Payrolls April 2025: Into the Weeds

We dig into the occupational lines in a resilient payroll gain not pointing to a downturn even if tariff dislocation concerns are justified.

Should be fine!

A gain of +177K in nonfarm payrolls is a resilient result amidst the policy chaos and sentiment shifts that leave a lot of questions on how hiring managers would react – and when. The result is better-than-expected in the context of a late cycle print with major questions looming around tariffs and future growth. Low multiplier effects services occupations padded the tally again this month.

Strength in the month was focused in the usual hot spots with Healthcare, Transportation & Warehousing, and Leisure leading the payroll number higher. The front loading of pre-tariff inventory building could have influenced short-term hiring. Construction turned in a positive month of +11K with quality payroll growth driven by specialty trade contractors in residential and nonresidential.

Manufacturing results were largely unchanged overall but mixed under the surface. Softness in motor vehicles and parts employment raises questions about the near-term effects of trade policy, particularly given simultaneous weakness in downstream auto retail.

The Fed has been provided a fresh look at a mix of March and April data in the past few weeks that offer evidence the economy is not heading into an immediate downturn unless “tariffs insist” as those are still under review in “the pause.” The urgent need for rate cuts is not apparent and the Fed’s data-driven approach is to remain patient.

The anxiety and uncertainty swirling around decision makers is taking hold though, and we see a more selective hiring environment in numerous industry groups with slower growth the likely path as trade tensions cause pockets of stress-testing as companies prepare for what lies ahead.

The above chart covers the composition of the monthly payroll changes by key industry groupings that we track from Table B-1 in the Payrolls report. The April numbers continue a second strong month of hiring after March even after a revision down to +185K. Revisions tend to get overlooked in favor of headline numbers and a two-month net revision of -58K trims some of optimism in interpreting the headline gain.

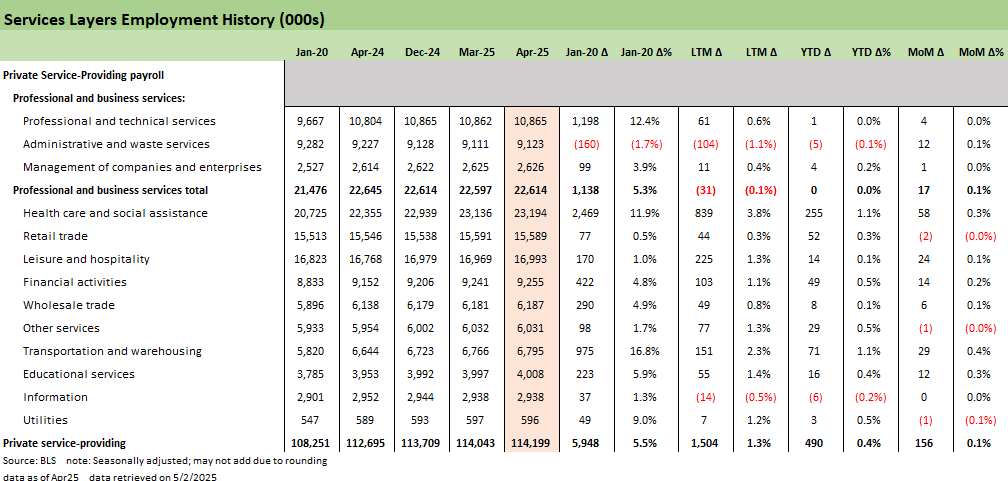

Top gainers in the above chart are usual core Services areas with not a whole lot of surprises. Healthcare (+58K) continues to have massive demographic led demand and Leisure & Hospitality (+24K) continues the slow recovery past COVID lows. Transportation and Warehousing results need some unpacking, driven this month by Couriers and messengers (+8.4K) and Warehousing and storage (+9.8K). The extra personnel in these areas may reflect inventory building and where the business reaction is pointing more positively in the data than the underlying rationale suggests.

