Existing Home Sales Sept 2024: Weakening Volumes, Rate Trends Worse

Existing Home Sales were down MoM and YoY while the strange combination of rising inventory and rising prices continue.

Strange times in existing home sales…

Inventories are higher (+1.5%) but still short of normal levels while prices are up (+3.0%) YoY for the 15th consecutive month even if down from the record levels of June 2024.

The short-lived affordability relief of lower mortgages faltered in recent weeks with soaring Sept payroll numbers, firm single family home starts and solid retail sales all pushing the long end of the curve higher (see Payroll Sept 2024: Rushing the Gate 10-4-24; Housing Starts Sept 2024: Long Game Meets Long Rates 10-18-24; Retail Sales Sep 2024: Taking the Helm on PCE? 10-17-24).

For September, the YoY decline in total existing home sales was -3.5% and -1.0% sequentially with October now under a darker cloud given the selloff of longer UST.

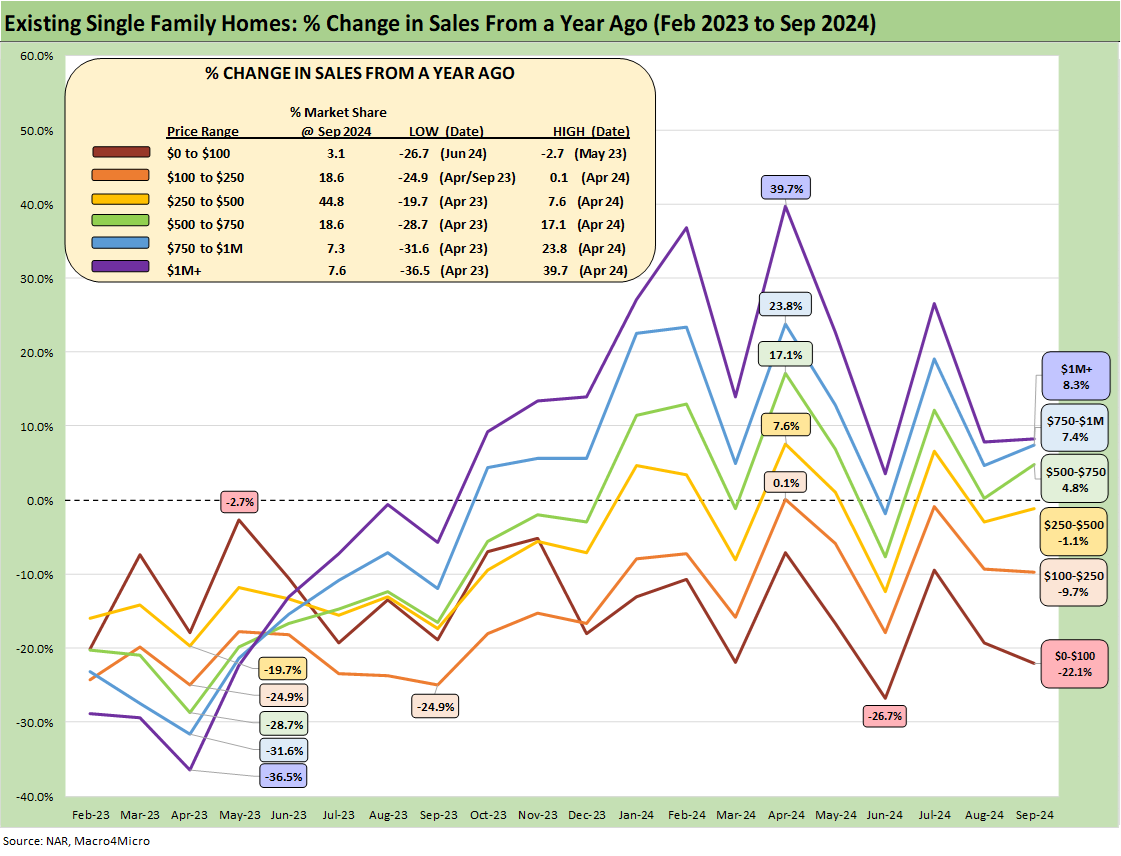

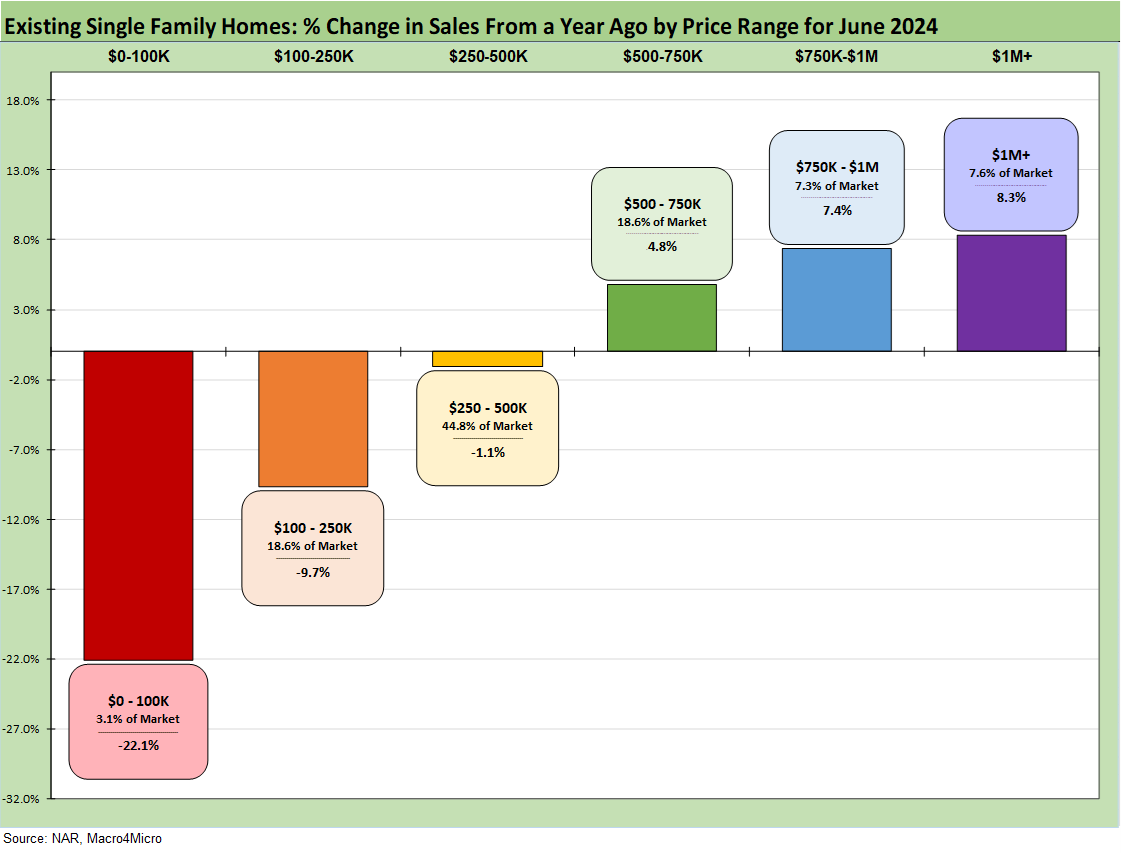

The trend line in existing home sales shows the 3 price tiers below $500K lower in volumes YoY with the 3 price tiers higher than $500K rising with higher increments moving up the price tiers. The important $250K to $500K tier was down by -1.1% (45% of total sales).

The above chart updates the time series on sales volume deltas by price tier. We look at the current mix in more detail in a chart further below. The trend shows the higher price tiers have declined since the summer peak but remain positive while the lower-price tiers are still struggling.

Well-heeled buyers have an easier time looking past the “locked-in effect” on current mortgages and many can plan on making a move and then consider refinancing later in a friendlier rate backdrop if that does come to pass. Many potential sellers with 4% and 3% handle mortgages have been tapping the brakes and have been slow to extract positive home equity in a sale of refi. Some had been expecting to move more quickly after FOMC easing, but the 10Y UST and 30Y mortgage rate have not been cooperating.

