GDP 3Q24: Final Number at +3.1%

We update the line item deltas for the revisions of GDP estimates as Biden’s last in-office GDP headline is a +3.1% GDP quarter.

Are the 3% annual GDP growth days over?

Biden is going out in style ahead of his exit stage left (literally and politically) with a +3.1% quarter coming on the heels of 3.0% for 2Q24.

The problem with facts for many politicians and policy makers is that they can be your friend or your enemy, but there is often an embrace of the idea that facts only matter when they help you.

The latest 3Q24 final number brings back-to-back 3% handle GDP quarters as a solid economy is in place with Biden handing the baton to Trump 2.0.

For some of the add-on items in the 3Q24 final GDP release, we see +1.5% for the 3Q24 PCE price index and +2.2% for Core PCE in 3Q24, the savings rate was +4.3% for 3Q24, and Real Disposable Income was +1.1% on the latest revision. The current dollar GDP was +5.0%.

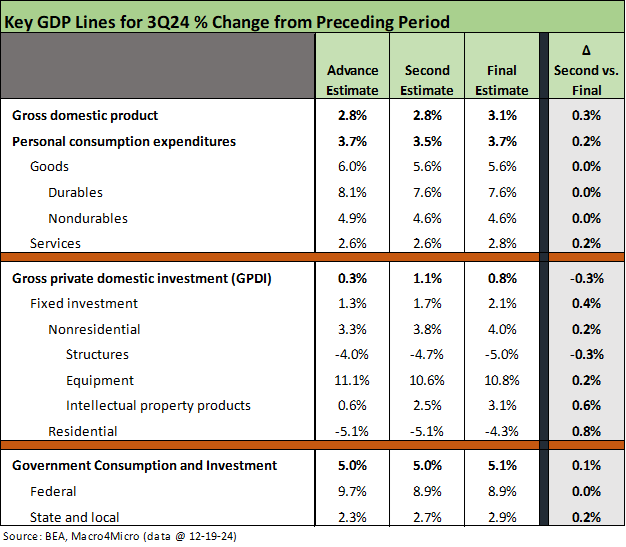

The latest print of GDP and the deltas across PCE, Goods, Services, and the important fixed investment lines are broken out above. We already looked at the first two cuts of the numbers in earlier posts (see 3Q24 GDP Second Estimate: PCE Trim, GPDI Bump 11-27-24, Presidential GDP Dance Off: Clinton vs. Trump 7-27-24).

The PCE line was revised higher by +0.3% from the second estimate, and PCE is always the key driver at over 2/3 of nominal GDP. The GPDI line and Government groupings are the other two big GDP components with GPDI revised modestly lower and Government higher. The economy still turns on the consumer and is even more evident now as Fixed Investment starts to see slower growth or outright declines.

While reshoring offers great theme music and it is conceptually sound on the “white board,” the short memories seem to forget that weak corporate investment and weak exports in 2019 led the FOMC to ease. A lot of pro-tariff economists (or tariff rationalizers) who pitch the lack of inflation in the last round of tariffs don’t seem to recall the capex weakness and export challenges. After all, it clashes with the tune being played.

The highlights from the above are clear enough:

The consumer is very strong: The PCE line was what slapped down the recession stories in the fall of 2022 as high payrolls and high PCE prevailed. The consumer drives the bus on GDP and is not swerving – yet. Asset quality erosion is in evidence, but a new crop of borrower/buyers enter the labor force regularly with a fresh game clock as long as jobs are there. Demographics are the friend of the PCE line. We see PCE tick back up to the advance estimate level at +3.7% with Goods and related categories flat while the much larger Services line moved higher.

GPDI ticked lower but Fixed Investment was higher on Nonresidential revision: Fixed investment is a major group of line items, and the bigger lines of Equipment and IP Products moved higher while Structures moved lower. Structures had been getting a lift this cycle from construction projects (see links at bottom) but has since peaked after a massive ramp-up (see Fixed Investment in 3Q24: Into the Weeds 11-7-24, Construction: Project Economics Drive Nonresidential 10-2-23).