In combing across the sectors more exposed to tariff effects, the combination of weakness in Motor vehicles manufacturing (-4.7K) and Motor vehicle and parts dealers (-4.6K) stands out. If a stated goal of tariff policy implementation is to bring more domestic auto manufacturing online, the disruption of established North American based supply chains and manufacturing through tariffs, some auto players are taking a step back.

One month of data leaves a lot of room for interpretation but the market reaction post-release has taken this as permission to rally for now. The morphing game plan on auto OEMs and suppliers indicates the message might be getting through to the Trump Tariff team that their initial plan was going to be a disastrous set or recommendation from “white boards run amok.” The outlook for increased auto transplant investment from Asia in particular is favorable. Those would have red states and right to work states as their likely destinations. In contrast, some legacy UAW OEMs could simply shrink. That will be an issue to watch.

The next series of charts including the one above show some key time horizons across the industry groups with more granular details. This first one is the broadest groupings that provide the Public and Private split and the Goods and Services split.

As evidenced above, the key driver of the strong growth for labor market for April is +156K in Services jobs and a minor contributions of +11K Goods-producing jobs and +10K Government. Trade policy to date has caused much uncertainty around what will happen in the summer and fall as transaction impacts (and uncertain retaliation decisions) play out.

In the payroll numbers above, there is little to point to for direct impacts even if there are plenty of anecdotes to weigh on timing and when employers would need to look to offset what they cannot pass along in price or lay off on other layers of the materials-to-supplier-to-OEM chain.

The question of how the above numbers can make the desired policy shift from predominantly services-focused to a mix tilted towards goods remains a mystery as the current state of affairs looks little changed from recent history. Trump may take the credit for continued labor demand now but the real damage will come as any tariff impacts start to reflect in some weakness in hiring or cost cutting actions.

The planning and execution of onshoring manufacturing takes time (years), but the plan also requires more clarity and stability in policy than has been provided to this point. Credibility has been a problem in the toggle from “committed to permanent” to constant bragging about “negotiations and deals” that lack transparency and occasionally get swept up in misinformation (“meeting with Xi” etc.) That is less than ideal for capital budgeting and project economics.

Consumers also need that clarity, and the headline panic has clearly led the sentiment surveys downward. The messaging has been poorly managed and that is one way to destabilize what has been a steady growth story.

The total Manufacturing growth came in at -1K, more or less flat on the month with little variance on the year. The LTM numbers above highlight the recent decline and where at least the motivation for tariffs is supported. We would not expect any major positive hiring actions just yet as a response to policy, but areas of weakness above in Motor Vehicles and Parts and Computer and Electronic products point to strain in the immediate reactions. How can one plan in electronics when the semiconductor policy is a moving target?

Motor vehicle jobs have been steadily declining this year, despite what should be accelerated production schedules for some inventory accumulation. OEM sales were exceptional in March. New orders in March for Autos were still ticking higher but these hiring numbers hint at expectations of softening demand. More visibility of where in the auto chain the jobs were lost will take some digging.

The Nondurable side of Manufacturing is laid out above, and the question remains on what would reasonably come back to the US with a higher tariff regime and which of these lines really need domestic capabilities. The “labor arb” is not going away. The above longer term trends support the idea that most of these are not essential though the tariff actions are indiscriminately broad for now even if some progress has been made to narrow it down.

Construction is a bright spot in the report with another +11K jobs after a strong March. However, the contractor heavy mix suggests activity in completing ongoing projects rather than new ones as we just saw negative construction spending numbers in from the March release. Changing project economics on incremental (or large) increases to material costs will be hurdles for more labor demand. We covered where equipment rental operators are not seeing pullback for most spending plans but increasing costs and lower spending do not bode well here.

Services is as always the largest group in the payroll mix and deltas. The strong headline prints go hand in hand with strong Services prints. Retail trade was flat on a net basis, but sector detail shows weakness in tariff-exposed categories such as motor vehicles, furniture, clothing, and sporting goods & hobbies, offset by gains in food and beverage stores. Reading too much into the one-month trend always comes with an asterisk, but Retail is one area where such tariff-exposed retailers are pulling back when tariffs are so high relative to the very low margins. The China inventory threat also looms large in coming weeks.

