Credit Markets: The Conan the Barbarian Rule 10-20-25

Another week of political division runs along with a protracted shutdown as the market awaits a single CPI reading.

“For no one – no one in this world can you trust. Not men, not women, not beasts.”

We could not resist invoking the “Conan Rule” in the above visual and link given the absence of economic data and a stream of disinformation on tariffs, the state of the economy and how the consumer is faring. It is always good to get back to the numbers and guidance as 3Q25 earnings roll out. The GOP will say this is the greatest 9+ months in Presidential history and the Democrats will frame the economy as being in freefall, but both extremes are patently false.

The “buyer writes the check to customs” is a fact (denied by Trump again this week) but inflation is not spiraling higher even as it hits select product lines. Headline CPI for August was basically right where it was in Biden’s last full month in office, and we get a fresh set of numbers this week since CPI is an essential number for Social Security COLA.

This week brings GM and Ford, defense and aero, rail/freight, a round of regional banks, telecom, and some major bellwethers such as Netflix and Tesla. 3Q25 is the main game in town with the BLS and BEA in shutdown mode.

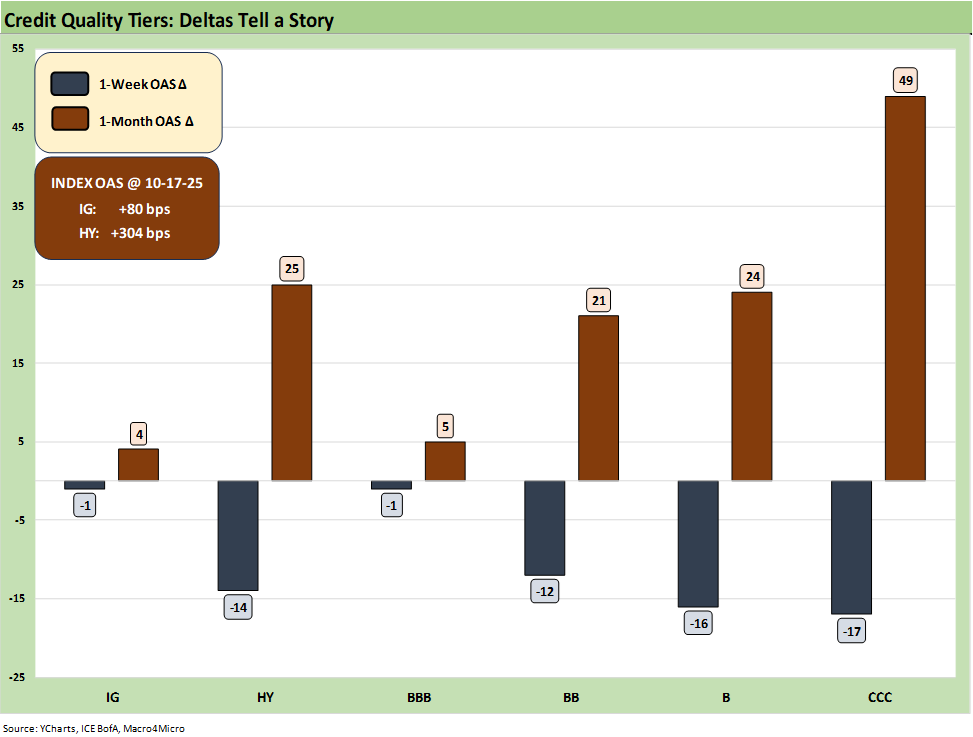

The above chart updates the 1-week and trailing 1-month spread deltas for IG and HY and from the BBB to CCC tiers. Credit risk pricing improved over the week as Trump backpedaled on China threats and the major banks brought solid 3Q25 earnings. We also heard very constructive news on the consumer from bellwethers such as American Express and Synchrony with Cap One teed up for this week with sentiments echoed by JPM and BofA on consumer credit quality in the middle and upper tiers.

While IG spreads were essentially flat on the week at -1 bps, we saw US HY tighten by -14 bps. The 1-month spreads were up slightly for IG at +4 bps with HY up +25 bps. The YTD HY OAS delta rose to +12 bps with IG OAS -2 bps tighter.

The private credit focus and BDC visibility ahead…

The private credit headlines that sent BDC equities into a sell-off over the past few weeks have had little discernible spillover into the HY bond market thus far. With HY OAS at +304 bps, the HY index is only slightly above where June 2007 closed during the credit bubble. That does not constitute credit market anxiety contagion.

The fact remains that most leveraged deals that might have tapped the HY bond market in past cycles migrated over to private credit given the active role played by the major private equity firms. That industry evolution was one factor as was the explosive growth of private credit from high quality to highly speculative.

BDCs are back in the limelight now given their role as a window into private credit. A few one-offs (First Brands, Tricolor) is not an indicator of waves of collapses, but the expectation of a higher rate of private credit restructuring would be intuitive in a material economic contraction. Anyone who has lived in an NYC apartment can tell you even more than a few cockroaches can be dealt with. The full bug infestation takes a lot to go wrong across industries and the broader economy. That is the same old challenge.

Investors will be tapping into the BDC earnings in the coming weeks. BDCs typically offer detailed presentations and Q&A. Hopefully, we will see some extra effort by management teams to arm investors with some inputs and small brushes to avoid painting the sector with a roller. Some big BDCs report in late Oct but the first week of Nov will bring the lion share. The market will be looking for a lot of reassurance on what is happening in the underlying portfolios and investors will be seeking more color on the quality of portfolio marks.

Shutdown dynamics should start to weigh more on spreads…

Meanwhile, the government shutdown continues with no end in sight despite some reassuring words today from the White House. Importantly, the November 1 ACA premium increase announcements are fast approaching.

The House remains closed with Johnson refusing to swear in Adelita Grijalva, the Arizona Democrat who won a special election last month. She would be the swing vote on the Epstein file disclosure which has been heating up with Virginia Giuffre’s book being published this week. As we covered in our curve piece, the goal of the House could be to further incite House divisions into more of a “Hatfields vs. McCoys” profile to get the full GOP in line against any more Epstein file legislative efforts. That intent is disturbing enough on its face from the pseudo-pious leadership (see The Curve: My Kingdom for 10 Cuts 10-19-25).

The willingness of the White House and Vought squad to target major projects as well as radically downsize the employee base (subject to the ongoing union litigation) could start to have more multiplier effects across more sectors and impact more small businesses and contractors. That will not help payroll numbers when they finally see the light of day again. Such actions will also not do wonders for private credit quality given the nature of that borrower profile (small to mid, less access to credit, etc.). A few bad quarters could lead to credit contraction in the small business sector to go with the stress being caused by tariffs that are still rolling in with much more to come.

