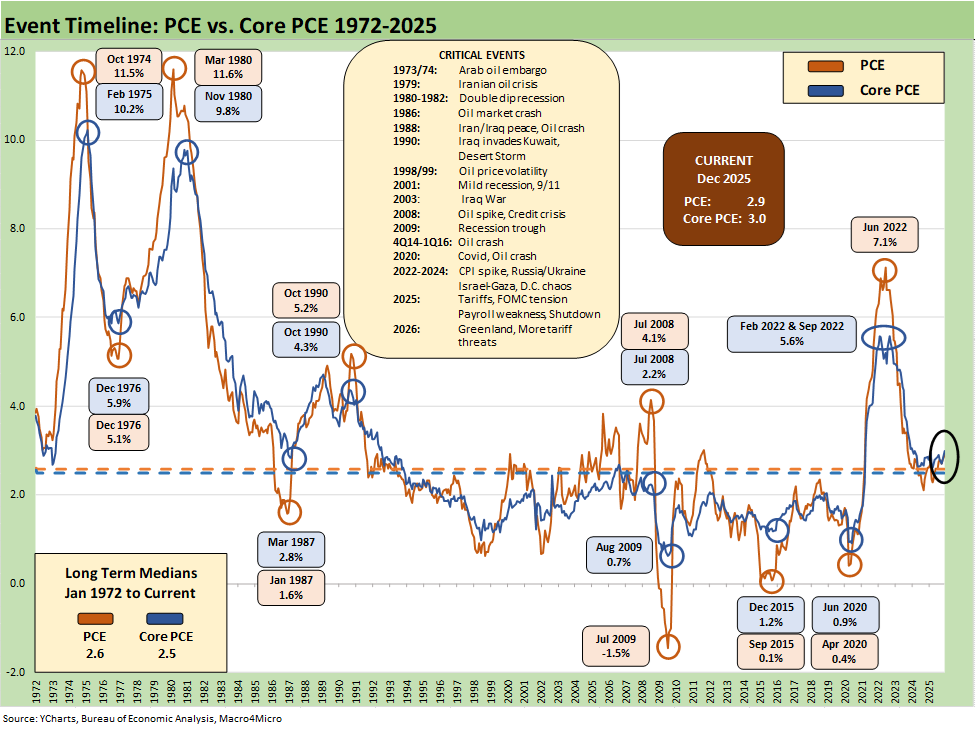

The above chart updates the long-term time series from 1972 for PCE vs. Core PCE across the decades and cycles. We see the 2.6% headline PCE long-term median in the lower left (below the current 2.9%) and the 2.5% core PCE median (vs. current 3.0%). That 2.9% headline is dramatically better than where we came from in July 2022 at 7.1% PCE, but it is still well above the 2.0% target.

The Dec 2025 PCE numbers are at reasonable levels in long-term context, but they are in somewhat of a stall with numerous key lines going in the wrong direction. Even if one seeks to embrace the “one-time event” theme for tariffs, that still means higher price levels that can bring reduced purchasing power for select line items – subject to a household’s typical “basket” (coffee drinkers, beef eaters and “sweets” fans take note).

In the move from early spring to Dec 2025, Goods moved from deflation to +1.7% inflation. We see Energy Goods and Services move from -3.8% deflation in May to +4.4% inflation in Nov 2025 and now down to +2.2% in Dec 2025. Services remain sticky at +3.4% in Dec 2025 down slightly from +3.6% in Aug 2025. When you hear the refrain of “prices are way down” in the White House rambling routines, it is simply not true.

