Trade Deficits: The Moving Parts and Macro Goals Matter Most

The commentary on the material YTD decline in trade deficits often misses the point –usually by design.

We have heard plenty of commentators claim that the shrinking trade deficit proves “the Trump plan” is working. That view shows how little progress has been made in applying reality checks to tariffs and trade flows. If the policy is working, the evidence should show up in the real economy, jobs, specific subsectors, corporate earnings in affected industries, and the consumer “price experience.”

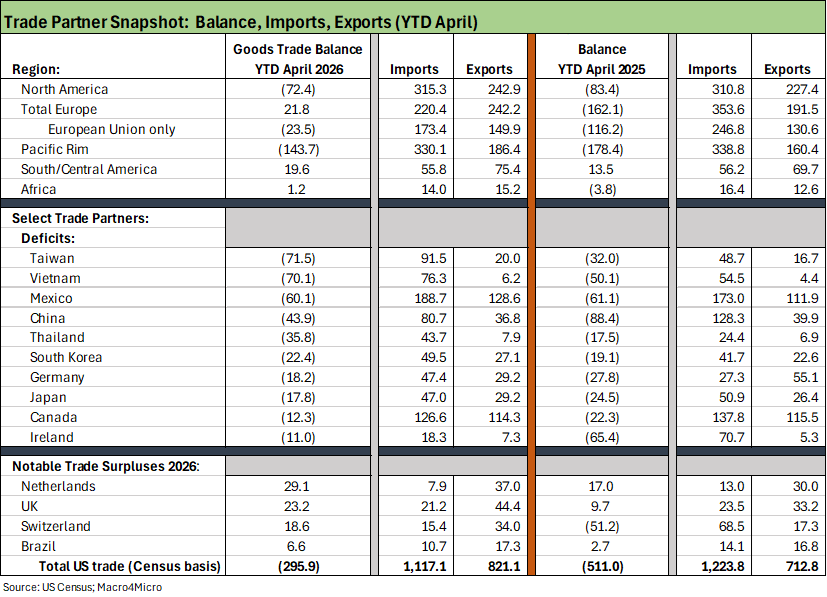

We look at some notable April 2026 trade deficit and import/export lines (the 1-month lag means April is the most recent available) to shed some light on what is behind the material decline in the total trade deficit. The main variances are out of Switzerland, Ireland, and China for various reasons that still do not amount to a major US macro success story.

If the goal of tariffs was just to make the trade deficit lower, that is “success with an asterisk” since it is supposed to be traced to reshoring and increased manufacturing jobs in the BLS release. That is not happening.

There is also the simple reality that an increased goods trade deficit has usually been a sign of a strong US economy and increased demand. The flip side is the goods deficit typically has declined in weak economies (just look at the post-crisis years). With +1.6% GDP growth and +1.4% growth in personal consumption expenditure in 1Q26 (as of the 2nd estimate) then the flip side may be a part of the explanation (notably with China). The tariffs did not help as prices have been rising along the supplier chain (see Trade Deficits: Math Challenge 1-30-26).

The trend line in 2026 has a range of distortions tied to pre-buying in 2025 ahead of tariffs and IEEPA. We also see some idiosyncratic variables by country such as the flow of gold (e.g. bullion imports) with US-Switzerland showing a massive deficit in 2025 on gold flows and pharma/medicines (see Switzerland-US Trade: A Deficit that Glitters 2-3-26).

If there was ever an easy example to show that a higher trade deficit can be good, we can cite the exploding trade deficit with Taiwan that has fueled the tech boom and capital markets gains (see US-Taiwan Trade: Risks Behind the Curtain 2-1-26). Just wishing that all the semiconductors were made in the US misses the point. There was a reason that US multinationals chose Taiwan in a free and open market. Bemoaning the location of the semiconductor supplier chain is somewhat like wishing the US was energy self-sufficient in 1974. Reality matters.

The above chart highlights the line items across goods trade deficits, exports, and imports for the 4 months YTD 2026 vs. the like period of 2025. We show the total lines as noted and detail exports and imports for each region and the major trade partners in the sample.

