Market Commentary: Asset Returns 12-7-25

The wild finish to 2025 is arriving with critical FOMC color and catch-up data on payrolls and inflation.

What affordability problem?

The major action this coming week will be wrapped around the FOMC and how they see inflation vs. payroll trading off against each other. A fresh game clock on easing decisions kicks into high gear in Jan 2026. The demand for mega-easing by the White House will keep tensions high.

Dead ahead is JOLTS for October, the Employment Cost Index for 3Q25, Nov jobs, Nov CPI, and some key earnings reports. We hear from tech bellwethers Broadcom and Oracle, retailer Costco (a recent addition to the tariff refund litigation list), and Toll Brothers in the high end of housing. Costco might raise the touchy subject of “affordability” as the White House tacitly admits (by way of action only) that the “seller does not pay” the tariff.

Equities have posted a very strong 6 months with some benchmarks such as the small cap Russell 2000 pushing beyond a weak 1H25 to hit a record high this past week.

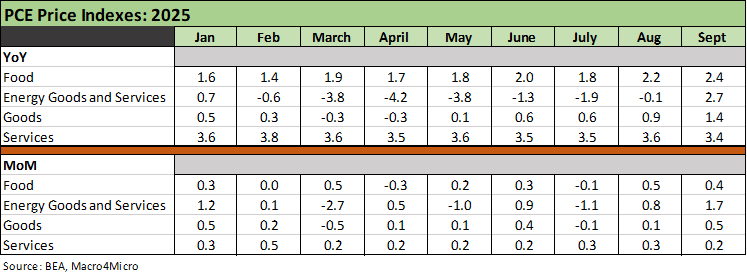

The PCE release from Friday (see PCE, Income & Outlays: Calendar Gap Closing 12-5-25 Credit Markets 12-1-25) did not help the easing case into 2026 is you look at some of the line items. We lift the numbers for the above table directly from the Friday release for Feb to Sept 2025. We took January numbers from the August release.

The reality is in the chart above, but the information below the headline level seldom gets called out. Rational people can just look at the numbers and state the obvious.

The simple drill is to look at the YoY PCE numbers for each month and ask a simple question:

Question: Are the September PCE price index YoY numbers for Food, Energy, and Goods higher or lower in September 2025 vs. the other months of 2025?

Answer: Higher with the high point of calendar 2025 reached in September.

Question: Is the Services PCE price index YoY higher or lower?

Answer: Lower, but still in the stubborn 3% handle range.

We will get CPI for November soon and the same drill applies. What is interesting to us is how little reference is made to the trend line across the major product lines in the financial media. Even CNBC ducks the topic given the rants that Trump sends out on such topics as he did this weekend when a guest on Fox and Friends dared to say “prices are going up” in 2025 (see Simplifying the Affordability Question 11-11-25).

Meanwhile, operations like CNBC need to protect their GOP guest tally and compete with Fox for dignitary time. So they just run with the high level PCE and CPI and skip the product lines that are unfavorable to the White House company line.

We look forward to a similar exercise when CPI comes out. Facts matter.

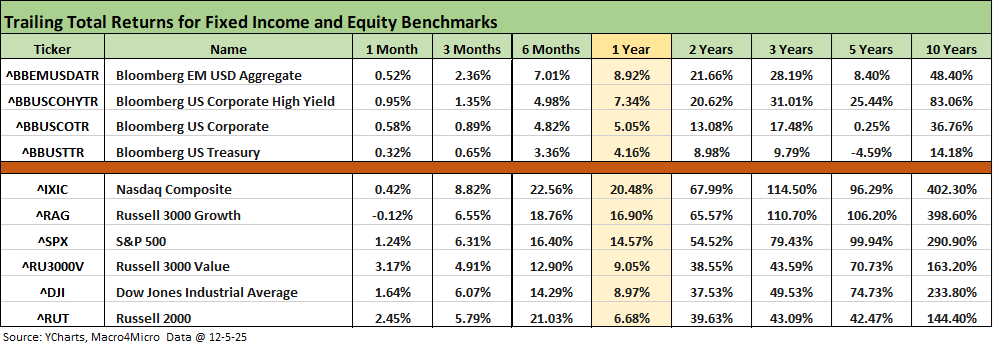

The above table updates the time horizon returns for the high-level debt and equity benchmarks we monitor. For the 1-month time horizon, we are back to all positive for the debt benchmarks. That positive return profile extends back to 5 years for the UST index as the tightening cycle kicked into gear in March 2022.