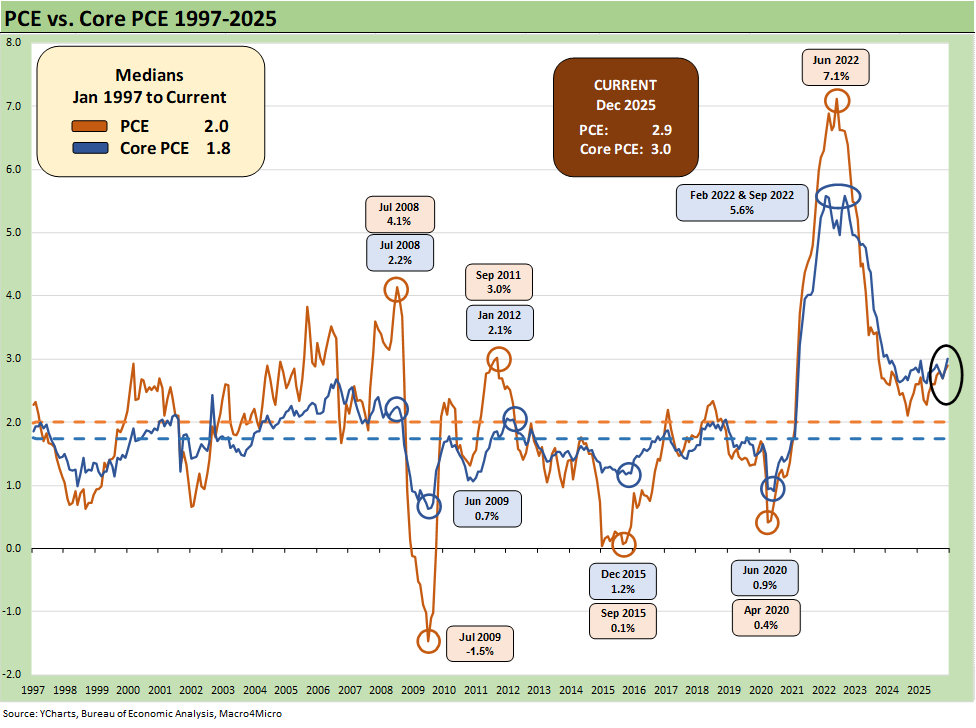

We include the 1997 to 2025 time horizon above for a good frame of reference on the PCE target of 2.0% that is routinely discussed by the Fed and in the markets. The shorter timeline from 1997 offers a better visual scale separate from the wild 1970s and 1980s.

Debate in financial and economic circles rage on around whether the Fed inflation target should be 2.5% or 3.0% or some other number. The above chart offers a reminder of how hard it is to get to 2.0% or below for headline PCE or core PCE. The earlier chart from 1972 covers the timeline from the inflationary/stagflationary periods of 1973 to 1982 to hammer that home.

The “1997 to 2025” period presents a rare stretch at or below the 2.0% PCE line and core PCE median as noted in the chart. It took a lot to go wrong in that time horizon to cross that 2.0% threshold. The events along the way included tech bubbles bursting in 2000-2001, oil crashes in the late 1990s and the late 2014 to early 2016 period, and a systemic bank system crisis from 2008 to 2011 (including sovereign stress) to get us there. The COVID pandemic in 2020 was a new one for the modern capital markets.

In the above timeline, we even see deflation in the post-crisis recession trough in mid-2009. The collapse in oil prices in late 2015 and then the COVID impact in 2020 gave an assist to low PCE. Oil is a big headline mover whenever there is a sharp decline or spike, and we have had plenty of both.

It is interesting that the topic of the Feb 2022 invasion of Ukraine and ensuing oil and gas spike never seems to find a way into the Trump and MAGA rhetoric on inflation in 2022. That was a major factor in inflation, but the economic reality of the Russia relationship did not serve the domestic political priorities of Team Trump in assigning any blame there for inflation.

The Biden politics and stimulus policies definitely had a major adverse inflationary impact on pricing and supply-demand imbalances after COVID. That is also the case with the Russian invasion of Ukraine.

Gasoline has been in deflation mode for part of 2025, and that helped dampen the inflation headline numbers. As 2025 wore on, energy inflation has gone the other way and notably in areas such as electricity and piped utility gas (see CPI Jan 2026: Reassuring Numbers, Missing Pieces 2-13-26, Simplifying the Affordability Question 11-11-25, Retail Gasoline Prices: Biblical Power to Control Global Commodities 11-13-25).