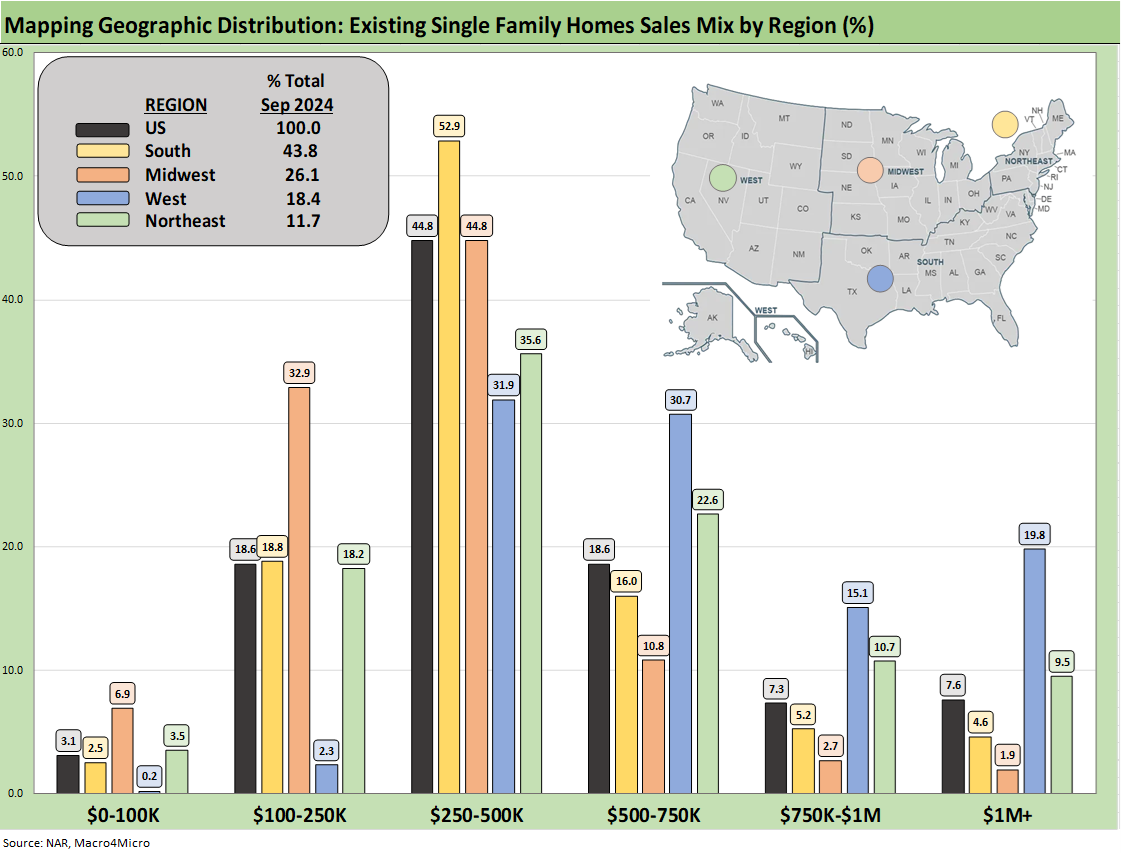

The above chart offers a reminder on the geographic mix of existing home sales volumes with some details on the price mix by region (as defined by the Census). As we covered in our earlier commentary on the Harris Housing plan, the South rules in the new and existing single family business (see Harris Housing Plan: The South’s Gonna Do It Again!? 8-28-24).