For equities, we still see the Russell 3000 growth slightly in the red. The 6-month return horizon is the key to the trailing 1-year numbers, which show 3 of the 6 firmly in double-digit return range. The NASDAQ return north of 20% is still well short of the 29% handle return in 2024. The S&P 500 and NASDAQ total returns for 2025 will need a very strong finish to match last year.

The rolling return visual

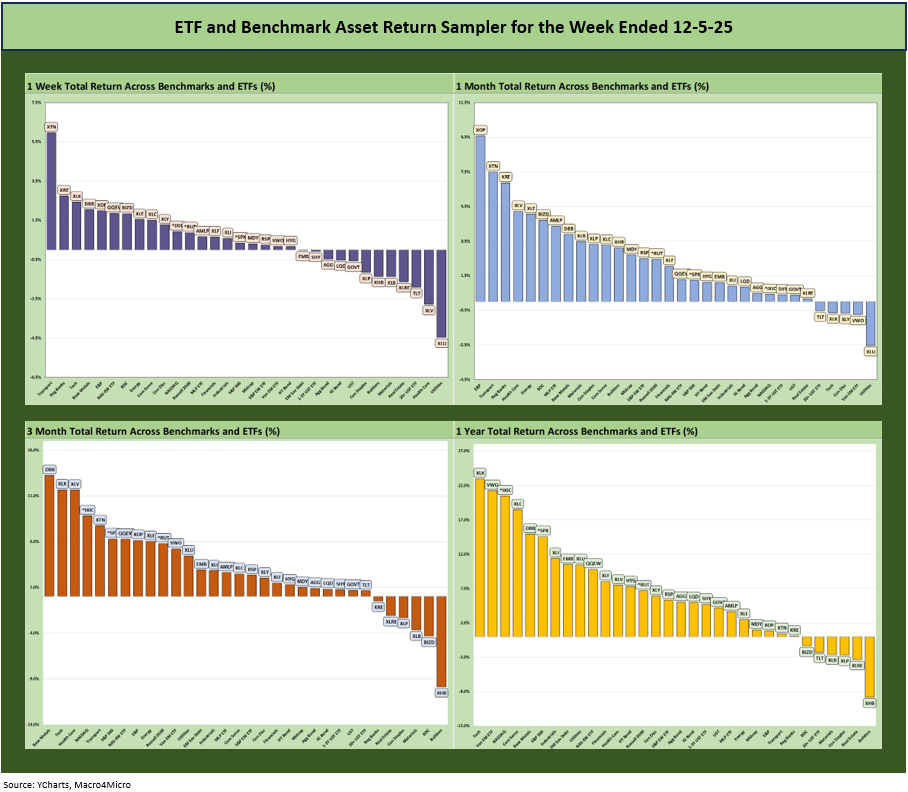

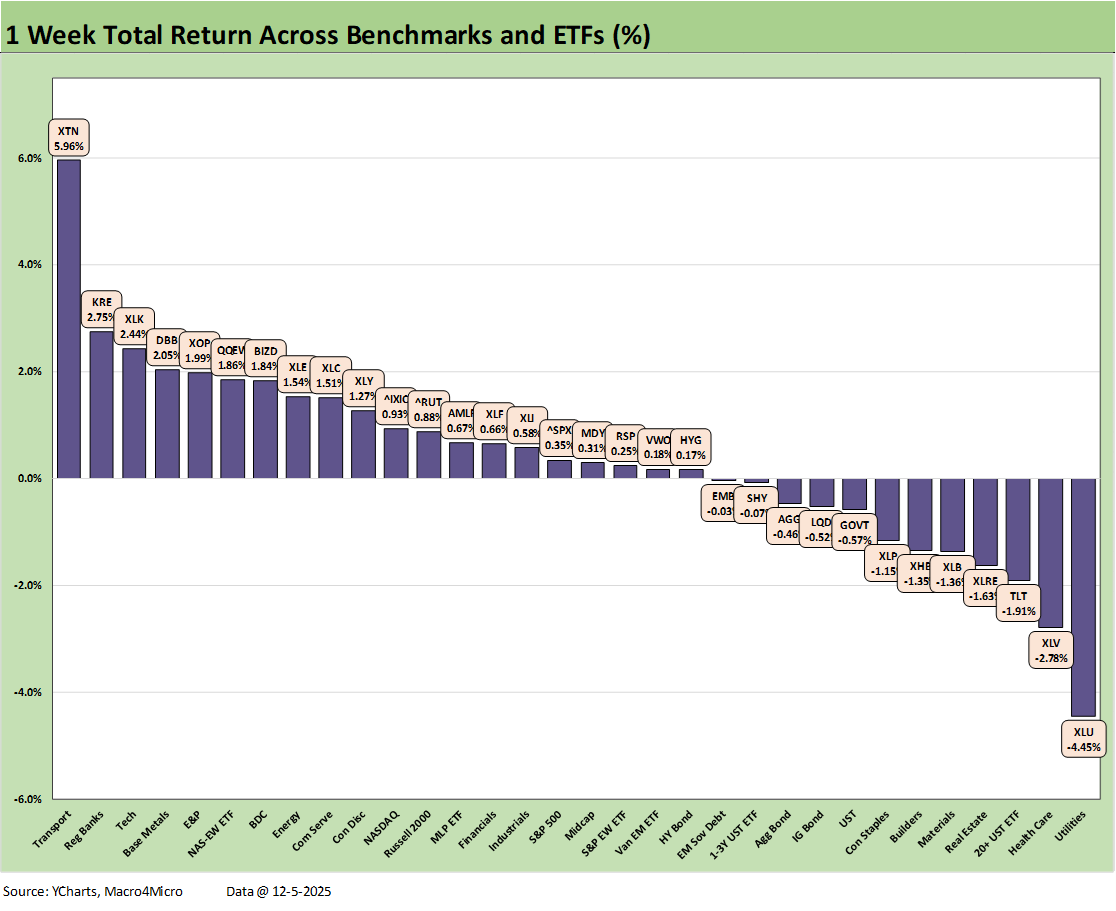

In the next section, we get into the details of the 32 ETFs and benchmarks for a mix of trailing periods. Below we offer a condensed 4-chart view for an easy visual on how the mix of positive vs. negative returns shape up. This is a useful exercise we do each week looking for signals across industry groups and asset classes.

The heavy weighting of positive return symmetry got back into action with a renewed stock rally this week partially offset by a mild setback in bonds. The YTD pattern (31-1) is not shown but sets the year up for a solid positive vs. negative score in 2025.

