Footnotes & Flashbacks: Asset Returns 11-17-24

We update running asset returns after a few bad weeks and a single spectacular week for equities as duration lags.

Did 50.1% of the country vote for this? We doubt it.

A bad week for equities and bonds came with a mixed inflation report, solid retail sales, and a weak industrial production report. The net effect of a bear steepener on the week weighed on the Mag 7 and drove soft numbers across large caps, midcaps, and small caps.

The excitement of the election and lower regulatory headwinds for many industries in terms of costs and M&A barriers is starting to give way to the reality of some very strange appointments that signal “Trump meant what he said.” The rationalization on “rhetoric vs. action” is losing some ground, and potential economic damage will need to start finding its way into risk pricing.

Things got strange quickly as the AG nominee (Gaetz) displays an adoration of Trump that is shared by Trump (of Trump, that is) and perhaps some common proclivities. The signals for chaos in trade/tariffs and mass deportation might not be what 50.1% of the nation voted for as opposed to what many voted against (or stayed home). He did warn you.

A fear of chronic White House interference at the company level (remember Harley and Amazon in the last administration and more recently Deere?) could also weigh in on strategically critical industries such as the defense sector and their supplier chain with the related multiplier effects in tech innovation.

A Fox & Friends host is teed up to purge the military leadership and be in control of the largest and most powerful military in the world with a budget exceeding the next 10 nations combined. Meanwhile, an unqualified anti-vaxxer who was never elected to office or held a major executive corporate position will hold sway over a broad health care sector that comprises around 18% of GDP.

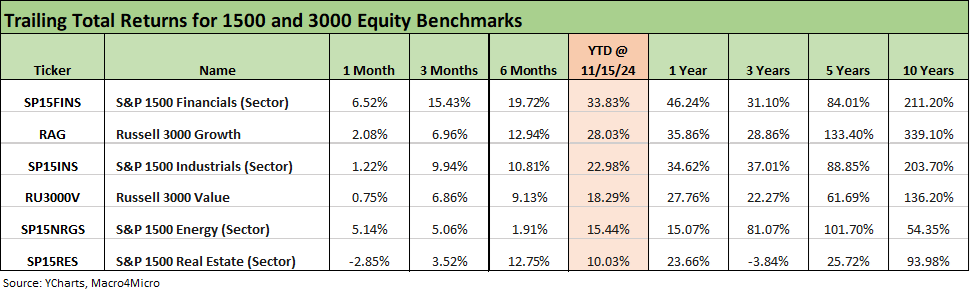

The above chart details time horizon returns for the benchmarks we cover in debt and equities. For the month, we see 3 of 4 in the red for debt and the pace of the equities fading in part after such a major post-election bounce last week.

There are many extremely conservative and highly accomplished leaders in finance, law, and health care, so this week’s appointments are a buzz kill for those hoping for prudent, intelligent and conservative government. Instead of tapping the A-Team, Trump seems determined to recruit from the Extreme Scream Team.

As we covered in the CPI commentary, this will feed the fear of worst-case scenarios on trade/tariffs and deportation with all the related macro and micro level fallout (see CPI Oct 2024: Calm Before the Confusion 11-13-24).

The above chart updates the 1500 and 3000 series, and the week saw some setbacks for small caps with Energy the only one showing a higher rolling 1-month number and Real Estate falling back into the red. Value took a hit and so did Industrials for the rolling 1-month and 3-month periods. Whether the anxiety around rates or policy risk or protecting year end performance, there are certainly a wide range of possible outcomes ahead. That is the case for those wrestling with hiring plans and capital budgeting decisions.