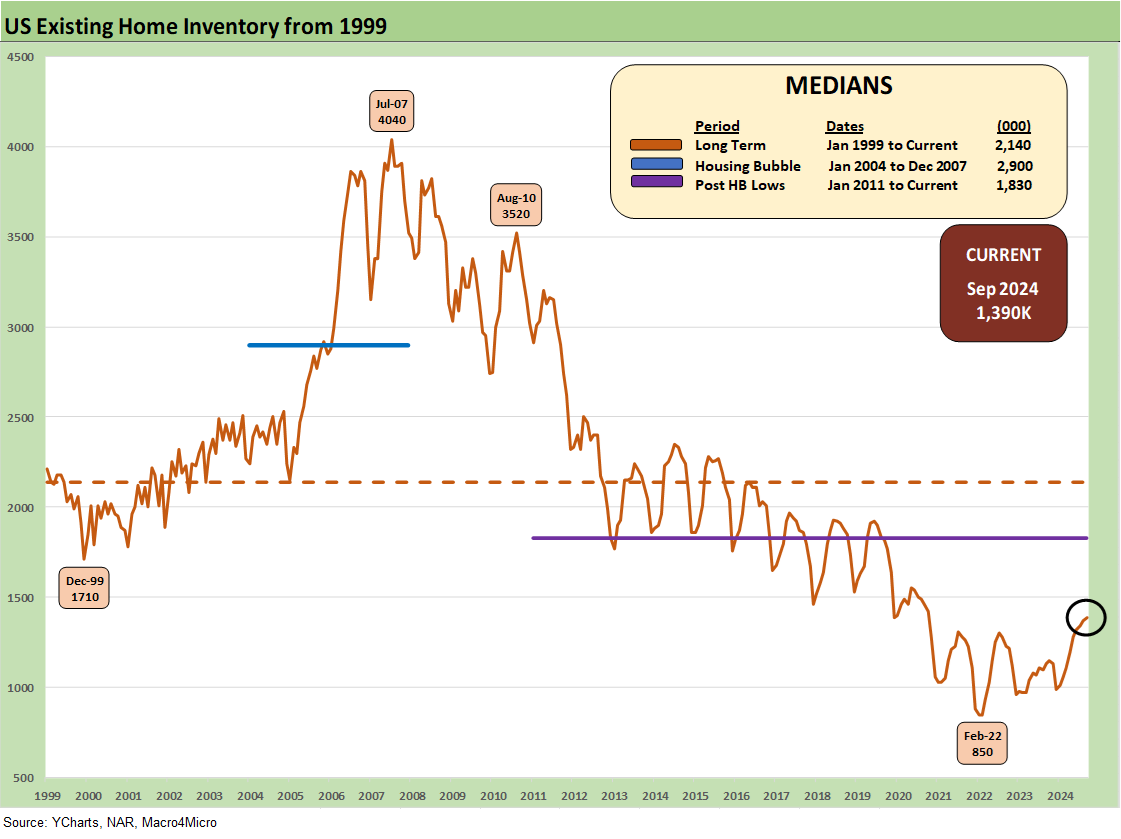

The above chart updates the run rate on inventories as those rise sequentially to 1.39 million units, up +1.5% MoM and +23.0% YoY. That clearly remains well below historical medians as noted in the chart. That helps keep Homebuilder ASPs strong with the relative lack of alternatives and existing home prices rising.