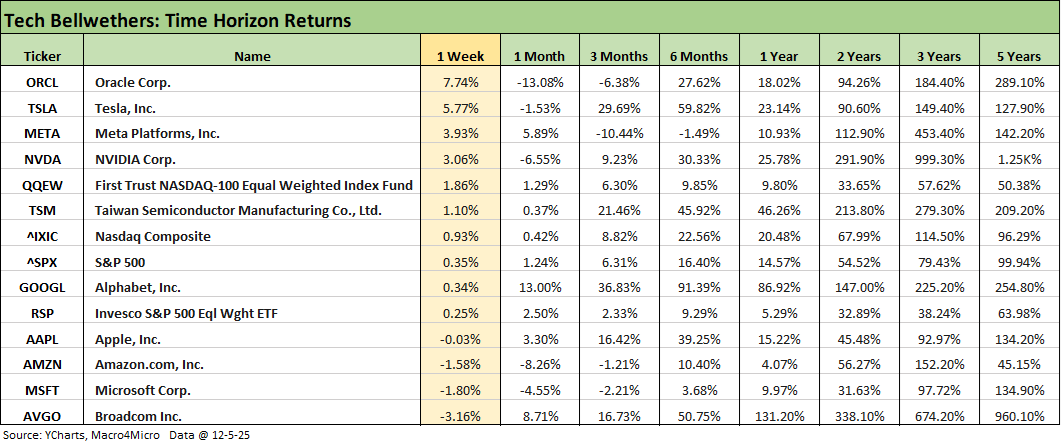

The Magnificent 7 heavy ETFs…

Some of the benchmarks and industry ETFs we include have issuer concentration elements that leave them wagged by a few names. When looking across some of the bellwether industry and subsector ETFs in the rankings, it is good to keep in mind which narrow ETFs (vs. broad market benchmarks) get wagged more by the “Magnificent 7” including Consumer Discretionary (XLY) with Amazon and Tesla, Tech (XLK) with Microsoft, Apple, and NVIDIA, and Communications Services (XLC) with Alphabet and Meta.

We already looked at the tech bellwether update for the past week in our Mini Market Lookback: Data Digestion (12-6-25). The FOMC color will weigh on how the UST curve might wag tech valuations, but we also get Oracle and Broadcom earnings this week for a fresh test of sentiment on the AI trade.

We already looked at the weekly return in our Mini Market Lookback: Data Digestion (12-6-25), but this week brings Oracle and Broadcom earnings for a fresh dose of speculation on where the AI boom is heading. The sensitivity of the mega tech names to interest rates is a matter of market realities. This week will bring some fresh discussions of those topics and also how the balance sheet X factors might be weighing on names such as Oracle with its heavy slate of recent debt issuance.