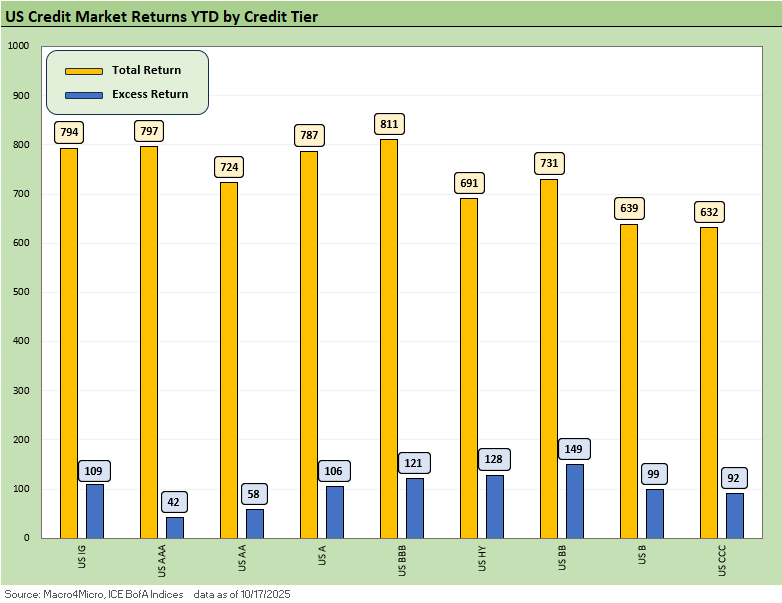

The above chart updates the YTD 2025 excess returns and total returns across IG and HY across the credit tiers. The support of the UST curve is clear enough in the total return numbers. For excess returns, the spread compression gave way to HY spread widening. Last week saw a partial claw-back of some of that widening. The YTD excess returns rebounded slightly, increasing to +128 bps YTD from +99 bps YTD. The IG excess return increased from +96 bps YTD to +109 bps. Duration was rewarded this past week on the mild UST rally (see The Curve: My Kingdom for 10 Cuts 10-19-25).

The BB tier remained in the lead in HY this week for HY YTD excess returns followed by the B then CCC tiers. The excess returns in the BB tier are on top as the BB tier generally is well positioned on the balance of credit risk and duration risk. Duration risk has favored the IG tiers YTD with BBB the winner overall in total return from the combination of credit and UST curve. The middle credit tiers are often seen as “no guts, no glory” for credit risk takers, but it has been and remains a sound risk positioning in the current market.

Credit has been delivering positive trends of late, but one can make an easy case that the risk compensation has played out more favorably for BBs for the risks being taken vs. the lower tiers. This week was obviously a setback with more action to play out in the China clash, shutdown, and with the FOMC.

The CCC tier with its mix of coupons, spreads, and shorter duration had been framing up well in the bar chart until recent weeks. The BB tier remains the clear winner YTD vs. the B and CCC tiers, begging the question of how much better the excess returns in the CCC and weak B range should be given the magnitude of the risks relative to the BBB and BB tiers.

For now, the B and CCC excess returns are falling well short of where their returns should be. The BBB tier also outperformed the B and CCC tier. The risk-adjusted debate tends to get obscured by the discussion of what is the right metric to make that risk-adjusted return assessment.

Note: The most recent data and related comments are in “Recent Trends.” We break out “Historical Context” sections in the Credit Markets and Yield Curve weeklies to roll forward the history and cyclical framework. We do that so new readers do not have to go fishing through links.

Recent Trends:

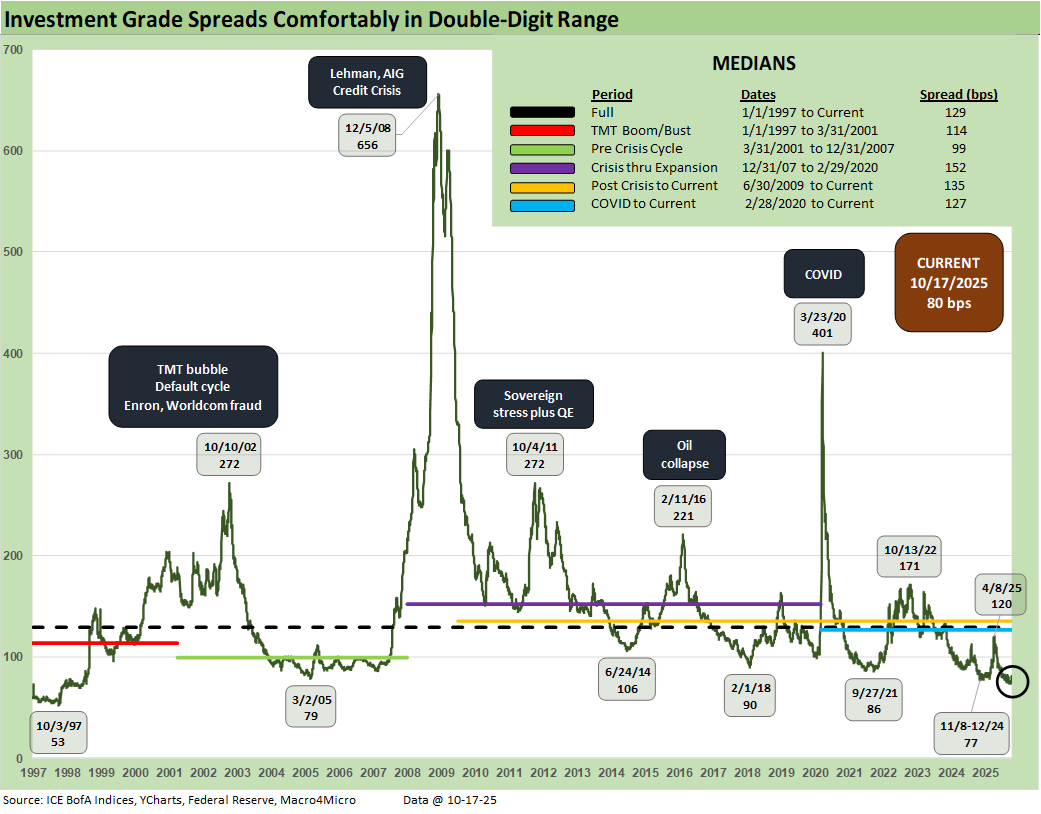

The IG market spread action was very uneventful for the week. We saw spreads tighten on the week for IG by -1 bps to +80 bps with BBBs -1 bps, and the same -1 bps tighter for the A and AA tiers with AAAs tighter by -2 bps. The total face value of the IG index is now almost $9.45 trillion (face value) with recent data showing the A tier edging ahead of the BBB tier in total face value over the summer. The BBB tier is larger than France and the UK GDP but still a few hundred billion short of Germany.

Historical context:

The above updates the multi-cycle spread history for IG as we see the wild swings across time when the banks were in harm’s way in 2008 and the heavy exposure to energy names whipsawed BBB energy in 2015 and early 2016.

The current +80 bps remains above the tights in the mid-70 handles in recent weeks and in Nov 2024 . IG spreads are right around the March 2005 levels just before the auto OEMs started taking a lot of heat with a GM warning in mid-March 2005 (downgrades for Autos later in the year). There is no getting around the reality that IG spreads rarely get this low, but there is plenty of history where they were lower in the late 1990s.

The record lows since 1997 were seen in early Oct 1997 when that year saw a protracted stretch of 60-handle spreads. The market spent time in 1998 in the mid-70s range including the early summer. Life got ugly starting in Aug 1998.

