Retail Sales Dec 2025: Muted Year-End

December retail sales close out 2025 on a soft note, with headline flat and core slipping a little.

The holiday season delivered in aggregate, but 2025 brought on a fresh round of tariff-related caution, pull-forward effects, and a widening K-shaped split in consumer behavior with consumer asset quality metrics starting to falter.

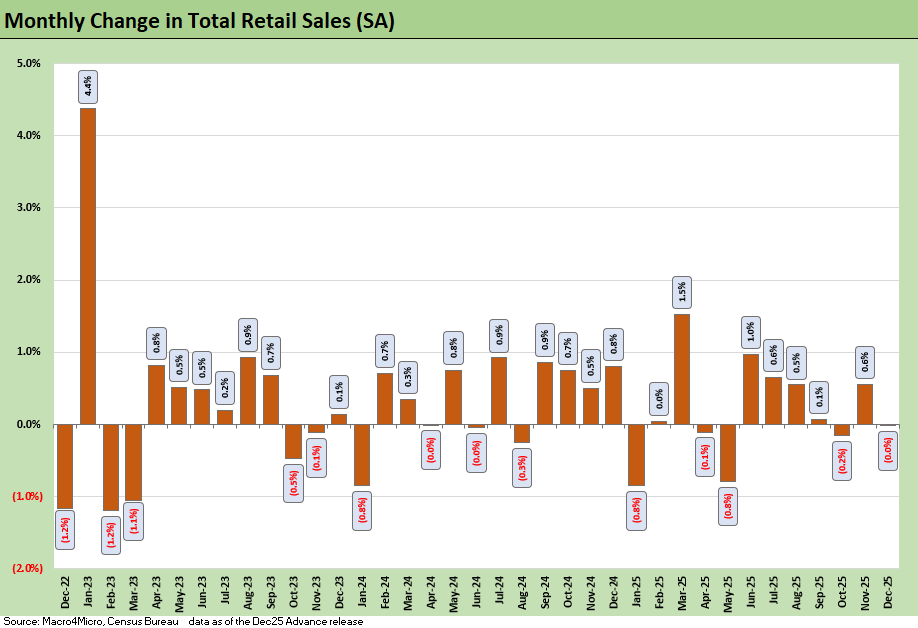

Total retail sales were flat MoM in December with core retail sales slipping -0.1% MoM. This follows a strong November and could point to more of a holiday anomaly after some some pull-forward effects as consumer activity broadly had remained robust later in 2025.

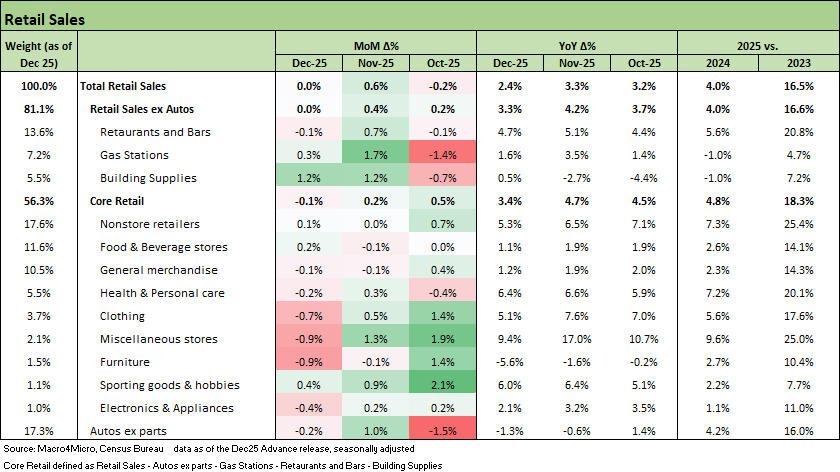

The underlying detail has few bright spots with discretionary and nondiscretionary categories alike showing up as negative in the month. Larger purchases like furniture (-0.9%) and appliance spending (-0.4%) continue to underperform.

Full-year retail sales rose about 4.0% in 2025, a clear slowdown from post-pandemic growth but still indicative of moderate nominal expansion. That growth was uneven, with core categories like nonstore retail, health and personal care, and miscellaneous stores doing most of the work. Tariff exposure and elevated cost pressures leave us cautious about extrapolating that strength into a broad-based consumer recovery. Payroll numbers and CPI will provide more input this week.

We enter 2026 with consumer behavior continuing to pose questions around durability of spending as the K-shaped nature of the economy will remain pronounced. Even with the tax refunds set to bolster consumer liquidity and balance sheets at the start of the year, the increasingly fraught labor market and stickier above target inflation leaves 2026 starting on fragile footing.

