3Q24 GDP Update: Bell Lap Is Here

Robust PCE growth and equipment investment tell a good story that looks better with sub-2% inflation for 3Q24 at 1.5% vs. 2.5% in 2Q24.

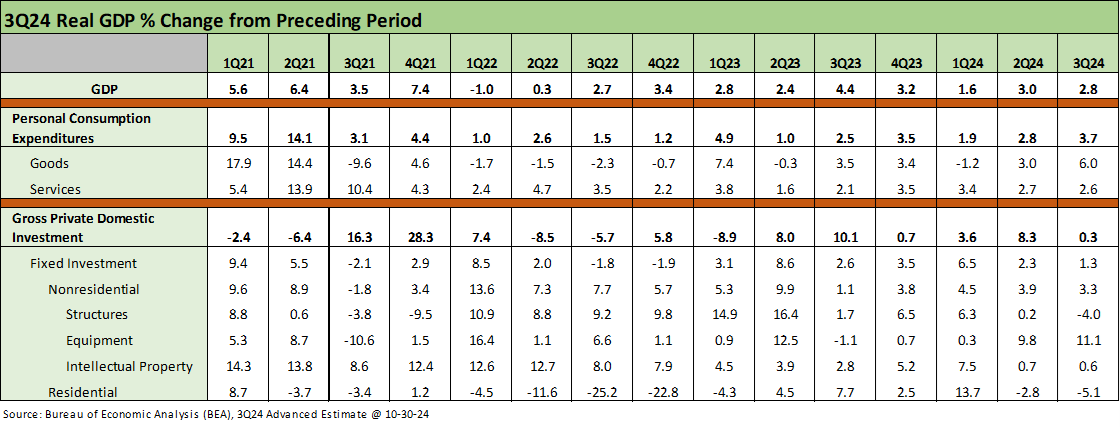

Speed and endurance good so far in the consumer sector…

For the latest 3Q24, the +2.8% headline number includes a very strong +3.7% for PCE along with a robust +11.1% in Equipment and +14.9% in National Defense with some offsets such as Residential Investment at -5.1%

The +2.8% headline GDP growth comes with a -0.73% haircut for trade deficits and private inventory liquidation, so it is better than it looks.

The 3Q24 also brought a lower sequential price index for gross domestic purchases at +1.8%, down from +2.4% in 2Q24 while the PCE Price Index posted +1.5% vs. +2.5%. Core PCE weighed in at +2.2% vs. +2.8%.

Income has been trailing lower with real disposable income at +1.6%, down from +2.4%. DPI was at +3.1%, down from +5.0%.

The above table runs across the quarters from 2021 through 3Q24 with more than the typical range of revisions running through back quarters including 2021 and 2022. The main takeaway is that the most important metrics we watch – PCE and Fixed Investment – have held in well.

The +3.7% in PCE will get a fresh round of data this Friday with the Personal Income & Outlays report. The old theme of “never bet against the US consumer” seems to be playing out for now. That is, until the election gets 50% of the country (whoever wins) pissed off and potentially reconsidering their consumption plans. The same is true for small business and mega global players with their extended supply chains who potentially will be staring down the barrel of massive and widespread tariffs in 2025. Such uncertainty on a much smaller scale promoted caution in 2018-2019.

A few questions and topics that we cannot help but consider with political tensions so high in this last stretch to Election Day:

Mass deportation: How will somewhere between 2 million and 21 million people who could face mass deportation consider their risks. That is quite an estimate range. Trump has reiterated that process as a “Day 1” priority. He has not been feeding his pet reptile (Stephen Miller) enough meat, so the consumer sector will necessarily be a wildcard into holiday season.

Tariffs: Will the potential for tariffs lead to an acceleration of inventory building ahead of any change in the White House in January and how will that flow into a range of timing questions on working capital and supplier stocking?

Debt ceiling: The Jan 2025 deadline on the debt ceiling could make some difference in government employee defensiveness and the same for retirees on threats to cash flow. Will that wag PCE in 4Q24? Will that flow into areas of the economy such as travel planning, etc. If Trump wins, the start of the Federal employee purge will be unfolding soon enough. This is not a partisan comment. It is clearly stated as a goal.

There will be much to take fresh looks at in the weeks after the election. When it comes to GDP growth, consumer behavior, fixed asset investment, government spending plans (defense budgets, etc.) the alternative templates are getting dusted off. The economic plans of the two candidates are starkly different, and many have just tabled those risk exercises in a wait-and-see move.

See also:

2Q24 GDP: Final Estimate and Revision Deltas 9-26-24

2Q24 GDP 2nd Estimate: The Power of 3 and Cutting 8-29-24

Presidential GDP Dance Off: Clinton vs. Trump 7-27-24

Presidential GDP Dance Off: Reagan vs. Trump 7-27-24

GDP 2Q24: Banking a Strong Quarter for Election Season 7-25-24

State Unemployment: A Sum-of-the-Parts BS Detector 6-30-24

1Q24 GDP: Final Cut Moving Parts 6-27-24

Construction Spending: Stalling Sequentially at High Run Rates 6-4-24

1Q24 GDP: Second Estimate, Moving Parts 5-30-24

1Q24 GDP: Looking into the Investment Layers 4-25-24

1Q24: Too Much Drama 4-25-24

4Q23 GDP: Final Cut, Moving Parts 3-28-24

4Q23 GDP: Second Estimate, Moving Parts 2-28-24

GDP and Fixed Investment: Into the Weeds 1-25-24

4Q23 GDP: Strong Run, Next Question is Stamina 1-25-24

Tale of the Tape: Trump vs. Biden 12-4-23

Construction Spending: Timing is Everything 12-1-23

3Q23 GDP: Fab Five 11-29-23

Fixed Investment in GDP: The Capex Journey 10-30-23

GDP 3Q23: Old News or Reset? 10-26-23

Construction: Project Economics Drive Nonresidential 10-2-23

GDP 2Q23: The Magic 2% Handle 7-27-23

1Q23 GDP: Facts Matter 6-29-23