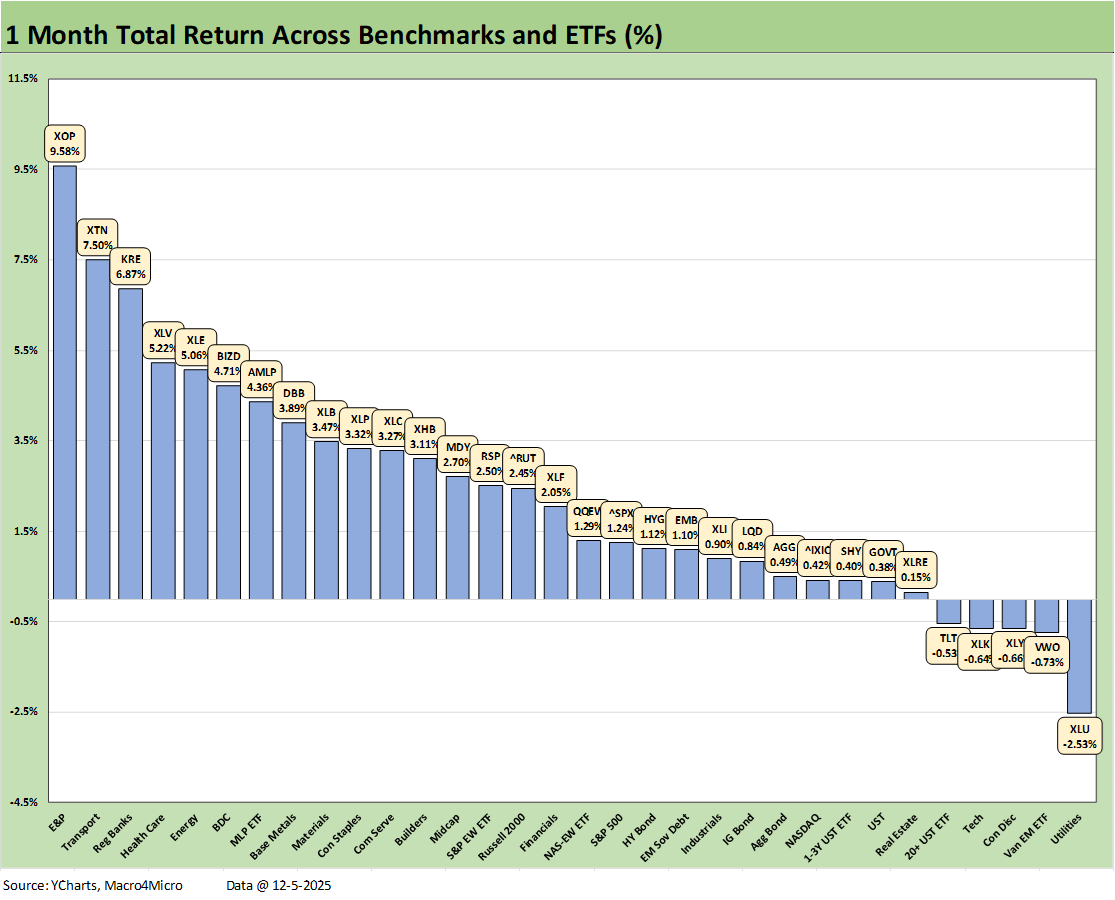

The 1-month time horizon weighed in with a score of 27-5 as equities saw a healthy performance from numerous non-tech sectors over the running 30 days. The top quartile saw a notable absence of tech-centric names and subsectors with the Tech ETF (XLK) in the red in the bottom quartile. NASDAQ was just across the line in the bottom of the third quartile joined by the Equal Weight NASDAQ 100 ETF (QQEW).

The top quartile also did not include the large cap benchmarks (S&P 500, NASDAQ) or the Russell 2000 small caps and Midcaps.

We see 6 of 7 bond ETFs in positive range, but the long duration UST ETF (TLT) is in the red in the bottom quartile. HYG carried the day within the group of bond ETFs, but HYG still was down in the 3rd quartile as bonds overall lagged.

Oil prices have struggled, but the energy ETFs have held in well. Whether it is a dim view of prospects for a Russia-Ukraine peace deal (i.e., Russian supply risk), the potential for protracted disruption of Venezuela heavy crudes, or simply cold weather bolstering natural gas, we see E&P (XOP) and the broad Energy ETF (XLE) performing well. We also see the Midstream ETF (AMLP) in the top tier.

Among notable comebacks has been the BDC ETF (BIZD) as the extreme extrapolation from a few headline private credit dogs is perhaps fading. Those deals could also be viewed through the lens of bad origination and not a wave of “cockroaches.” We cannot think of a major new wave of credit subsectors that have not had their share of underwriting and due diligence disasters across the decades.