That 1997 low of +53 bps came just before the Asian Yankee bond market started to implode, and the broader regional Asian crisis unfolded. Spreads in 1998 kicked into a correlated beatdown after the Russia default in Aug 1998 did damage to other markets as a contagion effect hit EM credit and US HY valuations. That was the summer and fall of LTCM after the Russian default of Aug 1998. Lehman also saw a mini-panic by Oct 1998 with a funding crunch that they got past quickly. CDS exposure and counterparty risk saw fleeting focus at the time. Counterparty risk lessons were not learned as we saw in the housing bubble and structured finance boom on the way to the 2008 crisis.

Banks and financial services are an anchor today…

Critical drivers of IG spreads are always the banks and financials broadly at over ¼ of face IG value, and the major banks are very sound at this point compared to past recession periods such as Dec 2007 to June 2009, which was an epic meltdown for the banks and brokers. The securities firms ended up merging (BofA+ML, JPM+Bear) or essentially getting sold off in pieces (Lehman) or converting to Bank Holding Companies (Goldman, Morgan Stanley). The days of commercial paper funding of securities firms have given way to deposits, so there is also much less funding risk in the system.

The TMT bubble years of 2000-2002 is the stuff of legend. Earlier, the infamous 1980s LBO reckoning and the commercial real estate stress of 1990-1993 came not long after the thrift crisis and oil patch collapse slammed many banks and S&Ls.

The COVID crisis was a very different beast, but the market benefited from a well-positioned Fed with a crisis-period toolbox to pull out. How the Fed will be governed or legislated under the shadow Project 2025 priorities (see Chapter 21 and 24) will be a critical variable into 2026 when the new team is in place.

What Trump wants to do with his loyalists at the helm is unclear except for the initial 300 bps in fed funds cuts he demanded (now 275? Soon to be 225 bps by Jan 2026?). He most definitely will not receive such an outsized series of cuts without a massive crisis in the markets, which would not bode well for his “clout” if they blame his economic policies.

Recent Trends:

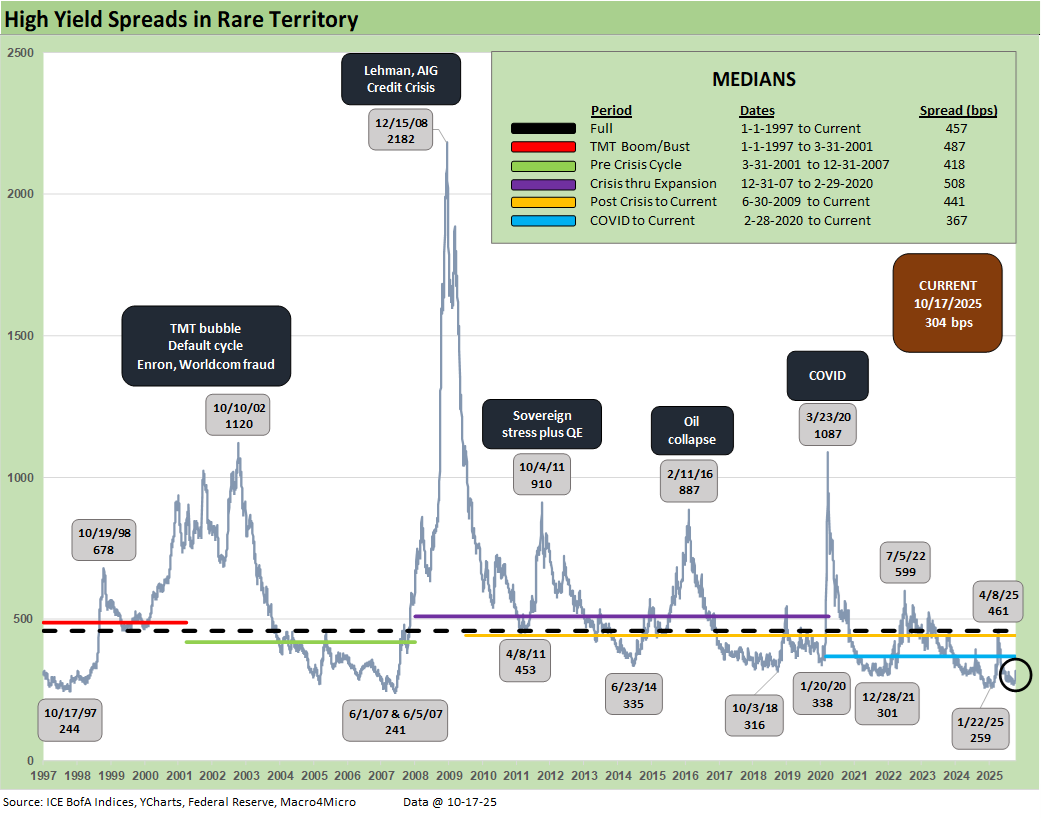

HY OAS saw a -14 bps move tighter on the week, which brings the YTD widening to +12 bps. The 1-month change is at +25 bps wider. We cover the credit tiers in more detail further below.

Historical Context:

The past week’s HY move to +304 bps on subsiding China anxiety plus solid bank 3Q25 earnings remains inside the COVID-to-current median of +367 bps and well below the post-Liberation Day spike to +461 bps. We’re now in the territory of late 2021 and with the recent sub-300 tights back on the table if Trump and Xi come to reasonable terms, the shutdown ends, the FOMC eases twice, and we can get economic data again.

Getting all these challenges to fall into place favorably is a big ask given the scale of the political dysfunction and Trump’s sensitivity around being tough on China with tariffs. China is the only trade partner that can stand up and defend their position in the same weight class as the US. Meanwhile, the IEEPA weapons in tariffs will be before SCOTUS in early November.

Today’s HY market presents a much healthier credit mix than in June 2007 when LBOs had gone off the charts and were partly funded with HY bonds. In the current market, those highly leveraged transactions have migrated over to private credit, which is generating some ugly headlines right now on a few deals.

The HY bond index default cycle is very much in check. The distress and debt exchange actions will be weighed more heavily (and for the most part quietly) over in private credit as the year plays out. That said, we have two very noisy private credit situations (Tricolor, First Brands) playing out in the headlines in recent days with the potentially massive fraud chatter around First Brands and some grim commentary around Tricolor. We have seen subprime auto finance defaults before – even in IG commercial paper issuers – so that is not a Loch Ness moment.

