4Q25 GDP (Advance Est.): Less Distortion This Time

In a year of wild distortions from tariff pre-buying and working capital swings, the 4Q25 GDP is back to basics ex-Govt shutdown.

On a day when GDP came in weaker and PCE price inflation came in higher, the story is still in the line items and not the headline numbers.

The 4Q25 GDP numbers were materially less distorted than 1Q25, 2Q25, and 3Q25 when the net export line and investment in inventory injected major plus and minus impacts on headline numbers (see 1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25, 2Q25 GDP Final Estimate: Big Upward Revision 9-25-25, 3Q25 GDP: Morning After Variables to Ponder 12-27-25).

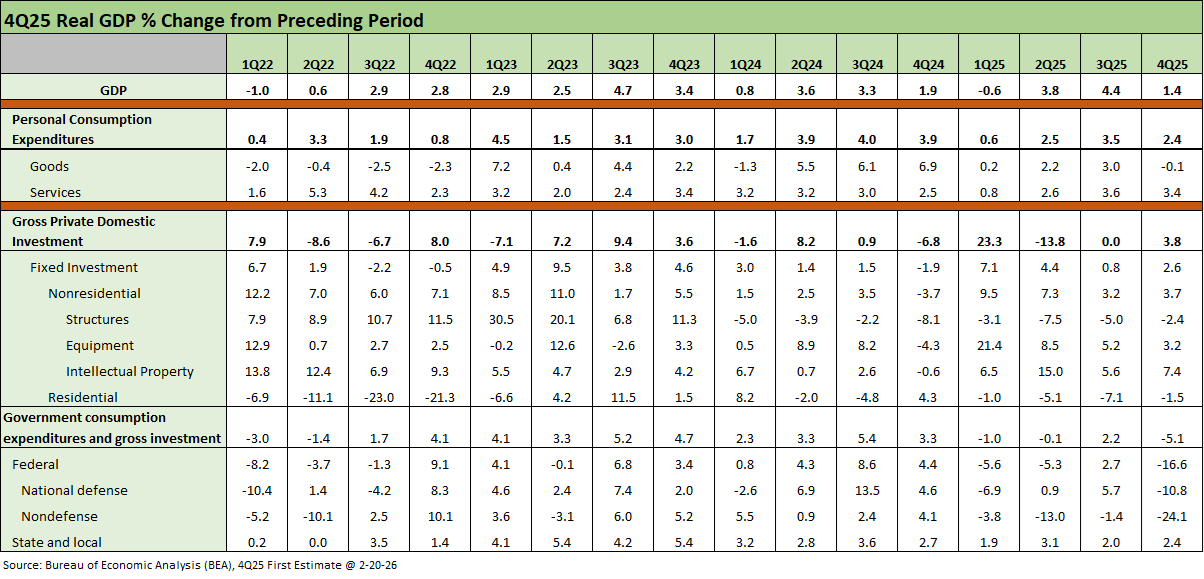

An exception to the better comparability across quarters for the core GDP lines was Government consumption and investment growth that weighed in at -5.1% with Federal at -16.6% in GDP and State and Local at +2.4%.

With Personal Consumption Expenditures (PCE) at 68% of total GDP, the +2.4% PCE growth was weaker than 3Q25 and 2Q25 and well down from +3.9% in 4Q24 and +4.0% of 3Q24. The 1Q25 period was the worst PCE quarter at +0.6%.

Fixed investment at 17.6% of GDP generated +2.6% before the Federal government shutdown was essentially N/A for the 4Q25 period at -16.6%. State and Local (1.7x the size of Federal) posted +2.4%.

If you believe we now are operating in a new millennium that is a 2% handle annual growth period for the US with its overleveraged Federal government and demographic profile (that is what we believe), the 4Q25 period was a normal set of numbers for GDP even if the distortions (notably net exports and inventory) can swing around from quarter-to-quarter (just not in 4Q25).

The 4Q25 headline GDP had less noise from tariff swings and working capital management chaos. For net exports of goods and services, the contribution to GDP was only +0.08% in 4Q25 vs. +1.62% in 3Q25, +4.83% in 2Q25, and -4.68% in 1Q25. The pre-buying binge ahead of tariffs in 1Q25 was one for the ages and reversed as the year went on with the change in private inventories for 4Q25 at +0.21% vs. -3.44% in 2Q25 and +2.58% in 1Q25.

We typically lock in on PCE given its scale in the GDP (68%) and the various fixed investment lines (almost 18% of GDP). In fixed investment, the mix of structures, equipment, intellectual property products, and residential investment are where some of the main cyclical and growth indicators live.

In PCE, Goods PCE posted -0.1% growth with durables at -0.9% and nondurables at +0.4%. That is not pretty. Services was +3.4%. Over in the PCE inflation data also released this morning, Goods inflation was +1.7% YoY while Services was +3.4% YoY. PCE inflation was +2.9% and Core was +3.0%. That is a mediocre backdrop.

Noise reduction…

The lower level of noise in 4Q25 will not stop the White House from doing their usual Watusi around nominal GDP, annualized quarters, etc., instead of sticking to the historical real GDP growth line items (note: anything to avoid rational, fact-based historical comps). The new world of record budget deficits and high tariffs is challenging, especially coming off the second high-inflation period since the Carter and early Reagan years.

When you are running with the “greatest economy in history” story line, numbers can be the enemy whether for that recurring claim in Trump 1.0 or for the “greatest first year in Presidential history” this time around (see Trump’s “Greatest Economy in History”: Not Even Close 3-5-25). Clinton and Reagan would certainly question that view (see Presidential GDP Dance Off: Clinton vs. Trump 7-27-24, Presidential GDP Dance Off: Reagan vs. Trump 7-27-24 ). Even Carter fans might raise their hands (see Payroll % Additions: Carter vs. Trump vs. Biden…just for fun 1-8-25, Annual GDP Growth: Jimmy Carter v. Trump v. Biden…just for fun 1-6-25).

In many ways, the party in charge might not matter in the new millennium low growth period since the challenges are a long list. The tariff policies and magnitude of the political and social divisions just make life more difficult to execute on policy in Congress in a world of “government by executive order.” That said, as we go to print, the Supreme Court just ruled against Trump’s IEEPA tariffs…we’ll tackle this separately. It will be interesting to see how refunds vs. new tariffs work in practice.

See also:

3Q25 GDP: Updated Estimate 1-22-26

Cyclical Histories: Will Facts Be in Vogue in 2026? 1-2-26

3Q25 GDP: Morning After Variables to Ponder 12-27-25

2Q25 GDP Final Estimate: Big Upward Revision 9-25-25

1Q25 GDP: Final Estimate, Consumer Fade 6-26-25

1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25

Trump’s “Greatest Economy in History”: Not Even Close 3-5-25

Gut Checking Trump GDP Record 3-5-25