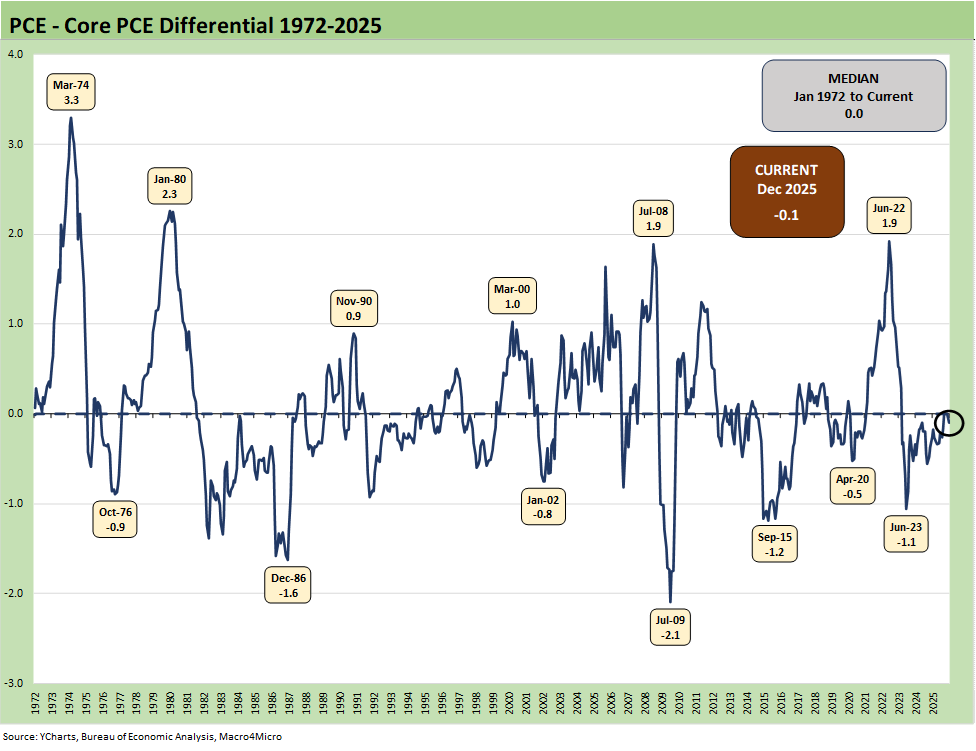

The above chart frames the long-term differential history between PCE and core PCE since 1972. The long-term median differential is zero and we are currently at -0.1%. The volatility around that compressed long-term median ties into the energy wildcard with some food distortions also back in the 1970s. We look at some of the CPI energy and food inflation moves in separate commentaries (see Inflation: The Grocery Price Thing vs. Energy 12-16-24, Inflation Timelines: Cyclical Histories, Key CPI Buckets11-20-23). Food and electricity inflation have been near the top of the affordability political rage-fest.

The above chart updates the trend line in disposable personal income (DPI) vs. personal consumption expenditures (PCE) that we get with each monthly PCE release. When PCE growth exceeds DPI growth, the conclusion is that the consumer is feeling good or tapping credit cards by necessity (e.g. the PCE could be outsized health care premiums).

The stimulus overload of 2021…

The 2021 period was a big macro rebound in GDP off the COVID peak period. The strong macro backdrop in 2021 and heavy dose of fiscal accommodation did not mesh well with residual supply-side shortages in goods broadly as 2022 saw the end of ZIRP and a material inflation spike.

Oil was a problem after the Putin invasion of Ukraine in late Feb 2022, and inflation hit a high in June 2022 at +9.1% for CPI as a headline grabber (headline PCE at +7.1% in June 2022) before the steady inflation slide to current rates. Core PCE had dueling peaks at +5.6% for Feb 2022 and Sept 2022.

The above chart plots MoM Disposable Personal Income vs. PCE and offers a read on how wild things got during and right after the pandemic peak. This is a chart we use each month to revisit the DPI swings that came with the three COVID relief/stimulus packages. That included two under Trump and one under Biden.

The COVID relief binge…

As a reminder, Trump signed the CARES Act in March 2020 (shows up in the DPI in April 2020) and Trump also signed the Dec 2020 legislation disbursed in Jan 2021 (Trump seldom mentioned that Dec 2020 one since it was easier to blame Biden and Powell). Biden signed the America Rescue Plan (disbursed in March 2021) that was a demand pile-on (we would argue over the-top-stimulus) in a supply-constrained environment (thus inflation). The DPI and PCE wave tied to each of those shows up in the chart above.

As a reminder, the vaccine was announced in early Nov 2020 just ahead of two stimulus actions. That was soon to be a factor in PCE patterns and lag effects. The quarterly GDP numbers in 2021 on the post-COVID bounce were numbers generally not seen since the Reagan and Clinton years (see Presidential GDP Dance Off: Clinton vs. Trump 7-27-24, Presidential GDP Dance Off: Reagan vs. Trump 7-27-24).