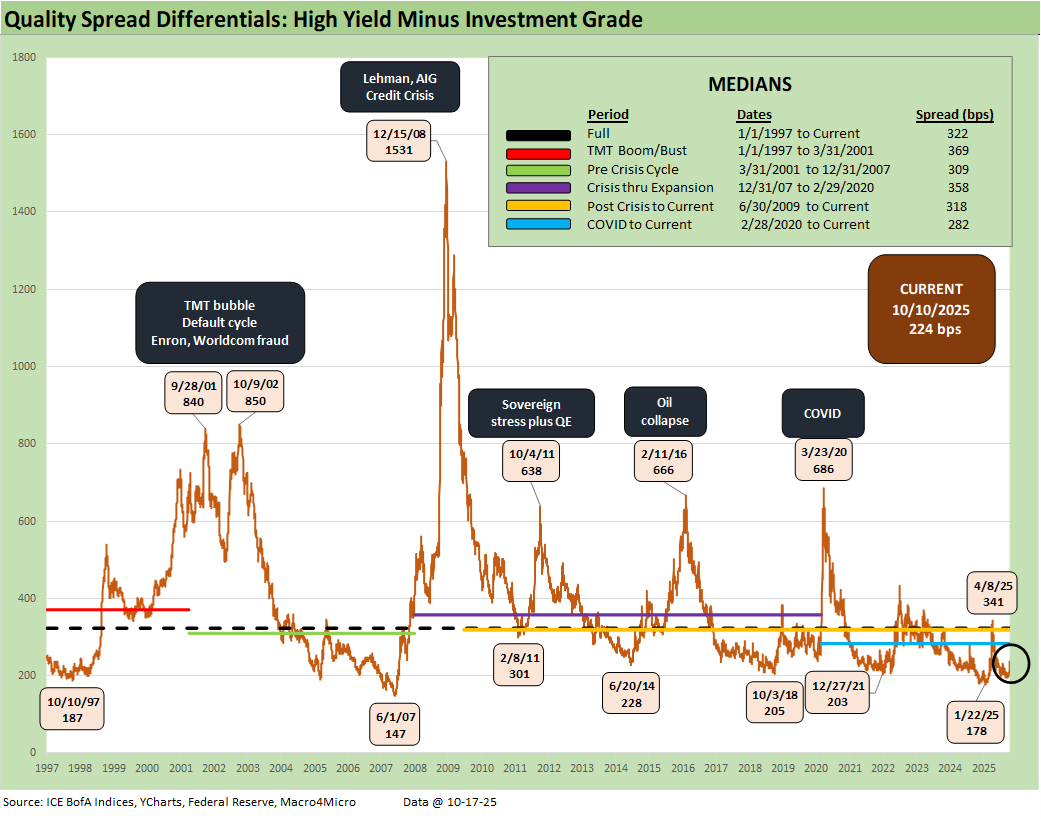

The “HY OAS minus IG OAS” quality spread differential of +224 bps is above the tights of +178 bps seen in Jan 2025 and materially higher than the +147 bps in June 2007. The +224 bps is more in line with the credit cycle mini-peak in June 2014.

We see the peak of +341 bps after Liberation Day vs. a long-term median of +322 bps. Most of the cyclical timeline medians noted in the box had 300-handles, so despite recent widening, the trend overall still highlights that quality spreads are offering very low compensation for moving down the credit tiers.

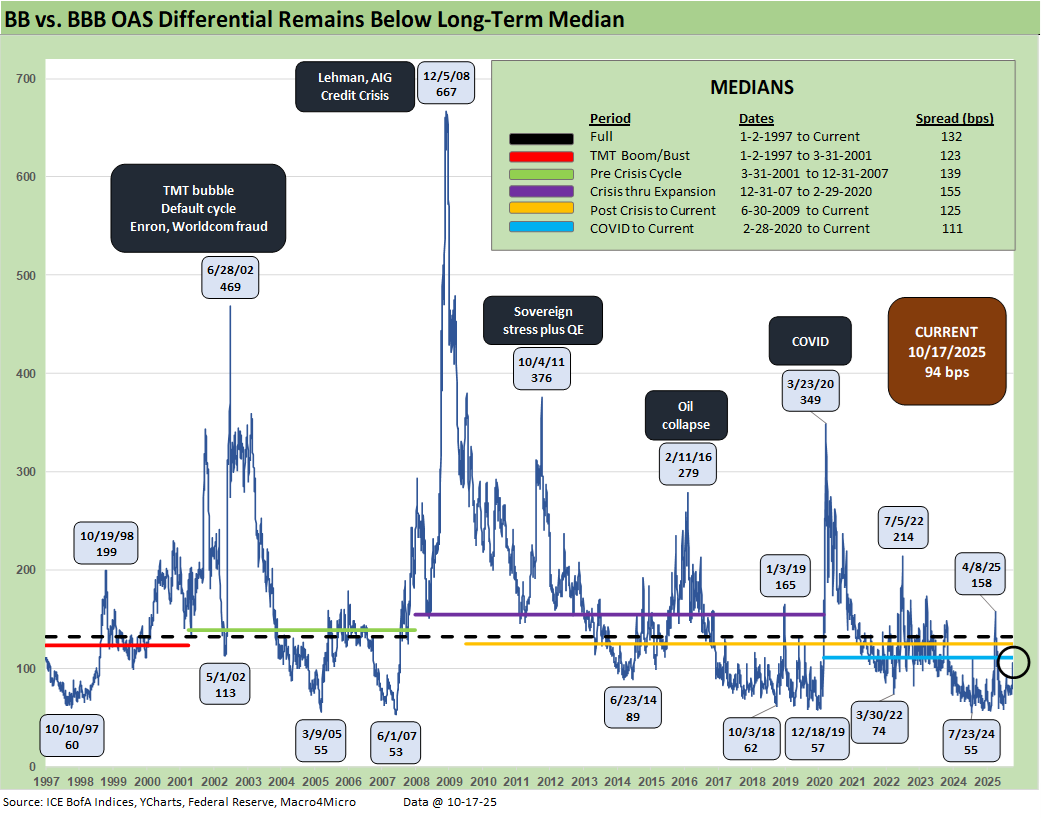

The “BB OAS minus BBB OAS” quality spread differential pushed lower by -11 bps to +94 bps on the week, or well inside the post-Liberation Day spike to +158 bps. The long-term median of +132 bps is consistent with the medians across the credit cycles detailed in the box.

The current cycle has routinely hit “lower lows” than the this week’s +94 bps with 50-handles seen at numerous points. The record low tick was in June 2007 at +53 bps. The market has come close to the all-time lows on numerous occasions from 2019 to 2024.

Recent Trends:

