Trade: Oct 2024 Flows, Tariff Countdown

We update the running US goods trade deficit, trade partner rankings, and break out the Top 15 imports and exports.

You just sunk my cost structure…time for capex cuts and layoffs?

We update key trade deficit and import-export numbers for today’s release of Oct 2024 trade flows. The numbers help shed light on what might (or might not) unfold if massive potential tariffs actually hit the three countries that comprise over 41% of total trade, 42% of imports, and 40% of exports.

When we add in the 100% tariff threats against the BRIC countries that jawbone de-dollarization and reserve currency changes, we see more of those in the Top 15 trade partners (e.g. India, Brazil).

If Trump adds in some more Truth Social threats against the EU, the total share of trade could get closer to almost 2/3 of total trade. That said, there have also been earlier threats against 100% of imports. That would be a big fight.

People can play with the trade flow numbers that get released each month, and these include state level exports. The bottom line is that there is a lot of “purchasing power risk” even if some economist/tariff apologists play the semantics game and say, “tariff price spikes are technically not inflation.”

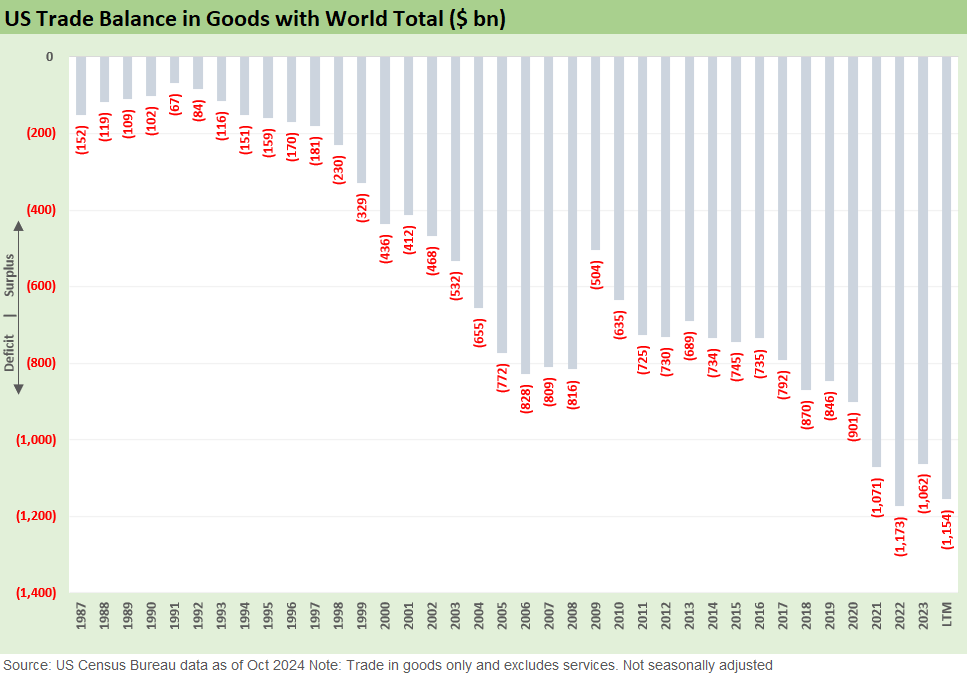

The above chart updates the running annual and LTM trade deficits for trade with the world and shows the numbers back to 1987. Since the late 1980s, we have seen NAFTA, various free trade deals, international tax reform, the rise of China, the increased (then decreased) importance of the WTO, and massive growth in trade and the global economy in general.

Supplier chain development was a recurring theme. From Caterpillar to the legacy Detroit 3 and their Tier 1, 2, and 3 supplier chains, the scramble was on to set up lower cost global supplier chains that allowed US companies be able to compete (labor costs, hedging supplier chain currency risks etc.). That was a priority whether it was to compete with Japan in the 1980s/1990s (CAT vs. Komatsu, Detroit 3 vs. Japan 3) or to face the challenges in trade from China in the new millennium. US companies made the mistake of running wild setting up JVs in China and transferring technology, further putting themselves at risk down the line.

The role of emerging industries (notably tech) and the reliance on Asia suppliers (notably semis but also in regional system integration operations) drove the growing interdependence of the global structure. It is an old story by now as NAFTA and globalization became the enemy of the left and was soon co-opted by the right. The challenging issue when Trump came along was that he saw trade deficits by definition as the enemy. His solution is tariffs. That is not news.

Trump had two new all-time trade deficits in his administration, so it is safe to say he failed to find the magic pill. That was after Bush had a record trade deficit as well (see above chart). Biden also produced 2 record trade deficits with one in 2021 during the economic rebound and another one in 2022. 2024 will likely be another.