COVID was a distinct period for supply chains and supply-demand imbalances. With tariffs and potential trade wars, it will remain important to look for similar imbalances whether in narrow product categories or in broad commodities and materials areas. So far, the major trade partners have not initiated much in retaliation with the exception of a brief China spat. That has mitigated the damage but that de facto submission could come back to haunt some major trade partners if others run for office with a “get tough” election pitch.

Jacking up aluminum, steel, copper on the materials side and seeking even more tariffs on lumber was not and is not a great idea for keeping prices and costs contained. Auto tariffs under Section 232 are extreme even after the array of “deals” and could go higher if the USMCA breaks down in 2026. We saw semis, pharma, and aircraft/engines/parts added to the Section 232 pipeline although most of the aircraft/parts risk was mitigated in EU talks. Recent period brought in commercial vehicles, branded pharma, cabinets, and a range of targets on national security grounds including upholstered furniture.

The IEEPA tariffs were just struck down by the Supreme Court in a 6-3 vote (Thomas, Alito, and Kavanaugh dissent). That will change the dynamics of trade deals from here even if Team Trump has been contingency planning. There are other trade and tariff remedies but we don’t expect those will cover threatening Europe with tariffs if they do not allow annexation of Greenland or hitting Brazil with massive tariffs for jailing Trump’s “coup bro.” Those tactics should be over.

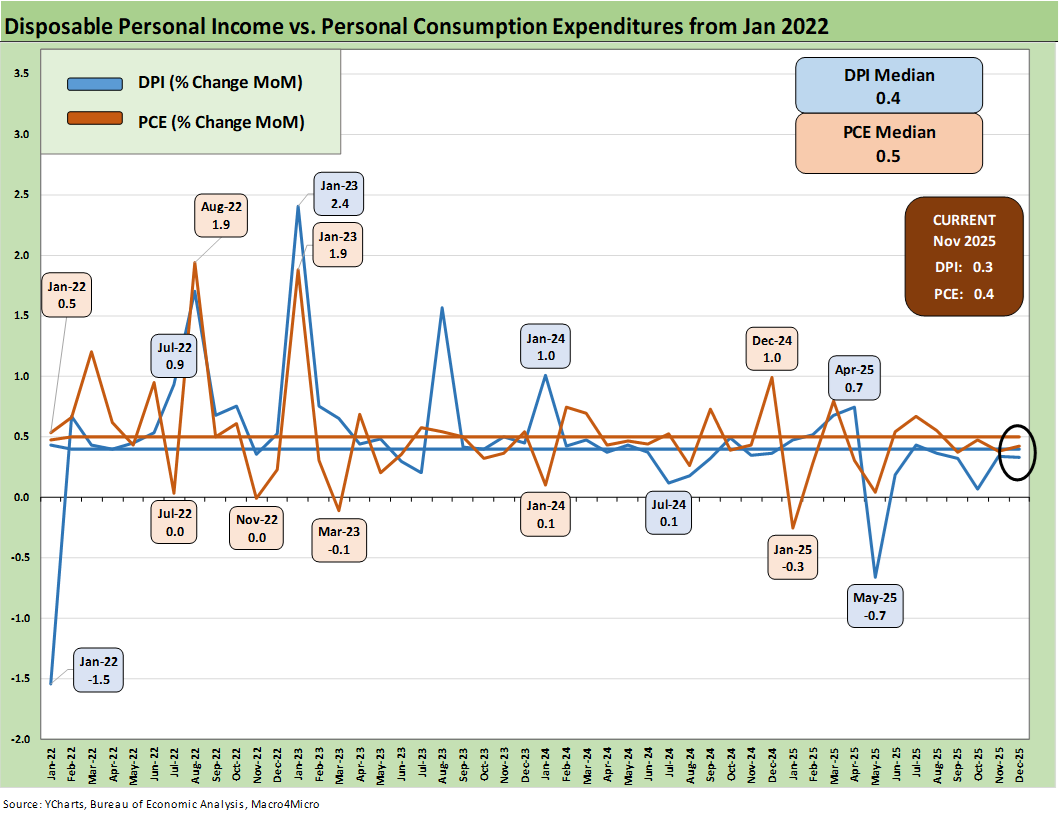

The above chart covers the time horizon for DPI vs. PCE from early 2022 as the tightening cycle kicked into gear after March 2022. Life in Jan 2022 was still quiet for Disposable Personal Income. We like to include this and the prior chart just given the heavy mix of disinformation and politically axed story lines we constantly hear from Trump on Biden being the cause of all the macro problems at the end of 2025.