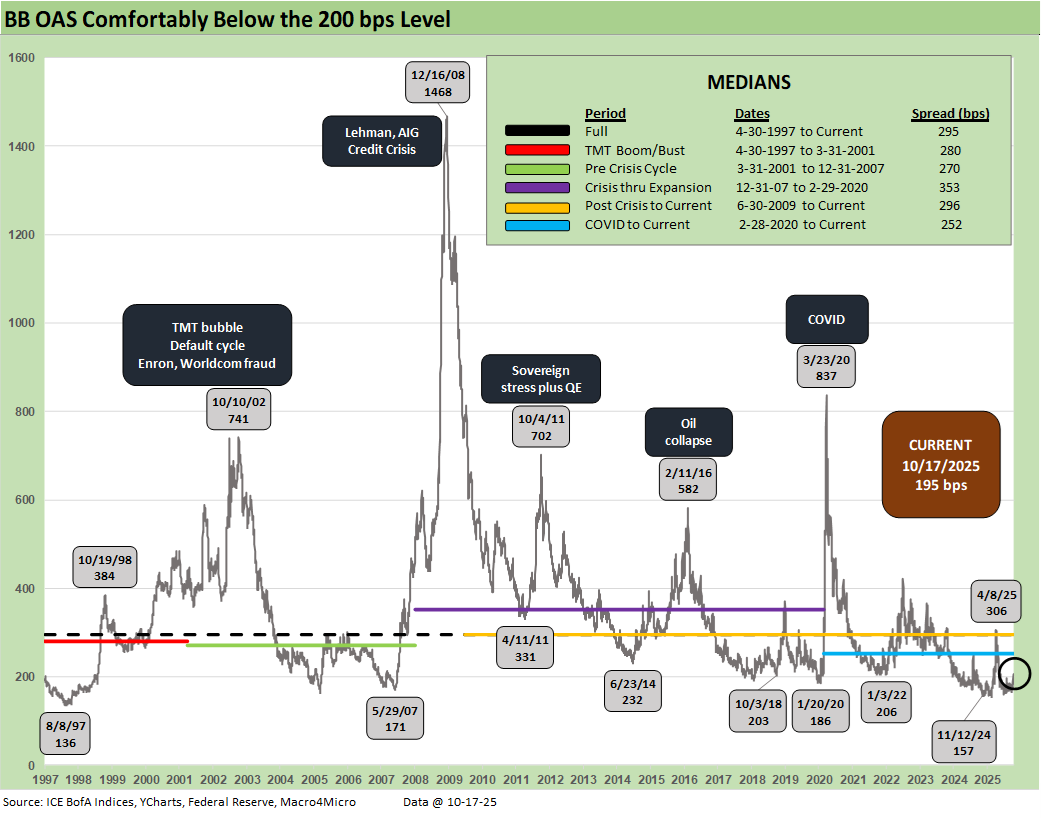

The above plots the time series for the BB tier across the cycles. The past week saw a -12 bps tightening to +195 bps. The long-term median of +295 bps remains in a different zip code.

Historical Context:

The demand for BB tier bonds has seen BBB buyers, HY lite strategies, and defensive HY funds all looking to this tier that ranks as by far the largest in HY. The strategy has worked as we covered earlier in excess and total returns across the tiers. The BB tier has been a good way to take credit risk while managing duration exposure and still carrying a respectable coupon.

Recent Trends:

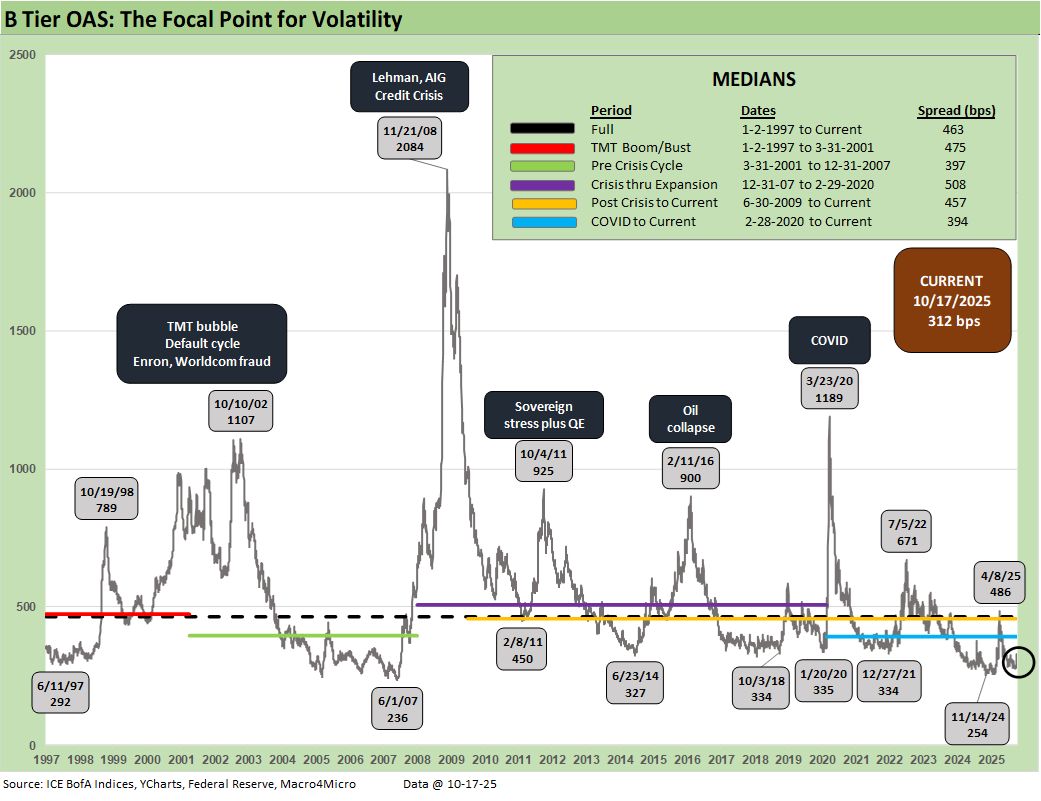

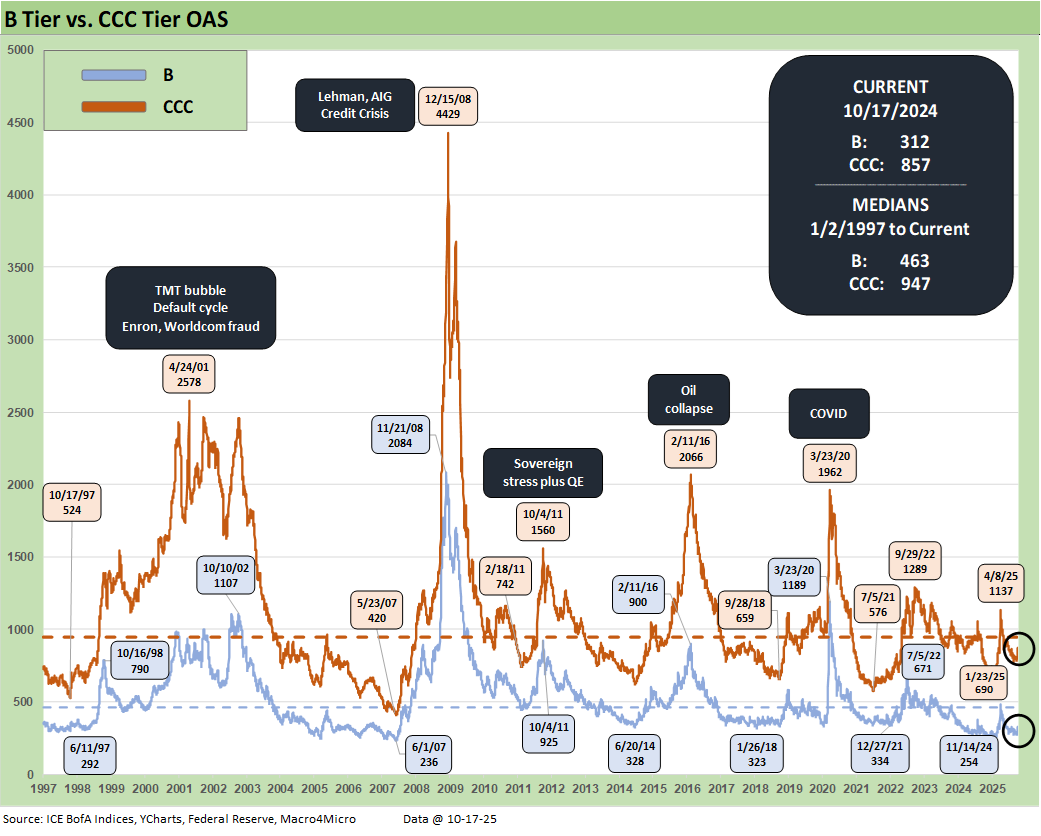

We see the current level at +312 bps, or -16 bps tighter on the week, as the B tier OAS remained outside the +300 bps line. B tier OAS had reached a post-2007 low of +254 bps in Nov 2024 before the Liberation Day fallout in April 2025 drove the B tier OAS to +486 bps. The long-term median stands at +463 bps.

