US Trade with the World: Import and Export Mix

We look at the major product groups in the import/export mix between the US and the world.

We already framed the 2024 trade flows, goods deficits, and major trade partner numbers, so we look at the major product categories for imports and exports between the US and the World (see The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25).

White House economists and the GOP fellow travelers on tariffs would rather broom water up a hill than try to get Trump to discuss comparative advantage or debate him on his version of facts (e.g. his belief that seller pays, not the buyer). They also don’t spend much time on the multiplier effects across waves of payroll, service providers, and a wide range of industries. Those are not friendly to the “tariff pitch.”

There is the fundamental question around whether erratic tariff policies and social media harassment of major companies is actually an aphrodisiac for direct investment in the US or a disincentive when the “next guy” might change the policies. Is it better to wait and let the tariff plan fail? That means there are likely to be time lags in the great reshoring wave and “build in America or else” coercion strategy.

We will follow up with Canada, Mexico, the EU, and China in other notes on the final import-export product mix for 2024. The topics force one to think about the facts in the context of product line tariff exposure and not “political story time.” The data provides a means of checking the veracity of what comes out of the political realm (see Tariffs: Questions to Ponder, Part 1 2-2-25).

The above chart highlights what the economic toll could be if the US slaps tariffs on imports in some categories that are very near and dear to household economics. Those imports have multiplier effects on the broader economy. The decisions that could unfold and drive tariff battles (or wars) could shoot major industries and the broader economy in the foot. Tariffs by definition raise costs for buyers and could flow into reduced affordability or earnings dilution along the chain depending on whether costs get passed on.

The recurring political counterpoint is “look at past markets where it did not happen” to deflect the questions about “who pays.” Their boss said (in writing and verbally) that the “selling country” pays (“collected billions and billions from China”). Tariff supporters need to avoid the words “buyer pays.”

It is always important to look at multiple variables in each economic cycle. Each economic backdrop is different. The pricing power can vary, and that determines how quickly costs can flow through into prices. The price impact can lag. The fact is that corporations saw slower capex and exports suffered in the last tariff experiment. That is why the FOMC eased in 2019 (the Fed said so). Those tariffs also were lower and less sweeping than what Trump has now put out there in “Maybe Land.”

The Trump tariff apologists also tend to ignore the stinging reality check of the post-COVID period on what supply-demand imbalances can do when demand is strong and pricing power available. Debating whether the cause is supply, demand, pricing power or costs eventually devolves into the absurd language game. Some remind us of the old question list: “Did the fall kill you or the gravity?” “Was it the smoke or the fire?” “Was it the knife or the blood loss?”

Think higher costs and higher prices…

We are not doing the Full Monty in this piece on the import-export mix with the world, but the above import chart is revealing. The top 5 import lines show Autos at #1 just edging out Pharma at #2 with crude petroleum a distant #3 (dominated by Canada), Computer Equipment at #4, and Semiconductors at #5.

Autos at #1 are a debate for another day. The history of global OEMs and supplier chains is a big topic with a record transplant presence on US soil. The auto sector has been in a battle around import share since Japan started racking up market share in the 1970s before starting decades of transplant expansion.

Autos are the #1 import from Japan, #1 from South Korea, #1 from Mexico, #2 from the EU (#1 from Germany), and a very distant #2 from Canada. The question is whether the US economy wants to die on that hill when autos and auto retail is doing so well this year and capex on EV and battery plants has soared – notably in red states. The EV is also now a question mark. Autos are for another day.

Pharma at #2 is a critical risk factor with EU importers showing Pharma at #1. For China, it is #11. The question there is how many substitutes are available and what could damage the Pharma supply chain from China. That risk factor gets a lot of focus from bears and fat tail prognosticators. Pharmaceuticals are always a worry given the health link. Broad tariffs there would be crushing for inflation and how that flows into household budgets, health care costs and Medicare among other contentious areas in US politics.

On computer equipment at #4, some might be surprised that is the #2 category on the Mexico import list. That raises the topic of the “labor arb” and low-cost labor for assembly. The same holds true for autos. That topic is a major variable in so many of the import lines in Asia including China and Vietnam. Computer equipment is also #2 on the China list with a much higher gross number. That “race to the bottom” angle is what gives it more bipartisan political legs.

