CPI Jan 2026: Reassuring Numbers, Missing Pieces

We look at a good headline month for CPI, but there are still a lot of trends to annoy consumers (and voters) when you get in the weeds.

Show me the health care insurance inflation.

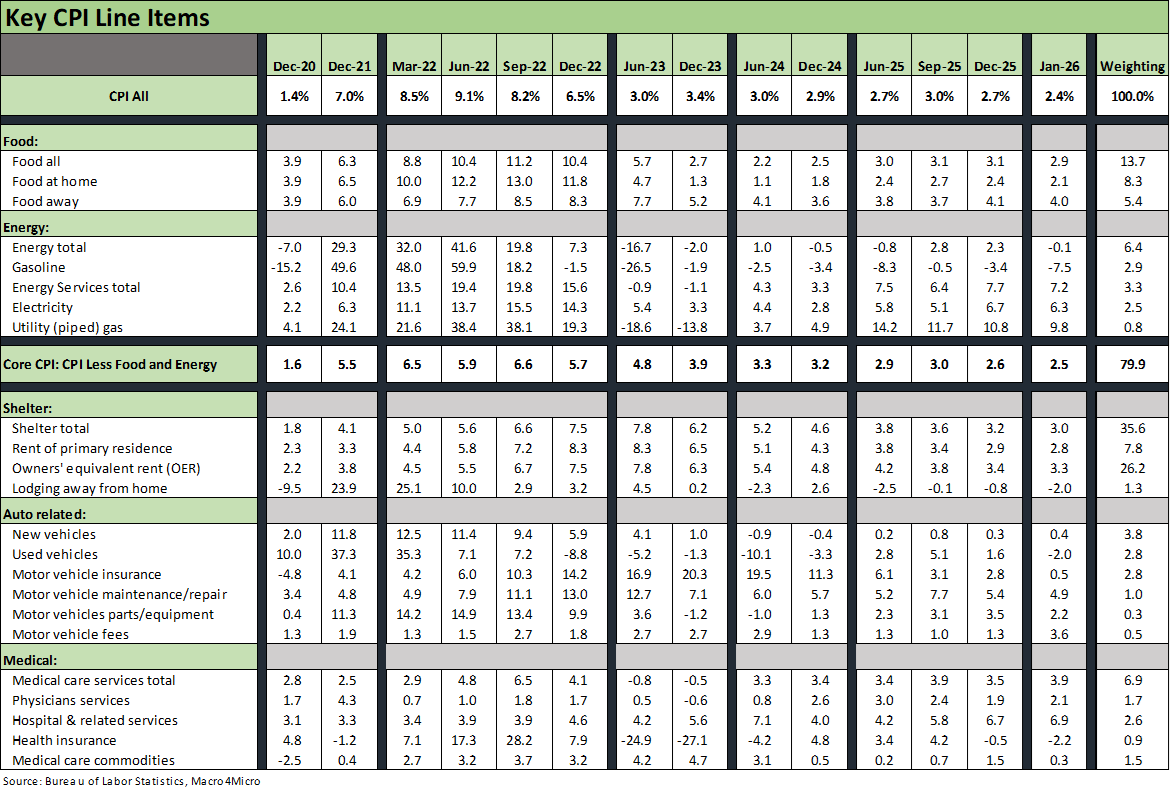

The overall CPI picture brought good news just by going down to 2.4% in total (vs. 2.7% in Dec 2025) while core CPI weighed in at +2.5% (vs. 2.6% in Dec 2025). As the Washington noisemakers turns up the volume (as usual), the reality is that +2.4% by definition means aggregate prices are rising (that is why they call it inflation – even when it is low). The good news is that inflation is slower than wage growth as covered in the CPI report as well as the 4Q25 Employment Cost Index report this week.

A granular dive into CPI lines still reveals pockets of affordability pain in areas that matter to consumers (and voters). The partisan talking heads on the right will run right past those lines. The partisans on the left will scream affordability problems even with lower CPI. The fact is the Jan 2026 CPI numbers mark an improvement in aggregate for consumers with pockets of bad news as well. What manufacturers and service providers had to “eat” in tariff costs lurks behind the CPI metrics.

Some CPI lines reveal a disconnect between the BLS methodology and household cash flow reality. A notable example is Health Insurance premiums as a headline topic and household crisis for many. Health Insurance weighed in for January at -2.2% YoY and -1.0% MoM from Dec 2025. As in housing and the infamous OER metric, the BLS has its own distinctive approach to measuring health insurance CPI. We have not yet seen much debate around BLS measurement on health care “deflation” of Jan 2026. Households often live in a cash-in, cash-out world and the OER metrics in housing and health insurance CPI levels are in a different world.