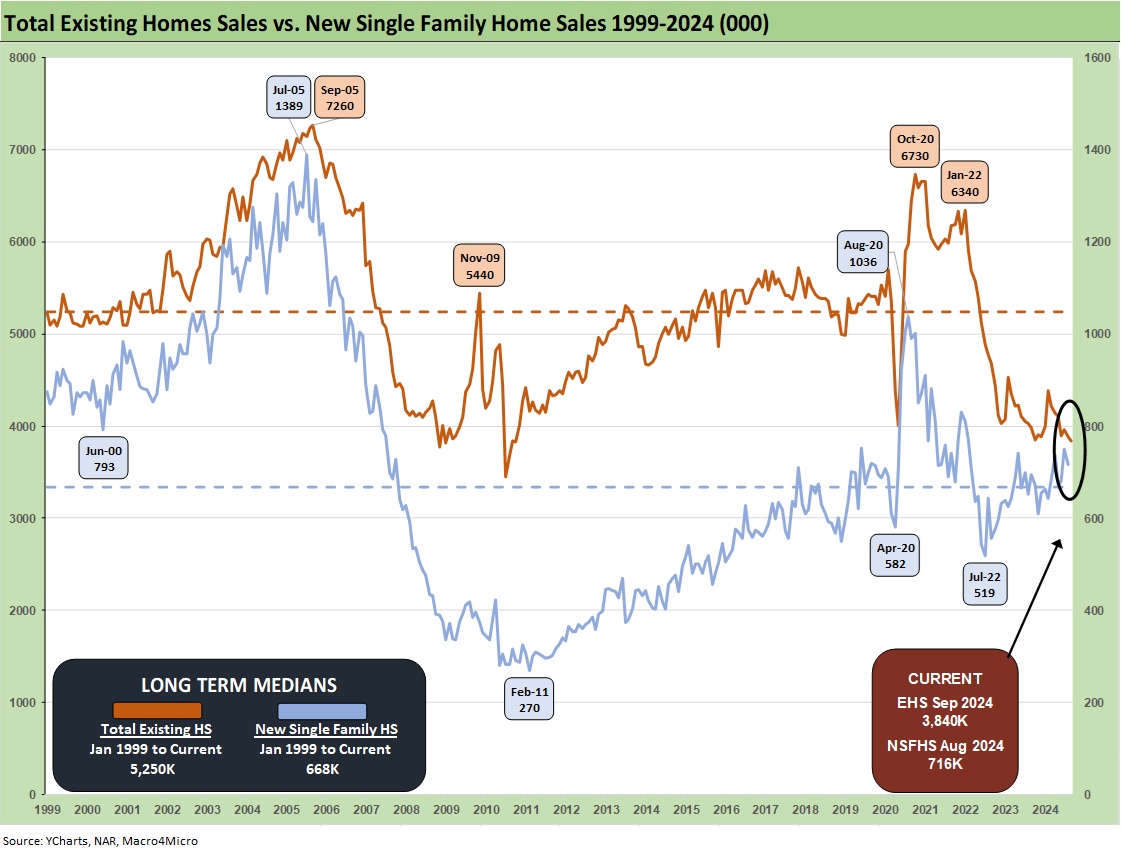

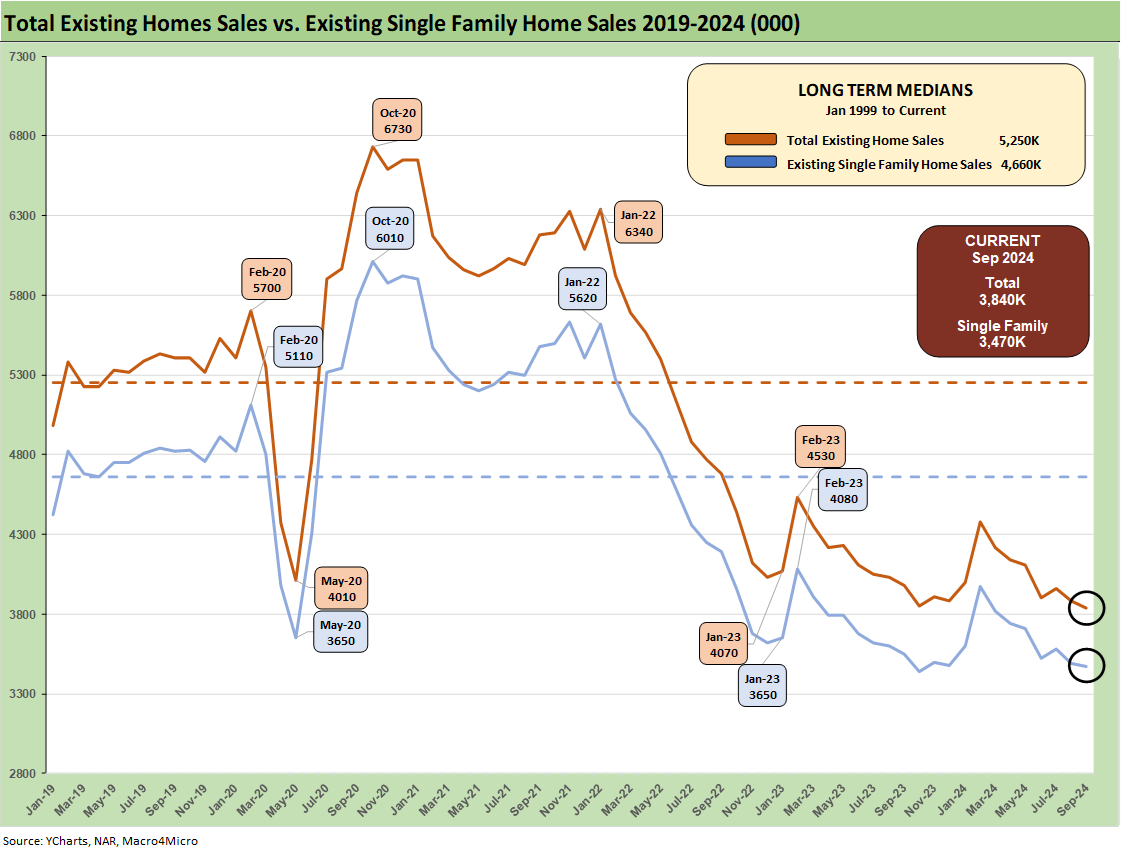

The above chart updates the time series for existing home sales and new home sales and the relative scale. We update the rising share being taken by new home sales with the “new home sales” September release this week. The simple point is that existing home sales dominate total home sales. That said, the continuing low in existing home sales vs. the long-term median is stunning in magnitude as noted in the median box vs. current levels (5.25 million vs. 3.84 million). Meanwhile, new home sales remain above the median.

The above chart breaks out the timeline for single family alone of 3.47 million vs. total existing home sales of 3.84 million, which is well below the long-term median (from Jan 1999) of 5.25 million for total existing homes. The lower line is ex-condo/ex-co-ops. We saw 370K in condos and co-ops in Sept 2024, down from 390K in Aug.