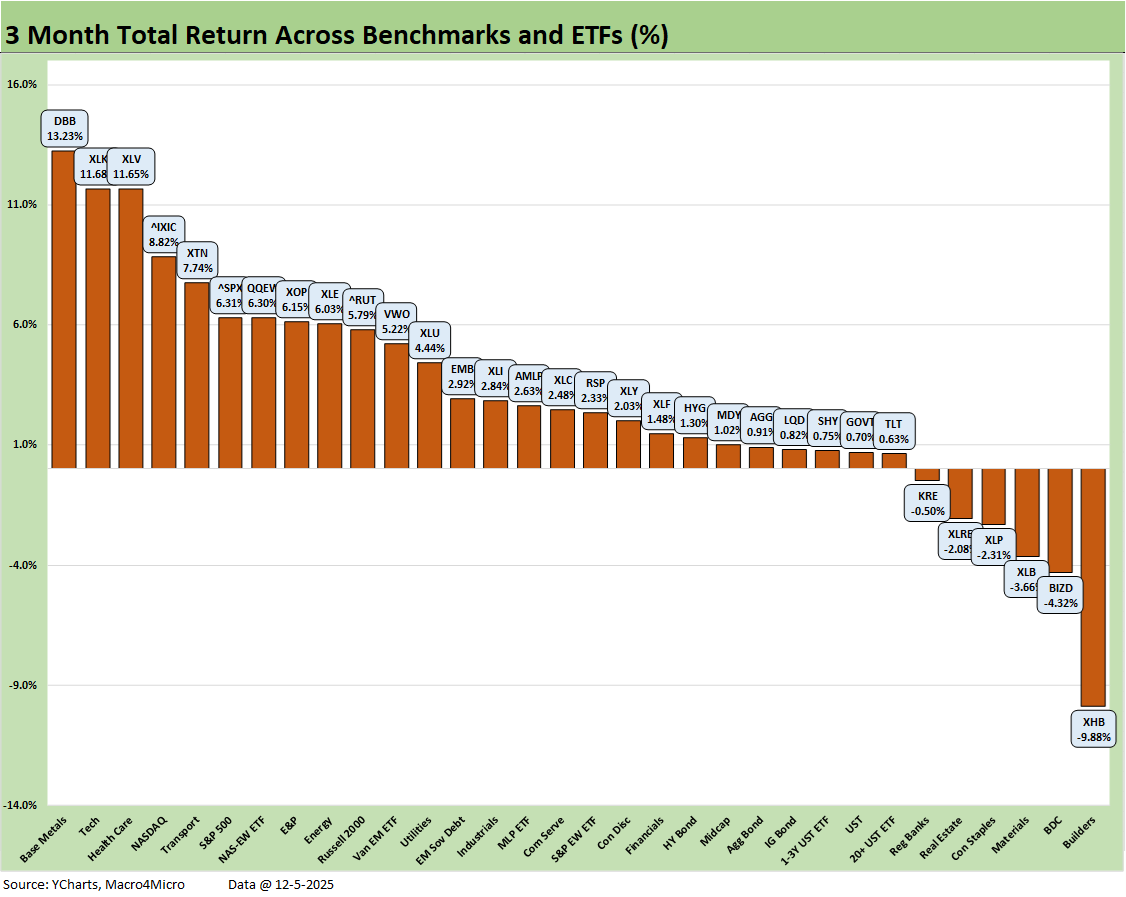

The rolling 3-month time horizon is still bringing a heavy tech-based contingent to the top quartile even though Base Metals (DBB) took the #1 spot. Tech (XLK) was slightly behind with Health Care (XLV) riding the pharma stock wave to the #3 spot. We see NASDAQ in the top 5 just ahead of the Transport ETF (XTN), who made the top tier on a recent airline rebound and the same for some bellwether freight and logistics equities. The heavy tech weighting of the S&P 500 kept the broad market benchmark in the top quartile with the Equal Weight NASDAQ 100 ETF (QQEW) in the mix.

Bond ETFs all made it into the positive return range with the asterisk that 5 of 7 bond ETFs returned less than 1% with 2 of the 7 in the bottom quartile (TLT, GOVT). Homebuilders (XHB) came in last place at -9.9% with BDCs (BIZD) second to last on the private credit headline wave. The other dwellers in the bottom tier included interest rate sensitive ETFs including Real Estate (XLRE) and Regional Banks (KRE). KRE also felt some of the private credit fallout.