Residential was “revised higher” to a smaller decline: Past housing cycles have shown material contraction on the Residential Fixed investment line when housing cycles turn down. Beyond the mortgage issues we looked at last night with the UST beatdown following the FOMC actions and color commentary (see Fed Day: Now That’s a Knife 12-18-24), there will be some other issues underway that we will address in our housing sector and single name builder work. Mass deportation will undermine the residential housing labor force and tighten subcontractor capacity. We will also see more supplier chain disruptions from tariffs for the many goods and components that flow into building homes and communities. That is a topic for another day, but the net factors there are all headwinds.

Government has peaked: With DOGE ball about to take on the role of Job Killer and Spending Rollerball, these lines will be in for a big shakeup at the Federal level, but State and Local consumption and expenditures ($2.45 trillion) is still much larger than Federal (with $1.5 trillion and more than half of that in defense). The big changes in Federal consumption will be interesting to watch from here. The DOGE plan impacts payroll, the tax base, services multiplier effects, etc. all the way down to the State and Local level. The rule of “there is no frictionless wheel” continues as a reality. Some choose to pretend side effects are nonexistent.

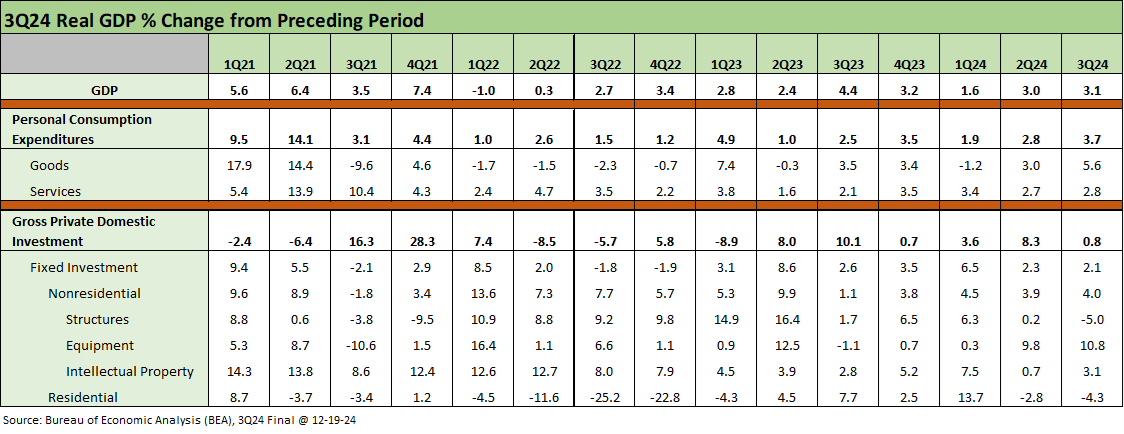

The above chart drops in the latest set of numbers back to the 1Q21 period when Biden took the helm. In 1Q21, COVID was still in play but with the vaccine rolling out. ZIRP was in place through 1Q22, and demand boomed for multiple reasons and notably after multiple stimulus programs from the Dec 2020 stimulus inked by Trump to the bigger programs launched by Biden.

As we look back to the 2021 and 2022 period as inflation spiked to a June 2022 peak and tightening was underway, we always wonder if there could be a show of hands of who would volunteer back then to forego any stimulus that directly impacted their jobs, their corporate top lines, or their net worth if they knew inflation would be the outcome. We suspect they would volunteer to let “the other guy” take the hit and not their own interests.

Facts, reality, and truth will face a tough 2025…

When one is looking for a light Christmas moment, Ayn Rand quotes are never a good idea, but so much for good ideas. As a card-carrying Democrat, I am not a big Rand fan per se. But it is always important to put right wing purity to a cleanliness test.

Rand was the icon of the right in the 1980s and one of Greenspan’s crushes. We wonder what she would think about the political and economic discourse and use of facts today. Here are a few Rand quotes on the topic of absolutes, reality, and truth:

“The hardest thing to explain is the glaringly evident which everybody has decided not to see.”

“The truth is not for all men, but only for those who seek it.”

“There are no white lies, there is only the blackest of destruction, and a white lie is the blackest of all.”