As we detail below, the Medical Care Services line is creeping higher with lines such as “hospital and related services” at 6.9% YoY, “inpatient services” at 7.4%, “dental services” at 5.3%, and “home health care” at 12.7%. We also saw some below-the-headline CPI metrics such as “water, sewer, and trash collection” at 4.7%, “motor vehicle maintenance and repair” at 4.9%, and “postage and delivery” at +5.3%.

Scrolling the columns of CPI can be depressing for many consumers and at times surprising since they are not as well-known as the grocery aisle prices (beef and veal at +15.0%, fresh fish and seafood at 5.7%, coffee at 18.3%, sugar and sweets at +5.7% with candy and chewing gum at 7.5%, etc.).

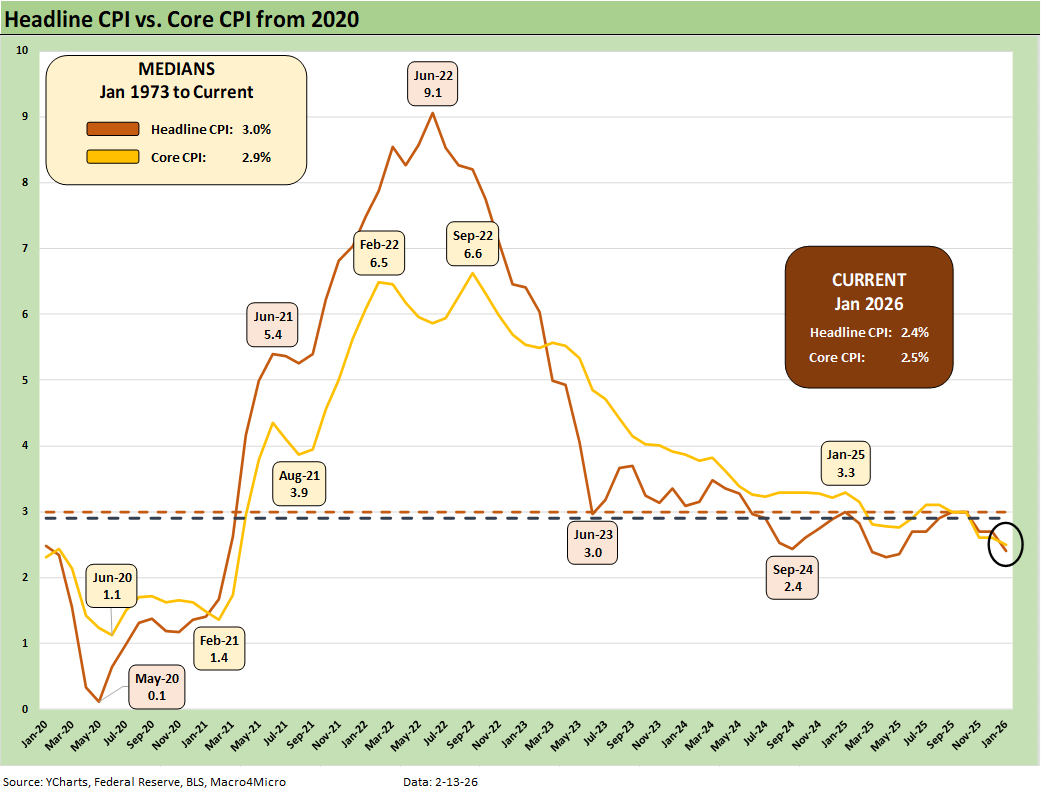

The above chart runs through the time series for Headline CPI and Core CPI since the start of the COVID year of 2020. By the numbers, the current +2.4% headline CPI is back around a recent Sept 2024 low point noted in the chart.

The time series offers a reminder of the multiple market imbalances that drove the CPI spike in the aftermath of COVID supply crises teamed up with excessive stimulus action.

The chart also offers a look at the first major inflation spike since 1979 brought Volcker into the job by August that year. That period rolled into the mother of all tightening and a double dip stagflation cycle that crushed many bellwether companies.

The pace of the decline in CPI across 2023 really stands out in the chart with the economic expansion continuing and regular record stock market highs into 2024. Those topics tend to not get much mention.

While Trump was slamming Powell and Biden as the most destructive creatures since the primordial soup, the fact is that Biden was only the second President in 50 years to get through his term with no recession months. Clinton was the other recession-free President across two terms but with much better headline and PCE growth years to boast (see Presidential GDP Dance Off: Clinton vs. Trump 7-27-24).