The monthly changes to headline retail sales above show the volatile holiday season with December coming in soft after the November holiday lift. Given the level of promotional activity throughout the quarter, price sensitivity likely drove a front-loaded holiday season, leaving December to reflect a softer, post-promotion run rate. It does not read as a collapse, and the coming months will offer better evidence. Looking beneath the headlines shows Core retail down -0.1% MoM in a step down from stronger October and November results.

As we have watched tariffs closely throughout the year, the most notable impact on consumer spending habits has been behavioral. Even without a price shock for select product segments, policy uncertainty earlier in the year encouraged pull-forward dynamics and more selective purchasing behavior. Coming into the year-end, the heightened preference for promotions and some signs of hesitancy to over-stretch balance sheets amidst such uncertainty seems to have taken hold again. We see this especially as we look at the yearly numbers where we see a lot of bigger ticket purchases lagging the headline numbers.

The above breaks out the underlying categories alongside the ex-autos and core retail changes. The headline is bolstered this month by another respectable bump to Building Supplies at +1.2% but that is just barely enough to eke out a positive result when framed against Dec 2024 (+0.5%).

Within core categories, the only positives show a continued upward trend for sporting goods & hobbies (+0.4%) and smaller positives for food & beverage stores (+0.2%) and nonstore retailers (+0.1%). We see some pullback in some more discretionary items like clothing (-0.7%) and miscellaneous stores (-0.9%) that reflect more of the pull-forward theme after a strong November.

On a full-year basis, the contrast in 2025 starts to become clearer and signals to us where uneven growth points to a less healthy consumer than headline suggests. The 2025 growth is led by nonstore retailers at +7.3%, health & personal care at +7.2%, and miscellaneous stores at 9.6%. Growth in these areas contributed the lion’s share of the core retail strength for the year and there was a notable lack of growth for big ticket items.

Taken together with bank earnings commentary, this mix continues to reflect a K-shaped consumer shaped by tariff-related uncertainty. Higher income households continued to spend enough on “experiences” and discretionary goods to paint a positive picture. Lower-income brackets leaned heavily on promotions and timing, avoiding larger purchases and leading to more volatility as conditions and sentiment ebbed and flowed throughout the year.

Zooming out, this print does not give a clear new signal but the setup for 2026 is increasingly mixed as the 2025 data closes out. The marginal contribution from retail sales narrowed at year-end, but with enough mitigating factors to warrant caution in over-interpreting a single month. All eyes will instead be on the delayed payrolls release tomorrow and CPI to get a fresh read on Fed actions.

See also:

Market Lookback: Monkey Business 2-9-26

Market Commentary: Asset Returns 2-8-26

Switzerland-US Trade: A Deficit that Glitters 2-3-26

US-Taiwan Trade: Risks Behind the Curtain 2-1-26

Market Commentary: Asset Returns 2-1-26

Trade Deficits: Math Challenge 1-30-26

China Trade: Shrinkage Report 1-28-26

Mexico Trade: Gearing up for More Trade Trouble? 1-27-26

Canada-US Trade: Trump Attack N+1 1-25-26

PCE Income & Outlays Nov 2025: Resilient Consumer, Higher Inflation 1-24-26

3Q25 GDP: Updated Estimate 1-22-26

Industrial Production Dec 2025: CapUte Resilience 1-17-26

Existing Home Sales Dec 2025: Getting up off the Mat? 1-16-26

Policy Mud on the Wall: Consumer Debt, Residential Mortgages 1-15-26

CPI Dec 2025: Sideways Calms Nerves – For Now 1-13-26

Payrolls Dec 2025 and FY 2025: Into the Weeds 1-10-26

JOLTS Nov 2025: Job Openings and Hires Down, Layoffs Lower 1-7-26

2025 Spread Walks and Multicycle Return Histories 1-5-26

Annual Return Differentials: HY vs. IG Across the Cycles 1-3-26

Total Return Quilt Across Asset Classes 2008-2025 1-2-26

Cyclical Histories: Will Facts Be in Vogue in 2026? 1-2-26

3Q25 GDP: Morning After Variables to Ponder 12-27-25

Durable Goods Oct25: Core Capex Still in Gear 12-23-25

Market Lookback: Last Call for Unusual Behavior 12-22-25

3Q25 GDP: Morning After Variables to Ponder 12-27-2

|

|

The gap between consumer sentiment and actual spending is finally starting to close, and not in a great way. With retail sales flattening out, the growth story for 2026 is getting much harder to tell. I just shared some data on this in my latest brief. If you're interested in the consumer side of macro, I'd appreciate a follow or subscribe