We also frame the trends at some trade partners where trade surpluses exist YTD. That includes Brazil, where Trump slapped on high IEEPA tariffs to extort the release from prison of his “coup bro” (US-Trade: The 50% Solution? 7-10-25). We see the surpluses grow in the 4 trade partners presented.

The full product line recaps are for another day, but pre-buying, energy flows, and aircraft are typical drivers for these surplus nations. The export deltas are part of the story for the Netherlands, UK and Switzerland with lower imports in 2026 for all 3 (dramatically so for Switzerland). We will get into those again for 2026 after more time has passed since the same distortions will apply. We offer some product line mix details in numerous commentaries in the links below.

The tariff Swiss miss on concepts…

The surplus YTD with Switzerland is an especially unusual case given the massive trade deficit in 2025 as relative macro panic sent a flood of gold bullion flowing into the US (the Swiss are the gold refiners, the US exports raw gold). The Swiss are also major exporters of pharma/medical supplies where imports from Switzerland experienced heavy pre-buying ahead of the planned punitive tariffs. That clearly distorted the 2025 goods deficits with numerous trade partners. The swing from a major trade deficit with Switzerland through April 2025 into a surplus generated a variance of almost $70 billion through 4 months.

Saint Patrick should have driven the snakes out of Washington …

The other extreme outlier was Ireland with a trade deficit swing of around $54 billion in another case of tariff threats and pre-buying (see Tariffs: Enemies List 3-6-25). Pharma and medicines (not Guiness and butter) have been a major part of the trade deficit story with Europe and especially Ireland. There is no question there is a low base of exports to Ireland from the US, but the pharma imports into the US had been massive. The Swiss and Irish trade deficit variance is around 58% of the total.

China keeps diversifying away from US, but tariffs still bite the consumer…

The other big variable in the trade deficit swing was China with a decreased deficit of -$44.5 billion. If we add in the China deficit delta with Switzerland and Ireland, that comprises over 78% of the total deficit deltas. Separately, Vietnam adds $20 bn into the YoY deficit.

The trade flows with China have always been a big deal in the macro picture with China’s exports to the US long-considered a restraint on US inflation and a godsend to those looking to build out low-cost global supplier chains whether for inventory on the shelves or low-cost inputs along the supplier-to-OEM chain. Those global supplier chains have been a core part of textbook “lean manufacturing.”

That ready access to low-cost China supplies has now been taken off the table with tariffs. We have described China imports in the past as a “systemic threat to the cost of sales line” and unit costs and inventory cost are rising as a result (see China Trade: Shrinkage Report 1-28-26). Margins will see financial and operational adjustments in 2026-2027.

That China pressure comes even as raw materials and an energy spike associated with the Iran War. The Strait of Hormuz crisis brought reverberating disruptions across petrochemicals, inorganic chemicals, the oil/refined products supply chain, freight and logistics costs, and metals.

Questions to ponder on tariffs to filter the nonsense…

We have written plenty on the topic of tariffs, but we would cite a few easy questions to revisit when someone makes a blanket statement on Trump’s tariff policy “working.” Hope is different than reality in economic terms.

Is the goal only to reduce the trade deficit?

If the conclusion is only to reduce the deficit, then there is a need for an “Intro Econ Primer” with a tutor who speaks very slowly. The deficit is a net number, so the related questions are easy enough to ask on imports and exports. Oil and LNG going much higher is just one line of many. The higher export of energy was caused by a war that had costs as well. We add in a few more questions in the import vs. exports product topics:

Is the goal to just lower imports or raise exports?

In what product classes?

If the US is the largest consumer market in the world, is a spike in exports even possible for many product lines when the target trade partners have low-cost labor?

Does the US have the ability to provide substitutes to replace that import line facing a tariff?

How do currency trends factor into the import-export flows?

Is the goal to reduce low-cost sourcing opportunities for businesses and consumers?

No party would admit that as a goal, but that is the effect even if not a stated goal. Trump will not even admit that the buyer writes the check for the tariff. He even claimed (in social media posts) that IEEPA refunds would go to the sellers (presumably someone might have informed him that was wrong).

Does the labor arb essentially make it impossible for the US to compete in some product lines?