Historical Context:

The B tier is the sweet spot and home of the “HY Classic” investor. This current cycle’s median at +394 bps is the lowest of the mini-cycle medians presented in the chart. It is well below the mid to high 400 handles seen in half the timelines detailed with the exception of the post-crisis (Dec 2007 to Feb 2020) median which crossed above the 500 range to +508 bps. The March 2001 to Dec 2007 (start of recession) median was just under +400 bps at +397 bps when the compression period from 1H04 to 1H07 pushed that timeline median lower.

Recent Trends:

The above time series plots the wildest ride across the cycles seen in the B and CCC OAS levels. Both credit tiers are dramatically below their long-term medians. The B tier at +312 bps is well inside the median of +463 bps while the CCC tier at +857 bps is well below the median of +947 bps.

Historical Context:

The post-crisis spread spike in Dec 2008 is ranked in a world of its own given the bundle of risks including a collapse of some market makers (and near collapse of others without Fed-engineered mergers) as well as evaporating secondary liquidity in the OTC HY bond market.

The TMT cycle default wave and secondary liquidity implosion saw multiple spread peaks in 2001 and 2002 that were especially ugly. Enron came in the fall of 2001 and WorldCom in the summer of 2002. IG spreads and BBB tier names also saw selective panic in the summer of 2002.

The sovereign panic of fall 2011 is in evidence as was the overexposure and E&P excess of 2015 to early 2016 on the collapse of oil and gas as the cash flow burn and valuation crisis dominated the upstream sector.

COVID saw a wave of supportive monetary policy and fiscal actions, so the energy sector HY crisis peak OAS in early 2016 was wider in spreads than those seen at the 3-23-20 COVID highs. In the case of the energy crisis, a major cross-section of the HY universe was driven by the same small group of risk factors in oil and gas prices and the recurring story of a collapsing borrowing base with the banks. Fear of HY fund outflows piled onto the defensive pricing.

During COVID, the return to ZIRP and the “great reopening” of the economy and markets bolstered risk appetites and generated record refinancing and extension volume. In turn, that materially reduced refinancing risk (thus default risk) and lowered coupon costs from IG to HY. Household cash flow was also boosted on mortgage refinancing to record lows.

The ZIRP backdrop also eased ABS costs and bank line costs. Under some of the Fed legislation and control moves being discussed in the current market, that support seen in earlier credit panics would not have happened. If the Fed loses such tools, that would mean the White House would pick winners and losers (i.e. friends vs. enemies).

Control of the Fed would offer the White House vastly more financial power than it has now to “influence” (intimidate? control?) borrowers and lenders alike. Such an outcome fits into any good authoritarian’s playbook (control the guns and money…one often leads to the other). Purges help.

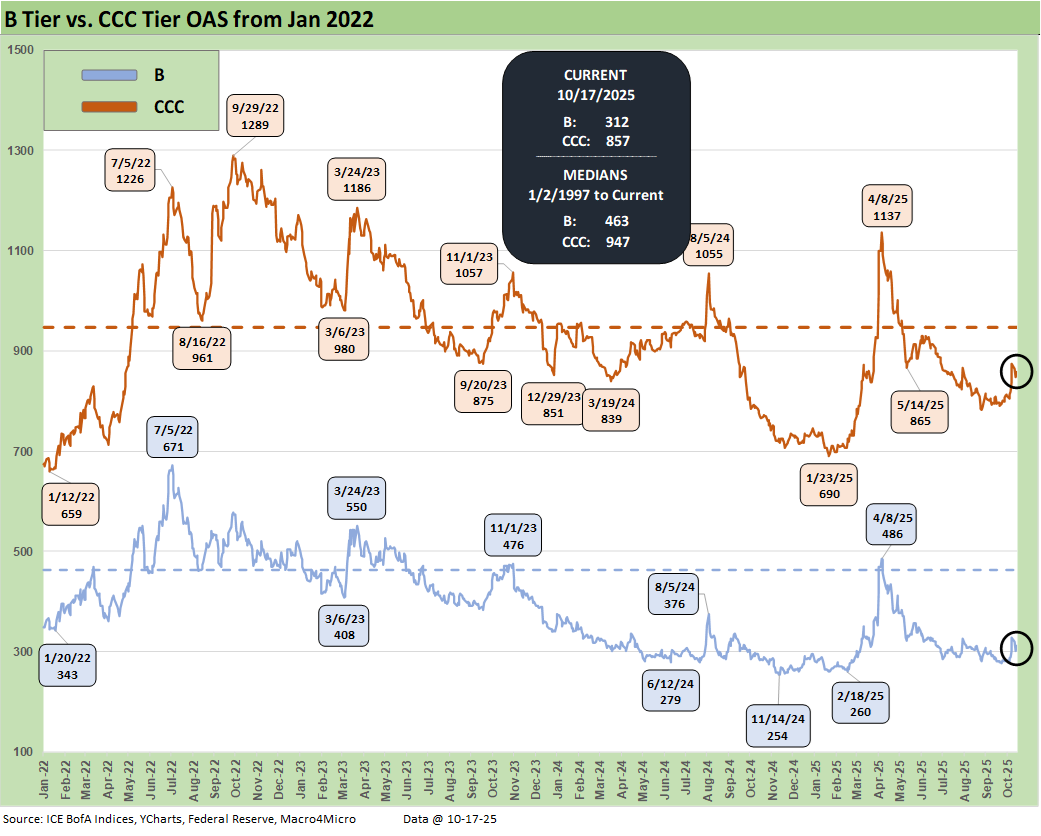

Recent Trends:

The above offers a more granular visual of the B vs. CCC OAS since the start of 2022 to get a read on how credit pricing moved across the tightening cycle on the way to easing mode.

The prior Friday’s sudden widening was a function of renewed aggression toward China trade policy (see Credit Markets: Toxic Brew? New or Old Recipe? 10-13-25). Trump tried to calm nerves on Truth Social on the following Sunday after making numerous threats to end that week. The China-US trade battle is a wait-and-see exercise again on “pauses” and extensions.