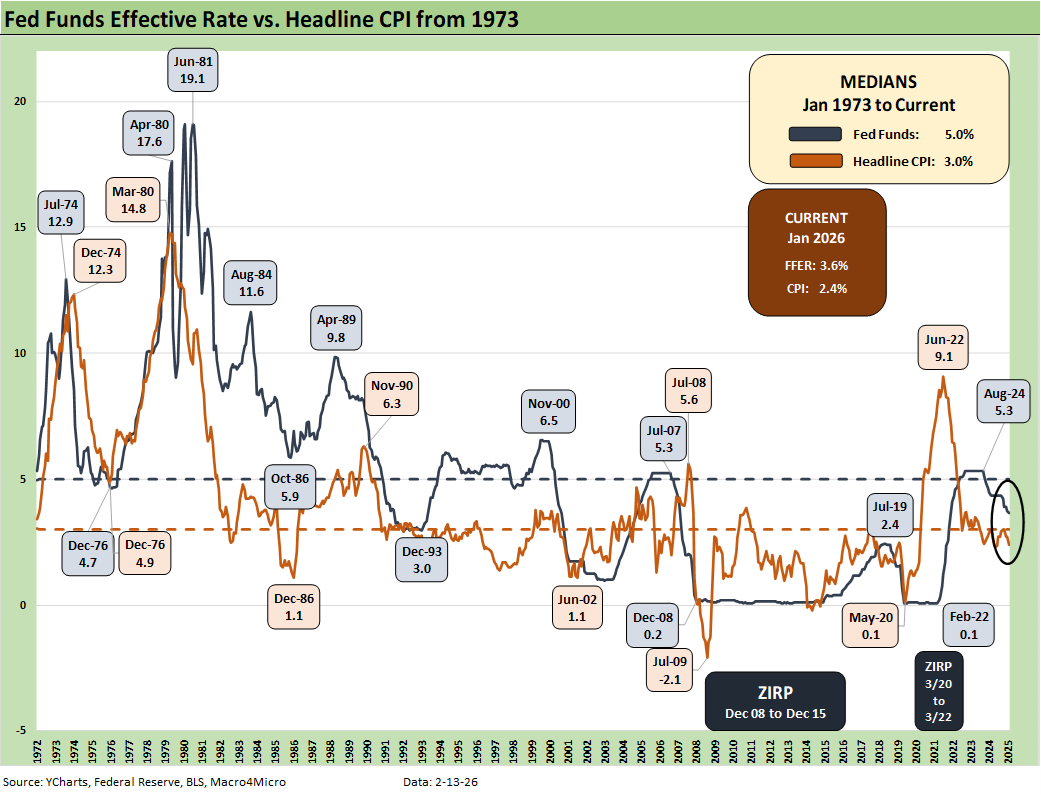

The above chart gives the longer-term history from the bad old days of oil embargoes (late 1973/early 1974) and the late decade stagflation and Volcker. We detail the fed funds rate and headline CPI. The earlier data of the 1970s and early 1980s uses weekly averages, so you don’t see some of the brief 20% fed funds days of that tightening cycle. We cover those histories in some links at the bottom of this commentary.

I occasionally highlight that I arrived in NYC to start work in the month the Misery Index hit 22%. In that context, 2022 looks mild. The CPI and PCE levels quickly corrected into 2023 and into 2024. Powell and the FOMC should be praised for that even if they justifiably can take heat for waiting too long in 2021.

Those who call 2022 “the worst inflation in history” are simply ignorant and/or dishonest (i.e. partisan idiots). The US did not even have a recession in 2022. PCE (consumption) remained high and unemployment low.

The 1980-1982 double dip was a radically different backdrop than 2022 (see Unemployment, Recessions, and the Potter Stewart Rule 10-7-22). The lack of a recession in 2022-2023 was a testament to the diversity of the US economy and the resilience of the consumer. That appears to be playing out again in 2025-2026 even with some mild signs of weakening payroll indicators and despite damaging tariff distortions.

The economic signals may be mixed, but growth is steady even if the White House does not make reality adjustments for the GDP growth rates it cites (see Cyclical Histories: Will Facts Be in Vogue in 2026? 1-2-26, 3Q25 GDP: Morning After Variables to Ponder 12-27-25).