Tariff-induced inflation expectations have already made their way into consumer sentiment and the above sectors will see disproportionate impact amidst spending cuts. Retailers have been outspoken already on their ability to stock goods and how a lack of tariff relief will decimate margins given very little appetite for higher prices for consumers. Trade credit could also become an issue with bankruptcy risks very real threat as the trade war unfolds.

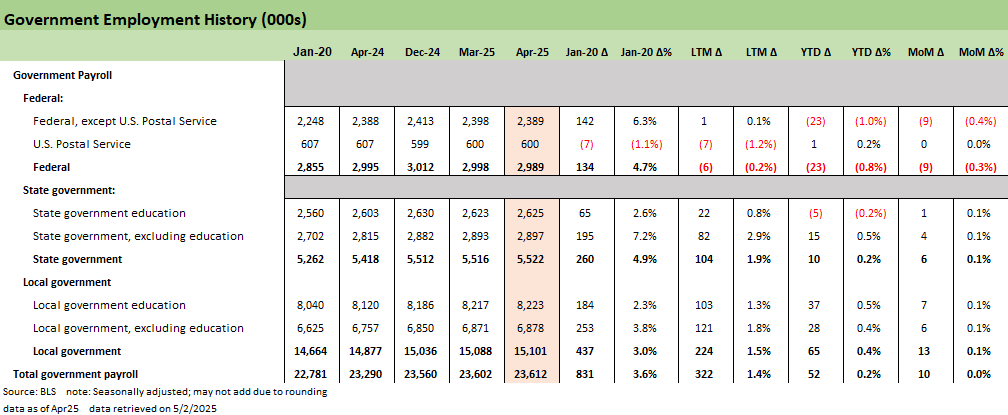

The last chart in the collection looks at the Government employment lines that had an outsized presence in headlines given Federal cuts by DOGE. The majority of that work seems to be behind us now with -23K the total damage done on jobs even if the impact has more room to run in some departments. State and Local hiring remained strong with 6K and 10K, respectively.

See also:

Payroll April 2025: Moods and Time Horizons 5-2-25

Construction: Singing the Blues or Tuning Up for Reshoring? 5-1-25

Employment Cost Index 1Q25: Labor is Not the Main Worry 5-1-25

1Q25 GDP: Into the Investment Weeds 4-30-25

PCE March 2025: Personal Income and Outlays 4-30-25

1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25

JOLTS Mar 2025: No News is Good News 4-29-25

Tariffs: Amazon and Canada Add to the Drama 4-29-25

Credit Snapshot: D.R. Horton (DHI) 4-28-25

Footnotes & Flashbacks: Credit Markets 4-28-25

Footnotes & Flashbacks: State of Yields 4-27-25

Footnotes & Flashbacks: Asset Returns 4-27-25

Mini Market Lookback: Earnings Season Painkiller 4-26-25

Existing Home Sales March 2025: Inventory and Prices Higher, Sales Lower 4-24-25

Durable Goods March 2025: Boeing Masking Some Mixed Results 4-24-25

Equipment Rentals: Pocket of Optimism? 4-24-25

Credit Snapshot: Herc Holdings (HRI) 4-23-25

New Home Sales March 2025: A Good News Sighting? 4-23-25

Mini Market Lookback: The Powell Factor 4-19-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Home Starts Mar 2025: Weak Single Family Numbers 4-17-25

Credit Snapshot: Service Corp International (SCI) 4-16-25

Retail Sales Mar25: Last Hurrah? 4-16-25

Industrial Production Mar 2025: Capacity Utilization, Pregame 4-16-25

Credit Snapshot: Iron Mountain (IRM) 4-14-25

Mini Market Lookback: Trade’s Big Bang 4-12-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

CPI March 2025: Fodder for Spin 4-10-25

Credit Snapshot: Avis Budget Group (CAR) 4-9-25

Credit Snapshot: AutoNation (AN) 4-4-25

Credit Snapshot: United Rentals (URI) 4-1-25