China had tweaked Trump to elicit that response on strategic metals and rare earth restrictions, but Trump has been threatening the EU and Mexico to jack up punitive tariffs on China for weeks. It is a two-way street with the consumer lying down in the middle of the road.

Historical Context:

The Russian invasion of Ukraine also rattled markets in 2022 as evident in the above chart. The resulting dislocation in energy markets was a major contributor to inflation that seldom gets mentioned in the political arena or by more partisan economists. Oil and gas prices were also major factors in the mix of 1973-1975 and 1979-1981 inflationary/stagflationary periods.

In the end, there was no recession in 2022 and no ugly default wave. Inflation came down quickly from the June 2022 peak. CCC spreads peaked in Sept 2022 as seen in the chart above as did B tier spreads in early July 2022. The inflation pain of 2022 too often gets cited without proper context around what is being “repaired” (or not repaired) in 2025 in the context of inflation.

Many of the talking heads have selective memories and seem to forget that headline CPI was 2.9% in Dec 2024. Despite claims, Trump has not driven inflation down since taking office. Too often the political rhetoric frames current inflation against the 2022 peak rather than the end of 2024. What Trump has done is create new contingent concerns around inflation from tariffs as well as disturbing supply and demand balances in key goods. China’s wide range of imports from high to low value is where you do not want to see more supply-demand imbalances.

Progress in 2025 through August on CPI has been essentially nonexistent to this point. The noisemakers should ask themselves how inflation went so high by June 2022 and then came down so quickly. That is a natural extension of pondering where it goes from here – and why.

The supply-demand imbalances of 2021 should have been on the Fed’s radar screen and a bigger priority at that time. That said, the absence of discussion of Russia and oil/gas impacts on inflation smack of selective performance attribution and is both misleading and intellectually dishonest. We are hearing plenty of intellectual dishonesty out of the White House on economic indicators, whether inflation or GDP growth (see The Curve: My Kingdom for 10 Cuts 10-19-25, The Curve: Macho Man Meets Patient Man 10-12-25).

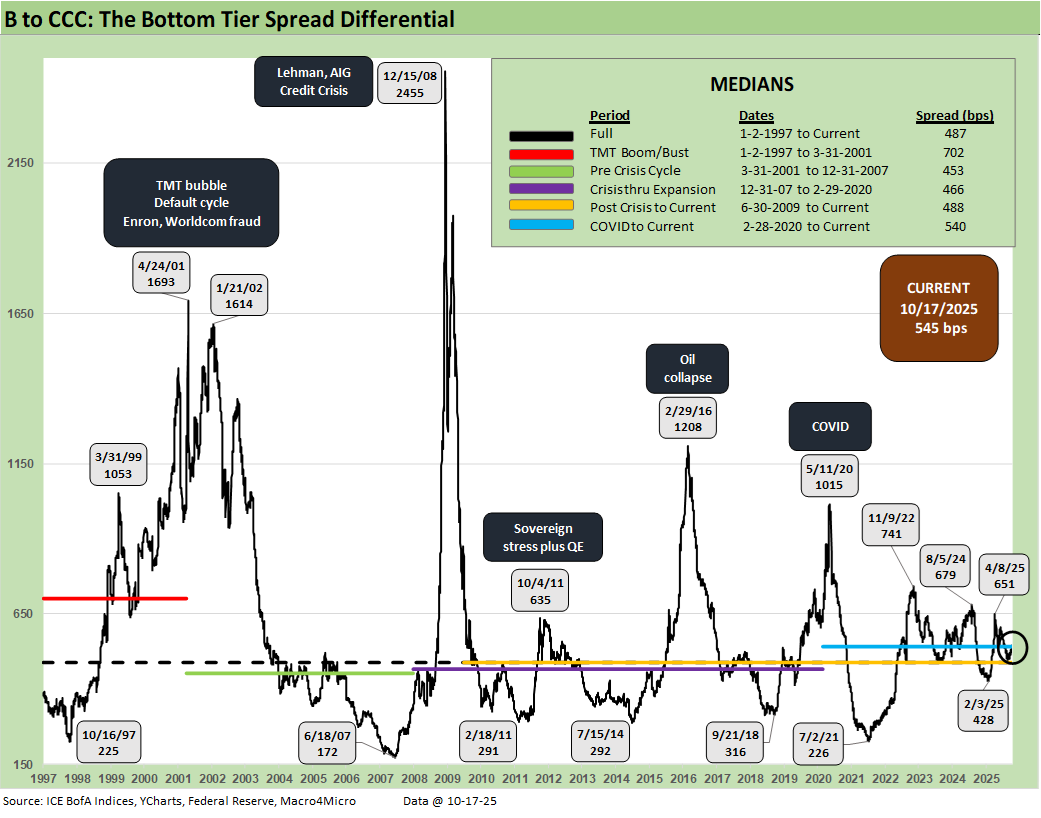

Recent Trends:

The quality spread differential between the B and CCC tier was essentially flat on the week tightening -1 bps to +545 bps with CCCs and Bs moving tighter by -17 bps and -16 bps, respectively.

Historical Context:

The above quality spread differential for B vs. CCC tells a simple story. In times of macro stress, HY secondary liquidity panics (fear of fund redemption waves, etc.) and quality shocks where the HY index has industry concentrations (e.g. TMT, Energy), the CCC tier quickly sees credit risk turn into the equivalent of equity risk and even high-risk equities. That means bond pricing is expected to offer returns commensurate with that status. That is when the action is about dollar prices and not spreads.

Trying to gauge the credit risk, the default risk, the loss-given-default pricing component, the secondary liquidity penalty, the structural risks of the governing documents, and the recovery value and time horizon risks (30 days on CDS vs. post workout value upon emergence, etc.) is where the distressed debt commandos and seasoned vets come in.

The quantitative modeling of defaults can sometimes take on the nature of “weird science” or “fake science” while the classic distressed investor typically has the experience and legal inputs to navigate such markets. Assumptions can always be wrong, but there are histories and templates that those players tap into.