Accurate factual and conceptual frameworks of “the now” matter more than qualitative political spin looking backwards. That said, having a sense of what the numbers were then helps clear up the misinformation nonsense. After all, this is a very different world of tariffs and top-down government policy with very different tax structures and priorities.

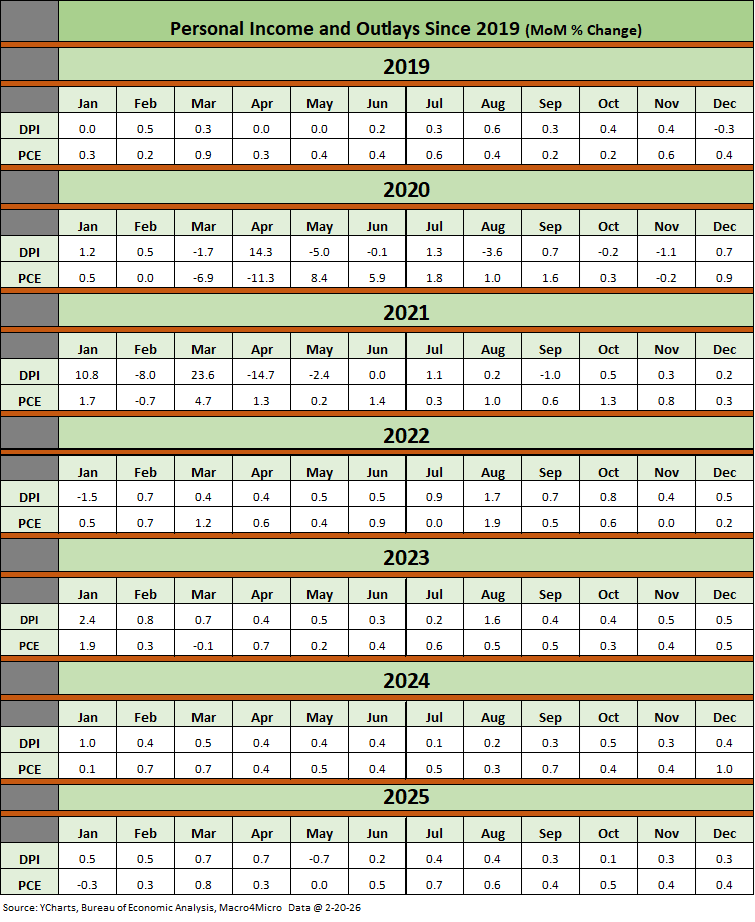

The above table plots the monthly Disposable Personal Income MoM change numbers vs. the Personal Consumption Expenditure MoM numbers across the years from 2019 through Dec 2025. It is an easy scan across key time periods for a look at turning points in DPI (e.g. stimulus payments) or PCE.

One exercise to do from time to time is to look at Table 1 in the monthly PCE release for the granular dollar amount on each DPI reconciliation line. The line items can sometimes show some volatility. We like to look for gaps between DPI and PCE and moves in Personal Savings.

Any reader of Table 1 can simply tick off which lines might come under pressure in coming months. Examples include expense lines such as Medicaid (post tax bill) or other health care premiums under ACA. There is also the recurring pressure on select durable goods that face tariffs.

It is always worth remembering that a tariff is a regressive tax that hits lower income consumers harder and the same for small businesses. The same is true in Medicaid costs based on the income brackets of Medicaid users. A loss of health care benefits and higher pharma costs is a zero-sum game with other consumption lines. The current ACA premium spikes will also be a zero sum “game” for many budgets.