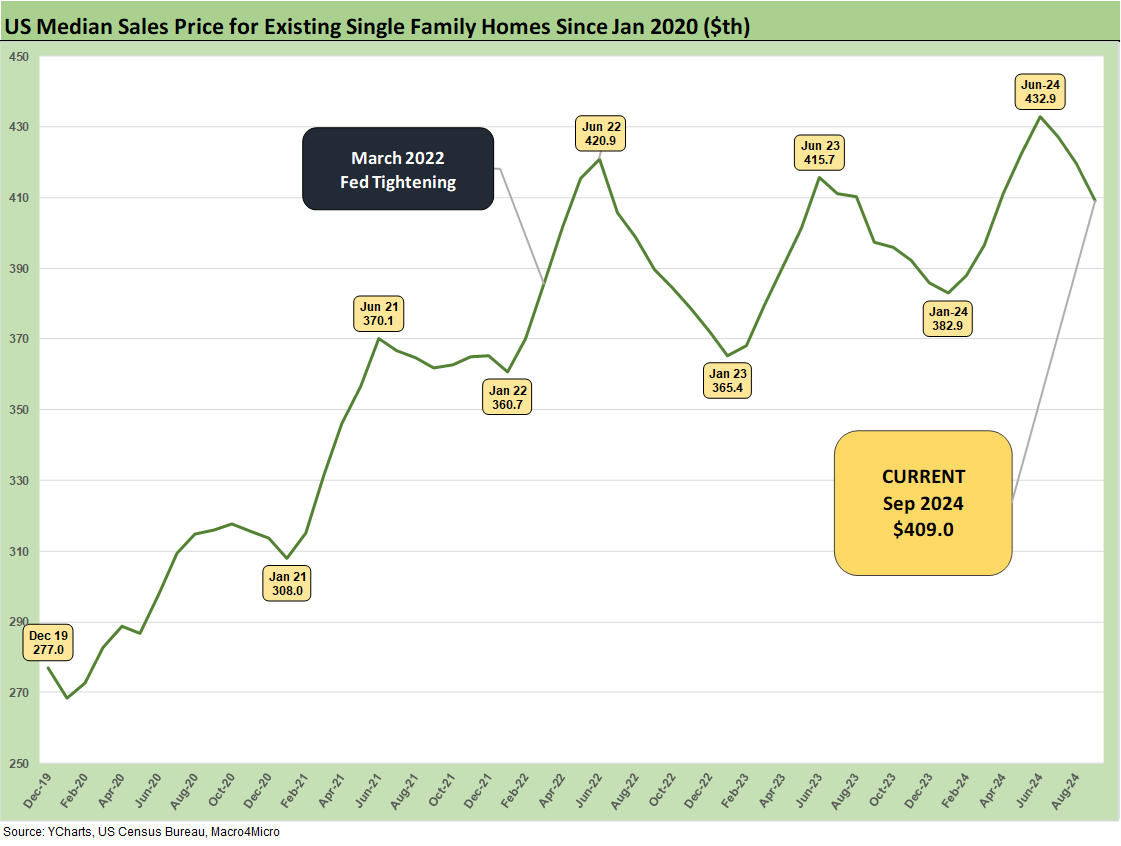

The above chart updates the median price for existing single family homes at $409K. Though down from the June 2024 high of $432.9K, the median price remains well above the $308K back in Jan 2021 when mortgage rates were near record lows. Higher mortgage rates and near record prices were the double whammy, but mortgage rates heavily drive the monthly payment burden.