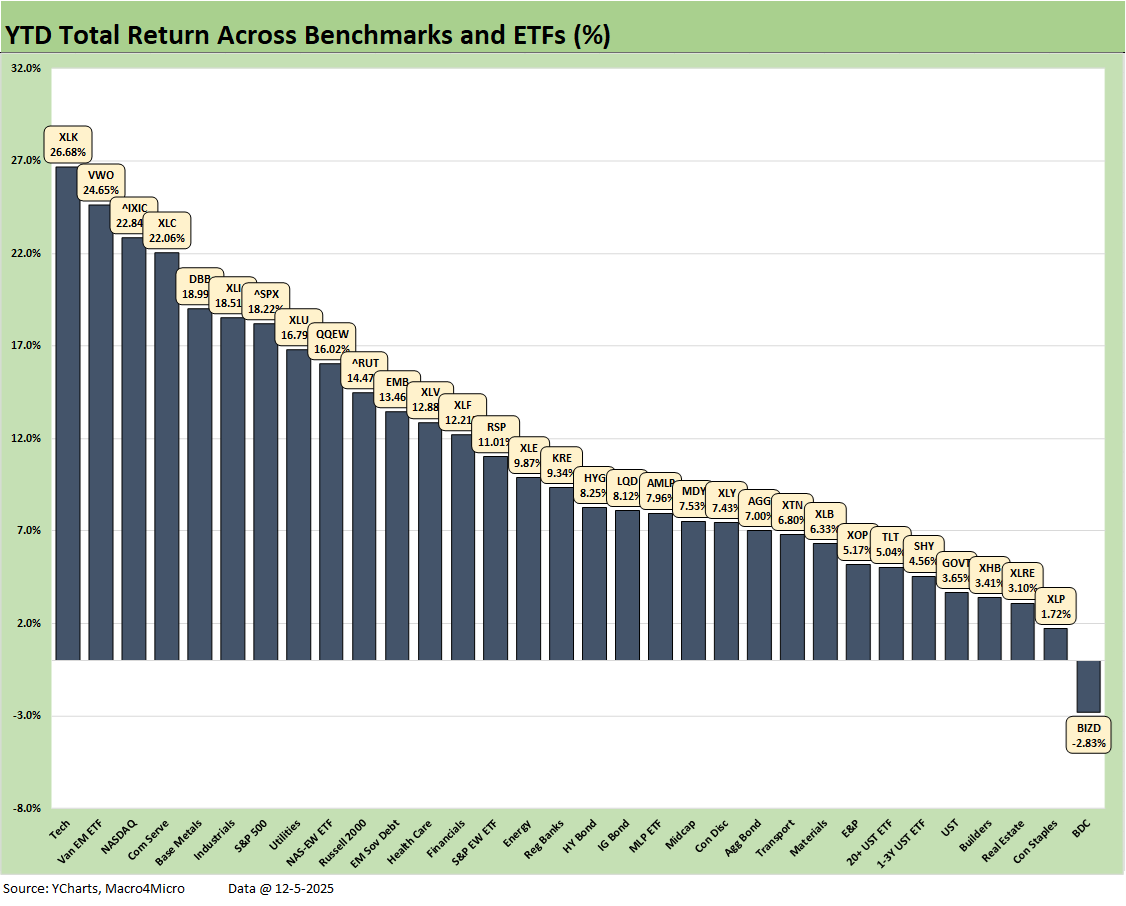

We looked at the YTD returns in our Mini Market Lookback: Data Digestion (12-6-25). The chart drives home that 2025 was a very good year to run the streak to 3 years of very solid asset returns following 2023 and 2024 (see Footnotes & Flashbacks: Asset Returns for 2024 1-2-25).

The score of 31-1 positive vs. negative returns include a single ETF in the red with BDC ETF (BIZD) at -2.8%. The hefty cash dividend returns on BDCs in those total return numbers ease the pain as we await more clarity on the direction of the credit cycle.