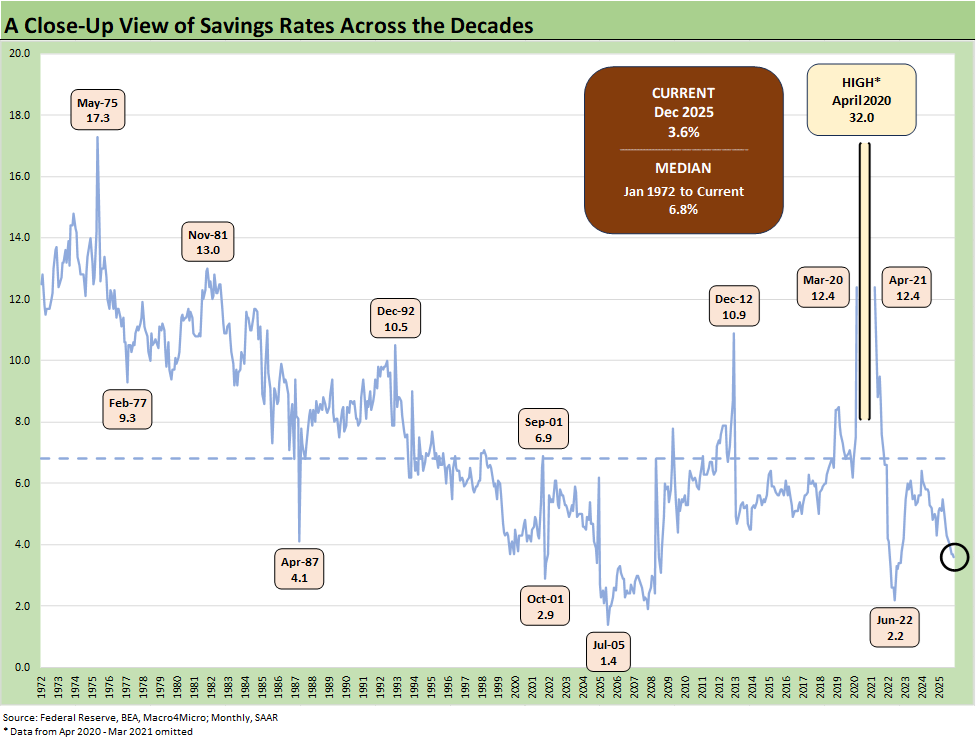

The above chart updates the savings rate history with the latest number down slightly to 3.6% after 4.9% as recently as May (as revised). We have looked at the savings rate dynamics in earlier commentaries (see Savings Rates: Context Across the Cycles 10-27-23). Savings rates peak in times of worry (occasionally panic) as evident in the chart above. As of now, households are clearly spending even if some more come to regret it when credit card bills come due.

The period leading into May 1975 was no picnic after the massive stagflation bout and the same was true in Nov 1981. Dec 1992 had a raft of issues as the commercial real estate bubble was bursting (and hammering some banks), the leveraged finance boom was on the back end of the default cycle, the thrift crisis effects were still playing out across some major regional economies (notably TX and CA), and the regional oil patch pain that had come home to roost in 1987-1990 was lingering.

See also:

4Q25 GDP (Advance Est.): Less Distortion This Time 2-20-26

2025 trade Deficits: Reality vs. Rhetoric 2-19-26

Industrial Production Jan 2026: Capacity Utilization Trends 2-19-26

Home Starts Dec 2025: Wrapping a Weak 2025 2-18-26

Market Lookback 2-17-26

Market Commentary: Asset Returns 2-16-26

CPI Jan 2026: Reassuring Numbers, Missing Pieces 2-13-26

Existing Home Sales Jan 2026 2-12-26

Payrolls Jan 2026: Into the Weeds 2-11-26

Employment Jan 2026: Good Headline, So-So Mix 2-11-26

Retail Sales Dec 2025: Muted Year-End 2-11-26

Market Lookback: Monkey Business 2-9-26

Switzerland-US Trade: A Deficit that Glitters 2-3-26

US-Taiwan Trade: Risks Behind the Curtain 2-1-26

Trade Deficits: Math Challenge 1-30-26

China Trade: Shrinkage Report 1-28-26

Mexico Trade: Gearing up for More Trade Trouble? 1-27-26

Canada-US Trade: Trump Attack N+1 1-25-26

PCE Income & Outlays Nov 2025: Resilient Consumer, Higher Inflation 1-24-26

Policy Mud on the Wall: Consumer Debt, Residential Mortgages 1-15-26

2025 Spread Walks and Multicycle Return Histories 1-5-26

Annual Return Differentials: HY vs. IG Across the Cycles 1-3-26