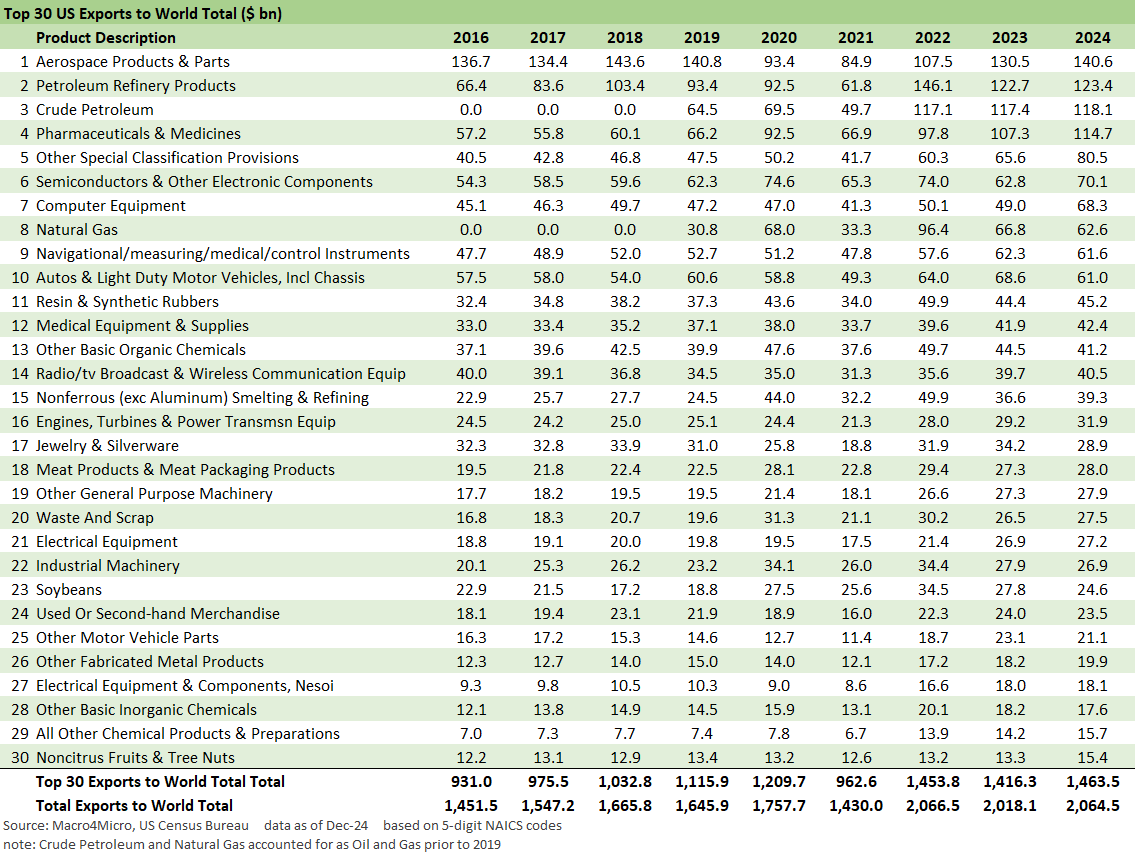

The export mix does not change much across the year from month to month, but the Aerospace business has historically been a leader until oil imports were allowed and has now extended to record exports of oil and gas products. The line items were broken up in recent years across refinery products, crude, and natural gas. Canadian crudes selling at material discounts to US grades have very strong demand from US refineries.

The critical aerospace export market could make for a tempting target in the EU and China on future commitments to Boeing, who is having enough trouble getting some aircraft certified. The risk of Trump attacking other major carrier home nations might lead to a change of heart on commitments existing and future. Airbus will not be standing still and China continues to work on finding its way into the top tier in airplanes with COMAC and make it a triopoly.

There is every reason to expect growth in US energy exports to continue, but attacking the EU might inspire them to be more cautious in buying from the US. It also might inspire Canada with its domestic political battles to be open to allowing more oil to reach tidewater and more international markets whether in the West (expand current capacity) or the East (unlikely, massive domestic opposition). Canadian crude is heavily landlocked and facing opposition to pipelines in both countries (Keystone saga etc.).

Tariff links:

The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25

Tariffs: Questions to Ponder, Part 1 2-2-25

US-Canada: Tariffs Now More than a Negotiating Tactic 1-9-25

Trade: Oct 2024 Flows, Tariff Countdown 12-5-24

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariff: Target Updates – Canada 11-26-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Facts Matter: China Syndrome on Trade 9-10-24

Trade Flows: More Clarity Needed to Handicap Major Trade Risks 6-12-24

Trade Flows 2023: Trade Partners, Imports/Exports, and Deficits in a Troubled World 2-10-24

Trade Flows: Deficits, Tariffs, and China Risk 10-11-23