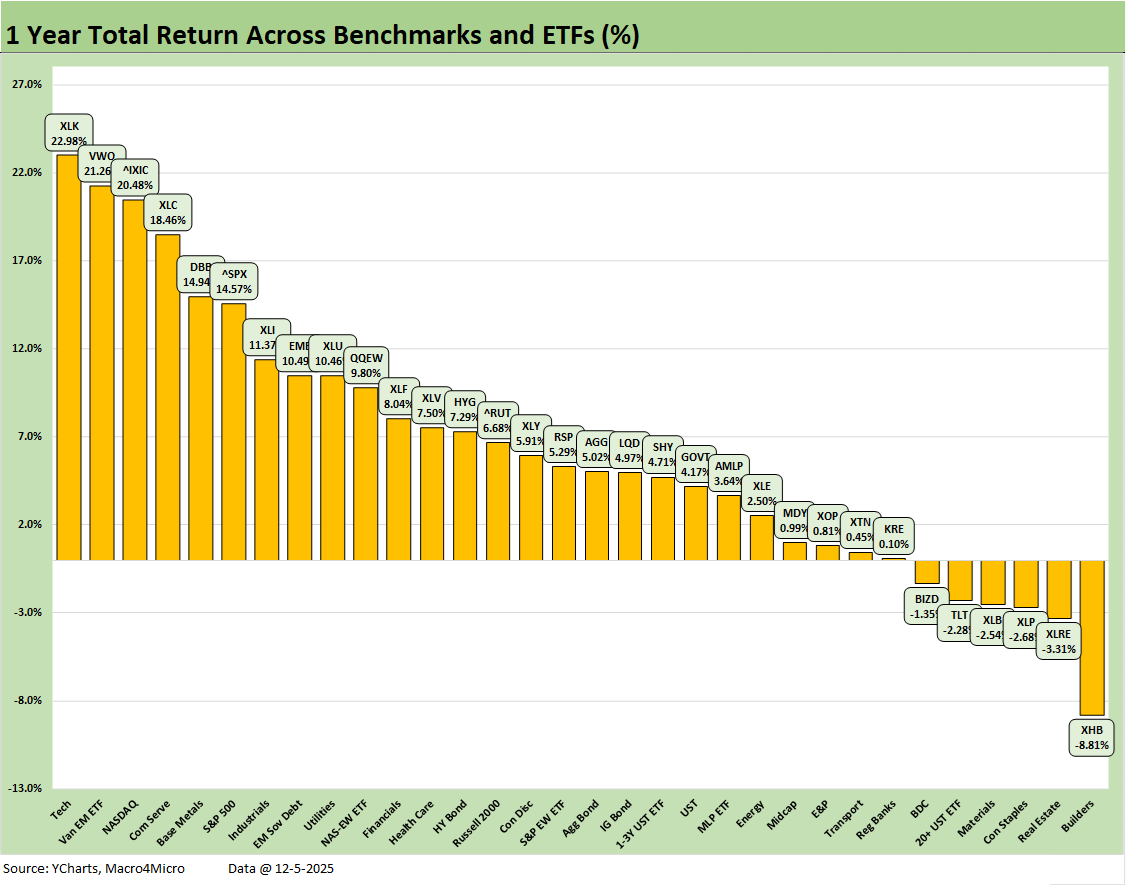

With around 3 weeks to go in the calendar year, the LTM score of 26-6 shows a heavy mix of interest rate sensitive ETFs in the red despite what has been a bull steepener in rates this year. Homebuilders (XHB) have been by far the worst performer at -8.8%. That comes after a period where XHB ranked #1 on an LTM basis at the end of 3Q24. It has been a long and troubled year for homebuilders and housing generally despite impressive home equity appreciation in recent years.

See also:

Mini Market Lookback: Data Digestion 12-6-25

PCE, Income & Outlays: Calendar Gap Closing 12-5-25

Credit Markets 12-1-25

Market Commentary: Asset Returns 11-30-25

Mini Market Lookback: Back into the June 2007 Zone 11-29-25

Durable Goods Sep 2025: Quiet Broadening of Core Capex 11-26-25

Retail Sales September 2025: Foot off the Gas 11-25-25

The Curve: Flying Blind? 11-24-25

Mini Market Lookback: FOMC Countdown 11-23-25

Employment Sept 2025: In Data We Trust 11-20-25

Payrolls Sep25: Into the Weeds 11-20-25

Mini Market Lookback: Tariff Policy Shift Tells an Obvious Story 11-15-25

Retail Gasoline Prices: Biblical Power to Control Global Commodities 11-13-25

Simplifying the Affordability Question 11-11-25

Mini Market Lookback: All that Glitters… 11-8-25

Mini Market Lookback: Not Quite Magnificent Week 11-1-25

Synchrony: Credit Card Bellwether 10-30-25

Existing Home Sales Sept 2025: Staying in a Tight Range 10-26-25

Mini Market Lookback: Absence of Bad News Reigns 10-25-25

CPI September 2025: Headline Up, Core Down 10-24-25

General Motors Update: Same Ride, Smooth Enough 10-23-25

Mini Market Lookback: Healthy Banks, Mixed Economy, Poor Governance 10-18-25

Mini Market Lookback: Event Risk Revisited 10-11-25

Credit Profile: General Motors and GM Financial 10-9-25

Mini Market Lookback: Chess? Checkers? Set the game table on fire? 10-4-25

JOLTS Aug 2025: Tough math when “total unemployed > job openings” 9-30-25Mini

Market Lookback: Market Compartmentalization, Political Chaos 9-27-25