The rolling return visual

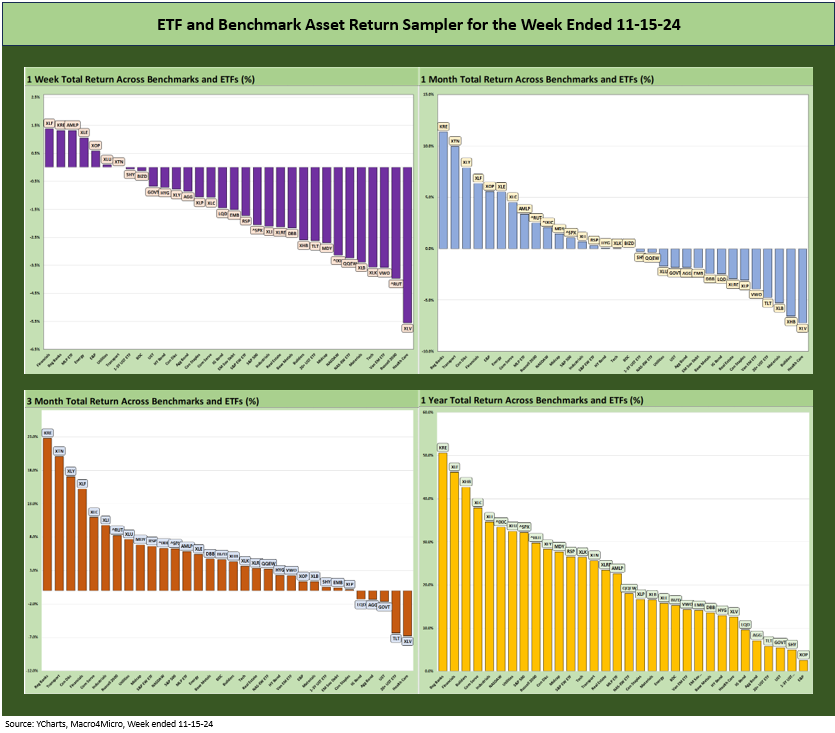

In the next section, we get into the details of the 32 ETFs and benchmarks for a mix of the trailing periods. Below we offer a condensed 4-chart view for an easy visual on how the mix of positive vs. negative returns shape up. This is a useful exercise we do each week looking for signals across industry groups and asset classes. We also have a YTD version that we include in the broader commentary on the time horizons further below.

The above chart shows a setback coming off a very impressive prior week with the election getting the Trump trade fans very bulled up. The 1-month returns are more divided. The 3-month, YTD (not shown above but covered below), and 1 year time horizons have been very solid with the start of the easing cycle and also due to a healthy economy and a breadth of growth driven both by the consumer and by fixed asset investment coming off the inflation peaks and the back end of the tightening cycle (see 3Q24 GDP Update: Bell Lap Is Here 10-30-24, PCE Inflation Sept 2024: Personal Income and Outlays 10-31-24, Fixed Investment in 3Q24: Into the Weeds 11-7-24).

The relative weightings of positive vs. negative remind us in the 1-week and 1-month returns that we are entering a period of material uncertainty – on the yield curve, policies in the White House generally, on trade/tariffs, the scale and pace of mass deportation, and on geopolitics from China to Russia/Ukraine.

We also cannot take for granted how the Saudi and Iran relationships will evolve and whether the Saudi-US “soft ties” will be maintained when the Secretary of Defense nominee (a Fox & Friends host with no senior command or major institutional governance background) has delusions that he is one of the Knights Templar (deus vult, God wills it!).

Medieval scholars have not had this much excitement in years explaining how right wing extremists have coopted religious symbols (they are very big on the Templar’s deus vult cross and Jerusalem cross, both of which adorn the Defense nominee’s body). They have also embraced a fair amount of Norse imagery and even the Detroit Red Wings symbol has not escaped abuse. Toggle around images on the web. Start with “deus vult cross” and “white supremacy Christian symbols.” The visuals speak for themselves (when JD Vance is not speaking for them, that is).

This drama will heat up quickly and set the stage for the ugliest stretch of politics since the Civil War. It comes at a cost. Trump has requested the Senate abandon their constitutional role. The market cannot stay insulated from this into 2025, but the street will need to stay radio silent on policy and caution.