This is the case with China and Mexico for many assembly line goods such as auto parts and some electronics. The same is true in apparel for low-cost Asian supplier chains. This labor arb will be a focal point when Trump potentially drops the hammer on Mexico in the USMCA review (or termination, which he believes he can do without Congress).

In the end, the absence of low-cost supplier chain alternatives comes out of the profit margins of importers or the pockets of households – or both.

Is the goal to make the consumer pay more for goods and services by increasing pricing power of US companies?

This is another topic where tariff fans will not admit the risks. Since the buyers get hit with a tariff they must pay, the importers or OEMs facing higher cost suppliers need to mitigate the tariff effects to offset them in whole or in part. Without adequate US substitutes, the price pressures could flow into higher prices and reduced affordability.

That price upside could be one-time effects or phased in and thus may not meet the “econ nerd’s” definition of inflation (recurring price pressures). It is still a running expense line that impacts importer cash flow, and the affordability of the household basket along with the corporate “cost of sales” line.

In the event of tariff mitigation strategies, the effect can also lead to downsizing, restructuring or exiting product lines where the tariffs bite.

Is this all just a waiting game until other executive actions by the “next President” and Congress?

The US trade regime is a case of “live by the executive order, die by the executive order” since Congress has been bypassed. That opens up a wide range of “promises to be made later” in future campaigns. Such time horizon unpredictability complicates the planning issue of long-term capex planning when executive orders can be so easily reversed.

Tariff commentary and some historical links:

After a tumultuous period in tariffs after the 2024 election and with a lot more change to come with the USMCA, we add some links below.

The factual misstatements and abandonment of basic concepts have been hallmarks of the process since 2018. Many GOP leaders whisper in corners about what is factual but will not be vocal on the economics.

We did not think it should be so hard to get a Secretary of Treasury or the head Trade Rep to make a simple statement such as “the buyer writes the check for the tariff.” Then he can explain the effects along the economic chain. Even CNBC tends to wimp out on the follow-up questions to keep GOP dignitary guests coming back. Lame.

We attach a collection of the tariff commentaries below.

Switzerland-US Trade: A Deficit that Glitters 2-3-26

US-Taiwan Trade: Risks Behind the Curtain 2-1-26

Trade Deficits: Math Challenge 1-30-26

China Trade: Shrinkage Report 1-28-26

Mexico Trade: Gearing up for More Trade Trouble? 1-27-26

Canada-US Trade: Trump Attack N+1 1-25-26

US-Canada Trade: 35% Tariff Warning 7-11-25

India Tariffs: Changing the Music? 7-11-25

Taiwan: Tariffs and “What is an ally?” 7-10-25

US-Trade: The 50% Solution? 7-10-25

Tariff Man Meets Lord Jim 7-8-25

South Korea Tariffs: Just Don’t Hit Back? 7-8-25

Japan: Ally Attack? Risk Free? 7-7-25

US-Vietnam Trade: History has its Moments 7-5-25

US Trade in Goods April 2025: Imports Be Damned 6-5-25

Tariffs: Testing Trade Partner Mettle 6-3-25

US-UK Trade: Small Progress, Big Extrapolation 5-8-25

Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25

Trade: Uphill Battle for Facts and Concepts 5-6-25

Tariffs: Amazon and Canada Add to the Drama 4-29-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

Tariffs: Some Asian Bystanders Hit in the Crossfire 4-8-25

Tariffs: Diminished Capacity…for Trade Volume that is…4-3-25

Reciprocal Tariff Math: Hocus Pocus 4-3-25

Reciprocal Tariffs: Weird Science Blows up the Lab 4-2-25

Tariffs: Enemies List 3-6-25

US-Mexico Trade: Import/Export Mix for 2024 2-10-25

Aluminum and Steel Tariffs: The Target is Canada 2-10-25

Trade Exposure: US-Canada Import/Export Mix 2024 2-7-25

US Trade with the World: Import and Export Mix 2-6-25

The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25

Tariffs: Questions to Ponder, Part 1 2-2-25US-Canada: Tariffs Now More than a

Negotiating Tactic 1-9-25

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariff: Target Updates – Canada 11-26-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24