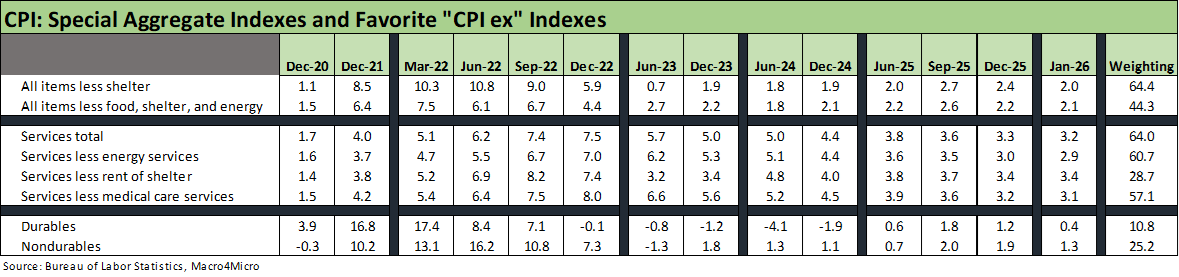

The above table breaks out some of the special aggregate CPI metrics that slice and dice the high-level index metrics to adjust for some outsized sectors (e.g. ex-shelter). The special index aggregates also narrow in on some key subsector lines (e.g. Services total, Durables, Nondurables). A few more angles on the big picture are always useful. We select some key quarter end dates to fit more data in the table. We had to leave some out.

The takeaway from these Table 3 adjusted CPI metrics bring good news after a stretch in 2025 that saw some unfavorable moves. “All items less shelter” is our favorite, and that CPI measure had trended down nicely into Jan 2026 after moving higher from +1.9% in Dec 2024 to +2.7% in Sept 2025 as shown in the chart. This metric in Jan 2026 at 2.0% is still above 2023-2024 but moving in a better direction.

Services total at +3.2% remains a headache in a services economy such as the US as the “Services” special index comprised 64% of CPI. At +3.2%, the Services CPI is now well below 2023 and 2024. The Services CPI is improving from the higher 3% handle numbers seen in 2025. This category is a win for Trump’s CPI metrics.

We see Durables trending lower, which in turn pushes back on the adverse tariff scenarios. Even in that case of good news for Durables inflation, consideration has to be given to cyclical demand trends or the potential margin erosion of the importer/buyer and the need to “eat the tariff cost” from the supplier chain. That can be a major risk from materials and components in the supplier-to-OEM chain.

If Trump crushes Canada or Mexico in the upcoming USMCA review, the downstream buyers may need to review their pricing strategies in 2026. People who pretend the tariff debate is over are engaged in wishful thinking. There is a lot of trade noise and decisions ahead.

The Big 5 buckets are broken out above. These 5 groupings dominate the CPI weighting with shelter at a disproportionately high 35.6% weighting in the CPI. As noted in the table, food and the total mix of auto lines are a distant second and third.

Shelter CPI stubborn as measured by BLS…

As covered in numerous past commentaries, the Shelter CPI is heavily influenced by a derived metric called “Owners’ Equivalent Rent” that is over 26% of the total CPI. The disconnect from cash reality is that a homeowner with a low 3% mortgage is not seeing his cash flow experience change as his home rises in value and his monthly payment remains unchanged. That homeowner is in fact seeing no change in his core shelter costs. That said, electricity, piped gas, insurance, furnishings, and the goods in the home are seeing price increases. The BLS does not use home prices and related financing costs in CPI since it changed its methodology back in the early 1980s.

Autos protected by OEM pricing and costly defense of retail markets…

We have put together a profile of Automotive sector CPI given its outsized role in household budgets (see Automotive Inflation: More than Meets the Eye10-17-22). We don’t include gasoline in the auto CPI since we have that over in Energy.

The good news for those buying new or used vehicles is that the new vehicle market has seen the OEMs step up to eat much of the tariff costs (for now) in the interest of preserving volumes and supporting dealers. That is likely to change gradually over time. GM especially has been active in planning to relocate production capacity to the US as additional measures to ease tariff margin pressures (see Credit Profile: General Motors and GM Financial 10-9-25).

Medical Care CPI rising while flawed health insurance metric “deflates”…

As noted above, the health care metrics come with some very big asterisks for health insurance inflation. We can’t wait for some White House talking heads to cite the deflation in health insurance as premiums spike. They would not be pressed by CNBC on the topic since CNBC wants to take share away from Fox News and keep the guests coming back.

As noted in the bullets, the Medical Care Services lines are troubling. While the headline “medical care services” line posts 3.9%, that includes -2.2% for “health insurance.” The BLS is not opening the mail for those seeing massive premium increases. We see 6.9% for “hospital and related services” with 7.4% for “inpatient services” within that group and 6.1% for “outpatient.” “Home health care” at 12.7% and 4.8% for “nursing homes and adult day services” also tell a story for the boomers and their families.