It is hard to see how the developments will be good for the PCE line as troops round up families and clash in urban environments. Young people might start reading the Diary of Anne Frank and hide in attics waiting for meals. That is, where the book is allowed in the curriculum. On a cold, bloodthirsty note, such chaos is bad for business even if guns/ammo sales and Wild Turkey volumes spike.

The Magnificent 7 heavy ETFs…

Some of the benchmarks and industry ETFs we include have issuer concentration elements that leave them wagged by a few names. When looking across some of the bellwether industry and subsector ETFs in the rankings, it is good to keep in mind which narrow ETFs (vs. broad market benchmarks) get wagged more by the “Magnificent 7” including Consumer Discretionary (XLY) with Amazon and Tesla, Tech (XLK) with Microsoft, Apple, and NVIDIA, and Communications Services (XLC) with Alphabet and Meta.

The above chart shows a shutout for the tech bellwethers this week. NVIDIA reports earnings this week (Wed), so that will be a focal point with fewer major econ releases this week outside of housing. For the past week, we see 3 of the 4 bottom performers tied to chips with Taiwan Semi and Broadcom both negative for the trailing month and Broadcom also in the red for the trailing 3-months.

The breadth in the equity markets has been steady and favorable as we have been detailing along the way. Small caps have been in the top quartile trailing 3 months with midcaps just across the line in the top of the second quartile, where we also find Mag 7 heavy NASDAQ and S&P 500 while the 3-month Tech ETF (XLK) is down in the third quartile with the Equal Weight NASDAQ 100 ETF (QQEW).

We looked at the trailing 1-week returns in the Mini Market Lookback: Reality Checks, and it was a rough week with the top quartile including Regional Banks (KRE) and Financials (XLF) and the three main energy ETFs in the top quartile across Midstream (AMLP), full spectrum services Energy (XLE), and E&P (XOP) back in the top tier.

Utilities (XLU) continue to perform well on fundamentals and resilience in the face of uncertain curve dynamics. Transport (XTN) names are somewhat mixed in forward risk profiles, but Airlines have been strong performers of late. XTN could see some headwinds around trade in 2025 subject to their relative exposures to trade disruptions.

The extremely weak performance of the Pharma-heavy Healthcare ETF (XLV) was notable with the short-term swoon in part tied to fears of RFK Jr. For the Kennedy clan, the talent pool saw some heavy dilution across the decades, and the younger generation gets this version. The competence force is not strong with this one. In the spirit of Camelot, this descendant took sides with Malagant (to the dismay of “the family”), but that is not his main virtue or flaw.

The stakes are high with health care comprising around 18% of GDP, and the lack of experience (despite no lack of opinions) on the functioning of a health care system could come under siege in a potential repeal of ACA. It will be interesting to see how RFK Jr balances his oft-voiced concerns for everyone’s health with their ability to maintain health insurance with all the maladies he routinely cites.

The questions around attracting knowledgeable people to work around him to advise and guide is questionable since he believes his own BS. Many policy spectators struggle with the idea that a trained lawyer who had to take the bar exam three times somehow knows more than all the experts in the medical sciences. The main attribute he leans on is being a member of the “lucky sperm club” with a storied name. The “born on third base” resume will help him fit in with the Trump team.

The 1-month numbers were discussed in broad strokes earlier in the piece, but we see the pressure on the interest rate sensitive equity sectors and all the bond ETFs. We see the long duration UST ETF (TLT) on the bottom of the 7 bond ETFs and housed in the bottom quartile along with the IG Corp Index ETF (LQD) with its longer duration profile. We see the short duration UST 1Y-3Y ETF (SHY) in the third quartile along with EMB, GOVT and AGG. The HY ETF (HYG) was more resilient with its higher coupons and shorter duration in the face of the bear steepening that fell harder on the long end.

The top quartile performers on the month mix in financials and energy and tech. We see Regional Banks (KRE) at #1 and Financials (XLF) in the top 5 with Transports (XTN) riding the airline rally. The 3 energy ETFs (XOP, XLE, AMLP) made the top tier while select Mag 7 heavy ETFs in the upper ranks included Consumer Discretionary (XLY) on the banner Tesla numbers and also Communications Services (XLC).