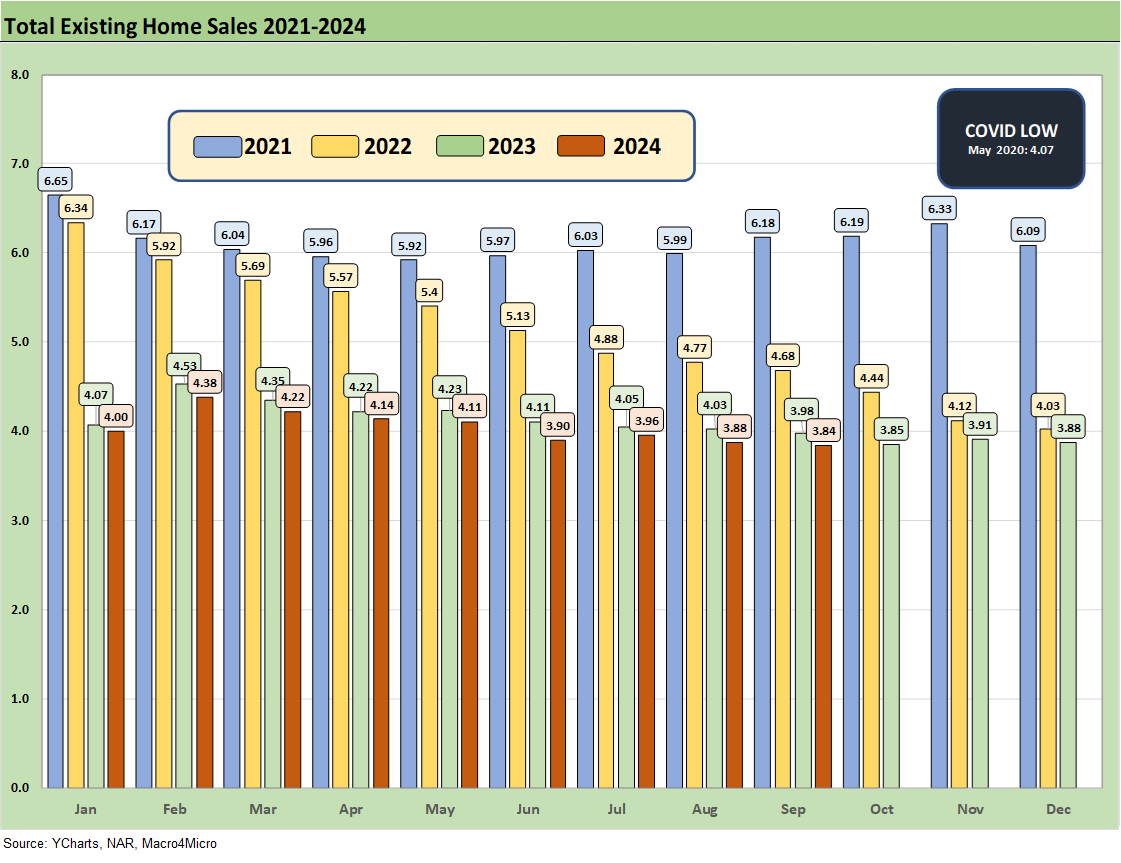

The above chart updates the monthly existing home sales across the timeline from Jan 2021 through September 2024. The market is a long way from the mid-6 and high 5 million handles of 2021 and then into early 2022 when many homeowners refinanced, and new buyers locked in low mortgages. ZIRP ended in March 2022 and then the UST migration began.

The September 2024 total of 3.84 million is below the May 2020 COVID trough of 4.07 although we had a few more sub-4 million handles along the way as noted in the chart.

The above chart details the sales deltas in the price tiers as lower price tiers are buffeted by affordability headwinds and “barriers to exit.” The recent move higher in mortgage rates will keep pressure on lower tiered pricing and potential buyers whose income levels are on the cusp in the context of monthly mortgage payments. After approaching low 6% handles, the 30Y mortgage rates are now closer to 7% once again. The sensitivity of monthly payments to changes in the UST curve and mortgage rates remain the critical swing factor.

See also:

State Unemployment Rates: Reality Update 10-22-24

Footnotes & Flashbacks: Credit Markets 10-21-24

Footnotes & Flashbacks: State of Yields 10-21-24

Footnotes & Flashbacks: Asset Returns 10-20-24

Mini Market Lookback: Banks Deliver, Equities Feel the Joy 10-19-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Retail Sales Sep 2024: Taking the Helm on PCE? 10-17-24

Industrial Production: Capacity Utilization Soft, Comparability Impaired 10-17-24

CPI Sept 2024: Warm Blooded, Not Hot 10-10-24

HY OAS Lows Memory Lane: 2024, 2007, and 1997 10-8-24

Payroll Sept 2024: Rushing the Gate 10-4-24

Credit Returns: Sept YTD and Rolling Months 10-1-24

Housing and Homebuilders:

PulteGroup 3Q24: Pushing through Rate Challenges 10-23-24

Housing Starts Sept 2024: Long Game Meets Long Rates 10-18-24

KB Home: Steady Growth, Slower Motion 9-26-24

New Home Sales Aug 2024: Waiting Game on Mortgages or Supply? 9-25-24

Lennar: Bulletproof Credit Despite Margin Squeeze 9-23-24

Existing Homes Sales Aug 2024: Mortgages Still Rule 9-19-24

Home Starts Aug 2024: Mortgage Rates to Kickstart Hopes Ahead? 9-18-24

Harris Housing Plan: The South’s Gonna Do It Again!? 8-28-24

New Home Sales July 2024: To Get by with a Little Help from My Feds? 8-24-24

Credit Crib Note: PulteGroup (PHM) 8-11-24

Credit Crib Note: D.R. Horton (DHI) 8-8-24

New Homes Sales June 2024: Half Time? Waiting for Mortgage Trends 7-24-24

Homebuilder Equities: “Morning After” on Rate Optimism 7-12-24

Homebuilders: Equity Performance and Size Rankings 7-11-24

Credit Crib Note: KB Home 7-9-24

Lennar: Key Metrics Still Tell a Positive Macro Story 6-20-24

Credit Crib Note: NVR, Inc. 5-28-24