Energy always a mixed bag across oil, electricity, and piped gas…

Energy inflation gets simplified in political spin as being all about oil and gasoline, but the real challenge has been electricity and piped utilities gas. Total energy weighed in at -0.1% YoY but “Energy Services” (electricity and piped gas) posted 7.2% CPI with its 3.3% index weighting. The “energy commodities” (primarily gasoline) posted -7.3% CPI with its 3.1% index weighting. Oil and natural gas can swing around, but the power grid issues are not going away.

Food comes down to your menu choice…

Food inflation is currently at 2.9% and down from levels seen in 2025 . Food CPI is above 2024, so Trump does not have bragging rights on Food inflation. “Food at home” is notably higher now than in 2024 with the 1% handles of that year while “Food away from home” is more mixed.

The food lines can be a mix of entertaining and depressing, but there is quite a range. Beef and veal at 15.0% with fresh fish and seafood at +5.7% are hitting the protein menu while +18.3% for coffee and +7.5% for candy and chewing gum are undermining those of us more inclined to caffeine and sugar stimulus.

We see some food lines facing pressures on packaging material costs with 5% handles in numerous canned products. Recent exemptions still show up in the YoY numbers but are easing in MoM trends (“exemptions” are another admission by the White House that the “buyer pays’).

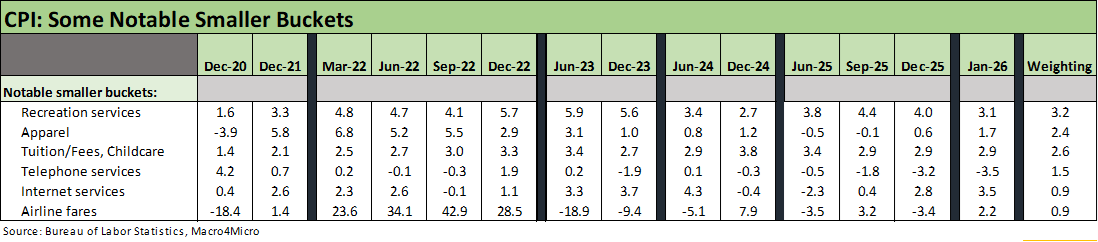

The above table is just an add-on to the main Big 5 groupings and bring the two prior boxes to around 87% of the CPI index. The mix in the table represents regular items for many households with 4 higher, 1 negative, and 1 flat. The decline in Recreation Services CPI is notable on the discretionary spending side. Apparel edged higher but remains low. All the tariffs slapped on low cost labor countries from Mexico to Asia will make that Apparel line an interesting one to watch.

Internet Services ticking higher with phones in deflation is another interesting twist on where the major providers are seeing pricing power (or a lack of in the case of telephones). Airline fares tie into jet fuel prices and passenger volumes, and we saw a rise in airline CPI.

See also:

Existing Home Sales Jan 2026 2-12-26

Payrolls Jan 2026: Into the Weeds 2-11-26

Employment Jan 2026: Good Headline, So-So Mix 2-11-26

Retail Sales Dec 2025: Muted Year-End 2-11-26

Market Lookback: Monkey Business 2-9-26

Market Commentary: Asset Returns 2-8-26

Switzerland-US Trade: A Deficit that Glitters 2-3-26

US-Taiwan Trade: Risks Behind the Curtain 2-1-26

Market Commentary: Asset Returns 2-1-26

Trade Deficits: Math Challenge 1-30-26

China Trade: Shrinkage Report 1-28-26

Mexico Trade: Gearing up for More Trade Trouble? 1-27-26

Canada-US Trade: Trump Attack N+1 1-25-26

PCE Income & Outlays Nov 2025: Resilient Consumer, Higher Inflation 1-24-26

3Q25 GDP: Updated Estimate 1-22-26

Industrial Production Dec 2025: CapUte Resilience 1-17-26

Policy Mud on the Wall: Consumer Debt, Residential Mortgages 1-15-26

CPI Dec 2025: Sideways Calms Nerves – For Now 1-13-26

2025 Spread Walks and Multicycle Return Histories 1-5-26

Annual Return Differentials: HY vs. IG Across the Cycles 1-3-26

Total Return Quilt Across Asset Classes 2008-2025 1-2-26

Cyclical Histories: Will Facts Be in Vogue in 2026? 1-2-26

Market Lookback: Last Call for Unusual Behavior 12-22-25

Some CPI Histories:

Inflation: The Grocery Price Thing vs. Energy 12-16-24

Inflation Timelines: Cyclical Histories, Key CPI Buckets11-20-23

Fed Funds – Inflation Differentials: Strange History 7-1-23

Fed Funds, CPI, and the Stairway to Where? 10-20-22