The above chart highlights the challenging UST performance with 6 of 7 bond ETFs in the bottom quartile and only HY (HYG) making it into the third quartile. Health care was on the bottom as the industry moves into a strange new world of RFK Jr and his theories as a non-scientist. The other bottom tier performer was Consumer Staples (XLP) in its miscast role as a “bond surrogate.”

The 3-month winners see the big gain for financials (KRE, XLF) and rallies in Consumer Discretionary at XLY (Tesla as a 3-month home run and to a much lesser extent Amazon). We see Communications Services (XLC) in the top tier with Disney and Netflix turning in solid numbers among others. Industrials (XLI) also added a nice dose of diversity and cyclical reassurance when combined with banks and financial sectors. The same is the case with small caps in the top quartile.

The YTD story is clear enough and consistent with recent results with a positive vs. negative score of 31-1. We only see the long duration UST ETF (TLT) in the red with the bottom 5 on the list all bond ETFs. This was not a great year for the UST curve and duration as we cover in our separate Footnotes publication on the State of Yields that we will post later.

Financials (XLF) are on top at #1 with Regional Banks (KRE) at #3. Those two saw Communications Services (XLC) split them at #2 with Utilities at #4 followed by the two Mag 7 heavy benchmarks, NASDAQ and the S&P 500. The bottom of the top quartile sees the income-heavy Midstream ETF (AMLP).

AMLP is likely to be in for a busy year when Trump energy policy takes the leash off infrastructure projects and takes record level production and record level exports to new highs that will reshape some of the national security issues and impact decisions in EU around energy sourcing.

The LTM returns post a score of 32-0. We see 6 of 7 bond ETFs in the bottom quartile but all positive and only EM Sovereigns (EMB) making it into the third quartile. We see some returns on the bond ETFs for the LTM period ahead of long-term nominal returns on equity with +14.1% for EMB and just under 13% on HYG with LQD at +9.6%. The rally of Nov-Dec 2023 really helped the running numbers in what was a very strong finish to that year (see (see Footnotes & Flashbacks: Asset Returns 1-1-24 , Footnotes & Flashbacks: State of Yields 1-1-24, Credit Performance: Excess Return Differentials in 20231-1-24).

See also:

Mini Market Lookback: Reality Checks 11-16-24

Industrial Production: Capacity Utilization Circling Lower 11-15-24

Retail Sales Oct 2024: Durable Consumers 11-15-24

Credit Crib Note: United Rentals (URI) 11-14-24

CPI Oct 2024: Calm Before the Confusion 11-13-24

Footnotes & Flashbacks: Credit Markets 11-12-24

Footnotes & Flashbacks: State of Yields 11-11-24

Footnotes & Flashbacks: Asset Returns 11-10-24

Mini Market Lookback: Extrapolation Time? 11-9-24

The Inflation Explanation: The Easiest Answer 11-8-24

Fixed Investment in 3Q24: Into the Weeds 11-7-24

Morning After Lightning Round 11-6-24

Payroll Oct 2024: Noise vs. Notes 11-2-24

All the Presidents’ Stocks: Beware Jedi Mind Tricks 11-1-24

PCE Inflation Sept 2024: Personal Income and Outlays 10-31-24

Employment Cost Index Sept 2024: Positive Trend 10-31-24

3Q24 GDP Update: Bell Lap Is Here 10-30-24

The Politics of Objective GDP Numbers: “Flex Facts” on Growth 10-30-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

JOLTS Sept 2024: Solid but Lower, Signals for Payroll Day? 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Durable Goods Sept 2024: Taking a Breather 10-25-24

New Home Sales: All About the Rates 10-25-24

PulteGroup 3Q24: Pushing through Rate Challenges 10-23-24

Existing Home Sales Sept 2024: Weakening Volumes, Rate Trends Worse 10-23-24

State Unemployment Rates: Reality Update 10-22-24

Housing Starts Sept 2024: Long Game Meets Long Rates 10-18-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24