Credit Snapshot: United Rentals (URI)

We summarize the credit fundamentals of United Rentals.

Credit Trend: Stable

Summary credit profile: URI is an important issuer that ranks in the Top 10 BB tier names and Top 20 for HY. The composite ratings fall prey to structural subordination conventions with a mid BB composite rating for unsecured, high BB for the single 2L bond, and low BBB for the 1L bond. We consider URI investment grade caliber with material excess asset protection and low business risk.

The history of URI is a mix of debt-financed M&A and heavy reinvestment in organic growth that has driven rapid growth in revenue, profits, and cash flow along with exceptionally high EBITDA margins. The recent attempt to buy H&E (HEES) continued that history, but URI was outbid by Herc Rentals (HRI), who needed to step up and close the gap between HRI and the two equipment leasing leaders, URI at a strong #1 and Ashtead at #2 (see Herc Rentals: Swinging a Big Bat 2-18-25).

Relative Value: URI is a more defensive core holding for medium grade credit risk exposure. Investors crossing the line into BB tier unsecured find better value and a wider range of maturities and coupon selection. URI has a heavy slate of bonds from 2027 to 2034 with coupons running from 3% to 6% handles. Intermediate URI bonds trade in the range between the BBB and BB tier spread composites, but healthy risk symmetry is useful in a market like this. URI bonds boast good secondary liquidity. Bonds in 2032-2034 maturities recently traded in the +185 bps midrange area (per 7 Chord).

Business Risk: The other side of the URI’s M&A story has been characterized by the rapid recovery of balance sheet metrics and consistently successful integration of M&A. That has led to a well-earned perception of low deal execution risk in URI’s role as an aggressive industry consolidator. The diversity of industrial verticals beyond the construction markets and an extensive customer counterparty base and equipment types mitigate risk.

Tariffs: The proposed tariffs will raise the cost of equipment and offer an advantage to companies who can provide equipment financing flexibility in funding equipment needs in the “lease vs. buy” decision. URI’s performance across the credit crisis and post-COVID supplier chain disruptions reinforce the ability of URI to operate in challenging markets with multiple equipment suppliers located onshore and offshore that mitigate the tariff risks as well. The secular trends in equipment leasing remain favorable, and the US-centric nature of the business and branch system insulates URI from many tariff risks even though they will also face some equipment inflation and side effects of the tariffs on customer activity. Tariffs will also strengthen the used equipment market that URI taps to manage fleets and net capex.

URI operations in Canada have a fleet mix tailored to Canadian needs. Energy infrastructure investment is likely to rise in Canada to reduce US exposure. In addition, if Trump’s goal of major reshoring/onshoring activity comes true, URI wins. The Trump focus on energy infrastructure also favors URI but some other major project groups will taper off and get undermined (EV capex).

Profitability: High EBITDA margins and high net margins across a wide range of cyclical histories since the 1997 IPO clearly highlight the success of URI’s growth strategy and prudent fleet management practices. URI’s ability to execute as a sector leader has been confirmed while URI broadened its end market exposure and the range of the customer base with its North American-centric operations (see United Rentals 4Q24: Strong Numbers Set the Table 2-2-25). That mitigates earnings volatility risk in the stressful trade backdrop.

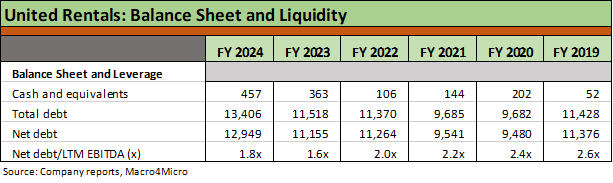

Balance Sheet: Leverage has a target range of 1.5x to 2.5x with FYE 2024 at 1.8x, which is the second lowest 12-31 leverage metric for the last dozen years. The attempted H&E deal ($4.8 bn including debt) called for URI getting to 2.0x within 12 months (see United Rentals: Bigger Meal, Same Recipe 1-14-25, Credit Crib Note: United Rentals 11-14-24) but that challenge now moves over to Herc Rentals, the # 3 leasing operator. Major deals are easily financed by URI with ABL and unsecured debt.

URI has demonstrated its ability to navigate a wide range of macro scenarios while sustaining very strong free cash flow and a solid balance sheet. That timeline included a period of the post-COVID supplier chain disruptions, which has some common features with potential trade wars. Free cash flow resilience and capex flexibility mitigates downside risk in a way that investors cannot find in high fixed cost manufacturing industries or issuers with high commodity price exposure.

Cash flows and capital allocation: Excess free cash flow allows for sustainable, major stock buybacks and in more recent years paying a dividend. URI uses brief pauses in buybacks after major M&A to quickly restore its balance sheet leverage. Capex flexibility and short lead times on equipment orders support the credit quality story as does the intrinsically flexible fleet management strategies with a deep secondary used equipment market.

SELECT CHARTS

Aggressive growth and high margins tell the story.

Disciplined leverage targets and strong balance sheet in historical context.

M&A, shareholder enhancement (buybacks, dividends) part of a balanced attack.

Net capex translates into flexible fleet management and resilient cash flow.