Facts do matter, and GDP growth statistics and the line items that roll up into GDP matter since those underlying lines frame supply and demand, inflation, wages, employment, and the usual array of issues that matter to households. The trick for many on the “vote for me” circuit is to market the economic variables that help one’s case. Usually that entails ignoring the rest.

It is fair game to spin facts in the world of lawyers and to be “selective,” but basic economic facts need to be considered when framing economic reality. The facts are that post-2000 economic trends in the US have been low growth but with phenomenal innovation and wealth creation. That does not change the facts of the good and bad on the checklist.

Along that vein of selective facts, Biden could not hide from the inflation in his term just as Trump cannot hide from the mediocre GDP growth of his first term. Biden took the hit on inflation just like Ford and Carter did and they all lost their post-inflation elections.

For Trump, simply calling it “the greatest economy in the history of the world” works with many, but it is laughably false. Reagan and Clinton would certainly disagree (see Presidential GDP Dance Off: Reagan vs. Trump 7-27-24, Presidential GDP Dance Off: Clinton vs. Trump 7-27-24). The Mike Johnsons pile on with the same message and they get a “rules of the game” waiver and not dishonest behavior demerits. Lying is OK in Washington and is now on a loyalty pass-fail checklist. You are required to repeat the lies from the top.

The practical reality is that Biden was awful at masking or explaining away important negative facts while the latter (Trump) is a Gold Medal Decathlete in “fact denial” and more dangerously setting loyalty oaths tied to an embrace that facts do not exist at all (election outcomes, GDP stats, etc.).

The ability to alter or erase facts is what gets covered in history books after the fact. You won’t find the unvarnished versions on MSNBC, and you likely won’t see many facts at all on Fox. Even CNBC is backsliding some days to make sure their guests come back. Nature of the beast.

See also:

Fed Day: Now That’s a Knife 12-18-24

Housing Starts Nov 2024: YoY Fade in Single Family, Solid Sequentially 12-18-24

Industrial Production: Nov 2024 Capacity Utilization 12-17-24

Retail Sales Nov24: Gift of No Surprises 12-17-24

Inflation: The Grocery Price Thing vs. Energy 12-16-24

CPI Nov 2024: Steady, Not Helpful 12-11-24

Payroll Nov 2024: So Much for the Depression 12-6-24

Trade: Oct 2024 Flows, Tariff Countdown 12-5-24

3Q24 GDP Second Estimate: PCE Trim, GPDI Bump 11-27-24

Fixed Investment in 3Q24: Into the Weeds 11-7-24

The Politics of Objective GDP Numbers: “Flex Facts” on Growth 10-30-24

3Q24 GDP Update: Bell Lap Is Here 10-30-24

2Q24 GDP: Final Estimate and Revision Deltas 9-26-24

2Q24 GDP 2nd Estimate: The Power of 3 and Cutting 8-29-24

Presidential GDP Dance Off: Clinton vs. Trump 7-27-24

Presidential GDP Dance Off: Reagan vs. Trump 7-27-24

GDP 2Q24: Banking a Strong Quarter for Election Season 7-25-24

State Unemployment: A Sum-of-the-Parts BS Detector 6-30-24

1Q24 GDP: Final Cut Moving Parts 6-27-24

Construction Spending: Stalling Sequentially at High Run Rates 6-4-24

1Q24 GDP: Second Estimate, Moving Parts 5-30-24

1Q24 GDP: Looking into the Investment Layers 4-25-24

1Q24: Too Much Drama 4-25-24

4Q23 GDP: Final Cut, Moving Parts 3-28-24

4Q23 GDP: Second Estimate, Moving Parts 2-28-24

GDP and Fixed Investment: Into the Weeds 1-25-24

4Q23 GDP: Strong Run, Next Question is Stamina 1-25-24

Tale of the Tape: Trump vs. Biden 12-4-23

Construction Spending: Timing is Everything 12-1-23

3Q23 GDP: Fab Five 11-29-23

Fixed Investment in GDP: The Capex Journey 10-30-23

GDP 3Q23: Old News or Reset? 10-26-23

Construction: Project Economics Drive Nonresidential 10-2-23

GDP 2Q23: The Magic 2% Handle 7-27-23

1Q23 GDP: Facts Matter 6-29-23