When the US economy is doing well, trade deficits grow since we are the largest consuming nation on the planet and low-cost sourcing strategies have been a cornerstone of planning in corporate America. The location of more Japanese and EU transplant operations to the US (e.g. autos) add even more offshore supplier chains.

Even if you don’t like it, the reality of the current structure is more than the “genie getting put back in the bottle.” It is now more the 300-pound lineman that you need to put back in the thimble. The path to get there takes years to even put a dent in it after decades of building it. Trump is essentially asking the private sector – companies and consumers – to pay for his speculative and risky “theories.”

The process needs to start with credible policy perspectives, and that gets off to a rough start when you can’t state clear facts like the “buyer pays” tariffs.

The above chart updates the running list of top trade partners. Sometimes people neglect to spend enough time flagging potential retaliation risk. The “total trade” number is important, but in some cases (e.g. Vietnam, Ireland) imports dominate. The growth in imports from Vietnam raises flags around what the policy will be into 2025. When China came under siege, Vietnam was a major beneficiary as a new offshore address rather than a return to the US. Similarly, Mexico was a beneficiary of low cost nearshoring/friendshoring.

That shift to other nations rather than “return to US” begs the question of what happens when you slap tariffs on Mexico. Do some of those low-cost assembly operations damaged by Mexico tariffs in 2025 just move to Vietnam or some other location that isn’t the US? Or do domestic prices just get raised and the US buyers face higher costs and less volume in total gets bought (the “price elasticity” thing)? Or does Trump finally answer the 1968 draft and fight his first war with Vietnam by placing tariffs on them?

The zero sum game and speculation on sourcing and the ability to replace offshore goods will be around for a while.

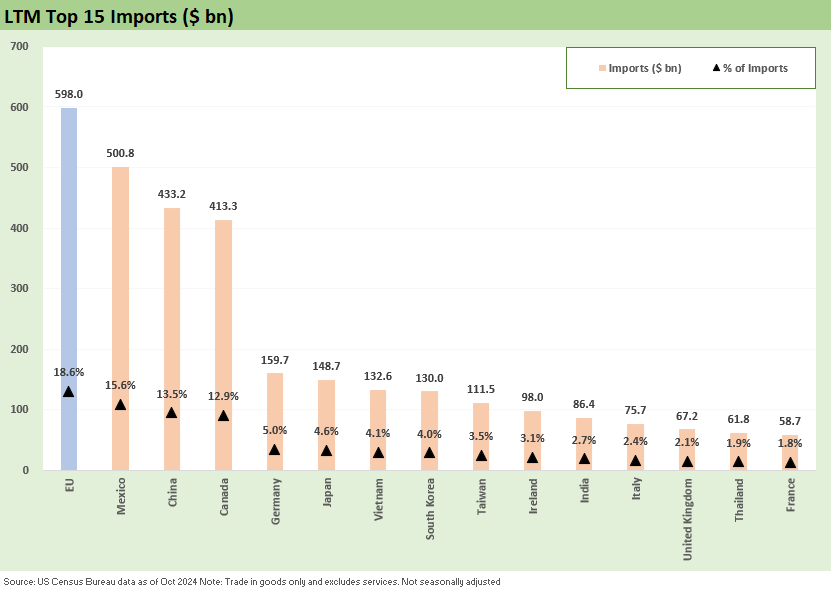

The above chart updates the top LTM importers. The list is more for food for thought. Digging into the product lines is the next layer of the exercise as one would do for any trade partner as we did with recent Canada, Mexico, and China commentaries (see links at bottom).

The above chart updates the Top 15 export trade partners. We include the EU as one trade partner given the reality of how they operate in tariff situations, and we also break out individual European countries that make the Top 15. We would note this list is the “retaliation target” for those who get hit with import tariffs. The main events are EU, the legacy NAFTA/USMCA partners, and various Asian and BRICs countries. The numbers add up.

Glenn Reynolds, CFA glenn@macro4micro.com

Kevin Chun, CFA kevin@macro4micro.com

See also:

Tariff: Target Updates – Canada 11-26-24

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Tariffs: Questions that Won’t Get Asked by Debate Moderators 9-10-24

Facts Matter: China Syndrome on Trade 9-10-24

Trade Flows: More Clarity Needed to Handicap Major Trade Risks 6-12-24

Trade Flows 2023: Trade Partners, Imports/Exports, and Deficits in a Troubled World 2-10-24

Trade Flows: Deficits, Tariffs, and China Risk 10-11-23