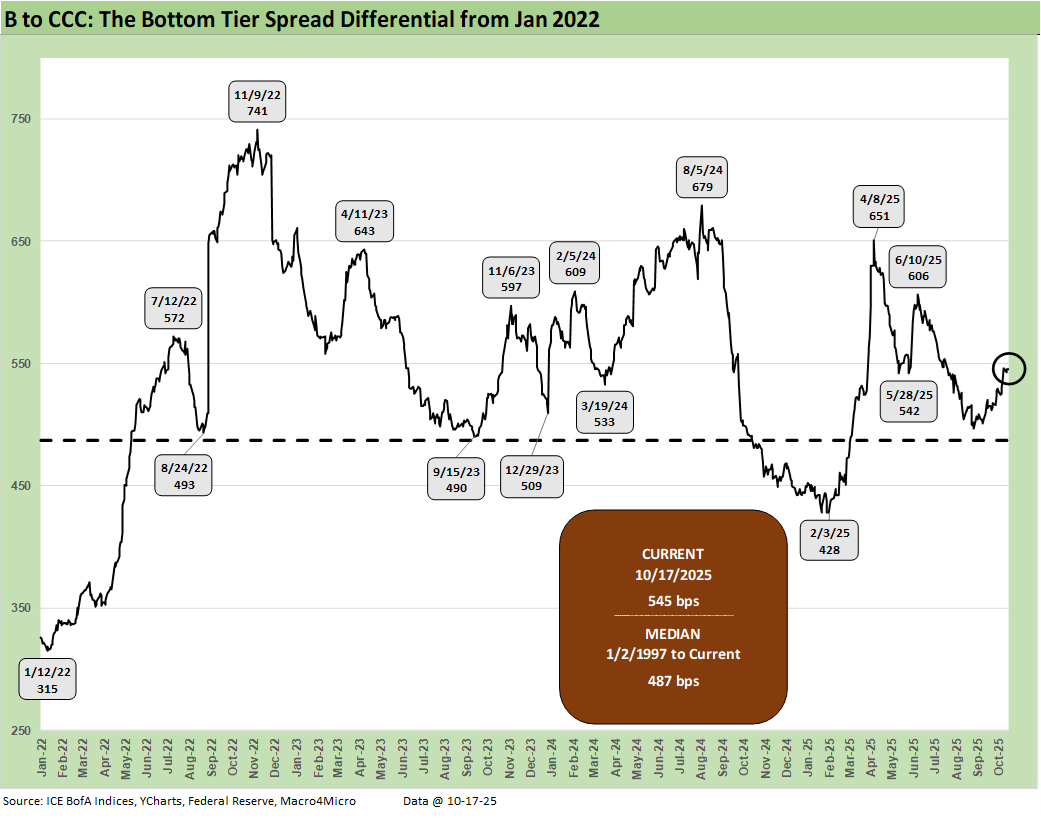

Recent Trends:

The above chart just shortens up the time horizon for the B vs. CCC quality spread differential history for the period from Jan 2022 through current times to capture the tightening cycle, the start of easing, and the new world of tariffs.

We see peak quality spread differentials at +741 bps in Nov 2022, up from +315 bps at Jan 2022. We are currently at +545 bps, above the long-term median of +487 bps. As a reminder, many market watchers were screaming recession in the fall of 2022. We did not see it that way (see Unemployment, Recessions, and the Potter Stewart Rule 10-7-22).

What NBER might dub a recession is always a “jump ball” and comes at a major lag (see Business Cycles: The Recession Dating Game 10-10-22). From our standpoint, that would require negative payroll and sustained weakness in Personal Consumption Expenditures. That is not off the table over the next 6 months, but we are not there yet. However, there is a growing chorus that the market is heading in that direction.

Cyclical turning points? 2022 vs. today…

In the current market and the recession debate, we see a mixed picture. The fall of 2022 lacked serious payroll pressures, and we are seeing those now. We will see if that data flow gets choked off in the shutdown or radically reduced via a Project 2025 hit squad.

The shutdown brings worries that Vought (OMB head and Project 2025 architect) will use the shutdown to overhaul all of the data resources. That will impair economic visibility and the ability to frame risks and Fed policy. The past two weeks brought back the risk of a China trade war, which is part of a radically different set of risks in tariffs that was not in the picture back in 2022.

There was plenty to worry about back in 2022 and Russia-Ukraine was not helping on the front of cyclical optimism with an energy price spike. However, consumer spending was still solid, and employment was strong. The yield curve was of course a mess. That said, it takes a lot to cause a recession.

PCE and consumer spending was rolling along impressively in the fall of 2022. That has been under pressure in 2025 with PCE lines in the GDP account weak in 1Q25 and 2Q25 even after the sharp upward revision in the final estimate for 2Q25 (see 2Q25 GDP Final Estimate: Big Upward Revision 9-25-25). We are seeing some decent retail sales numbers along the way, and the latest PCE release on income and outlays was more constructive on consumer outlays (see PCE August 2025: Very Slow Fuse 9-26-25). Unfortunately, GDP releases, PCE, and Income & Outlays data has been sidelined during the shutdown.

Tariffs and inflation…

PCE inflation numbers remain well above target while CPI posted some warm numbers for August, but PPI offered some offsets (see CPI August 2025: Slow Burn or Fleeting Adjustment? 9-11-25, PPI Aug 2025: For my next trick… 9-10-25). We will not get updates for September CPI until Oct 24 this week, and we have seen no commentary on any PCE price index releases at this point. The CPI was more critical to deliver on COLA for Social Security payments, so the BLS will get that Sept number done.

After the tariff legal decision on IEEPA in November, we believe economic turmoil could ease if that Appeals Court decision can hold up against the SCOTUS “friends of Trump” (see Macro Menu: There is More Than “Recession” to Consider 8-5-25). The market could not handle a China trade war as a much larger problem.

If SCOTUS rules against Trump in the IEEPA case, he would lose some of his easiest, readily available weapons in trade talks – especially with China. The loss of IEEPA would also (in theory) reduce Trump leverage over the EU, Canada and Mexico in the home stretch on trade terms. The White House will of course deny that and try more triple-digit tariff threats regardless. The USMCA is up for review in 2026, so the anxiety will be part of the landscape one way or another.

The 3Q25 earnings season and guidance priorities…

Last but not least, we saw solid earnings trends coming out of 2Q25 with constructive guidance. The 3Q25 earnings season has now started as the mix of factors and the advancing stage of tariff effects get more weight. We also just saw a fresh wave of tariffs to be phased in and even more in the queue and expect to get fresh color on these tariffs and associated cost mitigation strategies in earnings call Q&A.

The questions around capex planning for 2026 will be interesting to the extent they even get answered this early. That might be a 4Q25 earnings guidance discussion. For those most exposed to tariffs and global sourcing, the IEEPA decision is critical. That will not be available except for (maybe) the late earnings reports. That decision will be available for the later reporting season for retailers. The BDC earnings reports are concentrated in the first week of November, and those have taken on new significance with the two meltdowns (First Brands, Tricolor).

Recession debate still gets our “no” vote for 4Q25…

For now, the recession risk handicapping is a pitched battle. The mix of variables are worse in the fall of 2025 than 2022 with the exception of inflation (lower now). Short interest rates are lower now and heading lower. Jobs and consumer spending and corporate sector reinvestment and hiring are the main events, and labor will remain a weak part of the cyclical story. Consumer spending in the PCE lines of GDP is weaker now than in 2022 (and 2024) as is the employment picture. The small business sector is also weaker now on tariffs.

All in, risk premiums in credit are low, multiples are very high in equities, and the market is relying on Washington to not blow it all up. So far, we have avoided fully unhinged trade wars in the “age of Trump tariffs” except a very brief and ugly one with China, who is again will be the main worry in coming days.

Presumably, the shutdown will not do too much damage, or the market will need to react. The signs are not good on the shutdown, but we could see odds of a deal improving once all the “mail gets opened” on health insurance premiums and voters are outraged. If the shutdown brings a mass overhaul of economic data releases (BLS and BEA), then the market will know that there is serious trouble ahead for Fed independence.

See also:

The Curve: My Kingdom for 10 Cuts 10-19-25

Market Commentary: Asset Returns 10-19-25

Mini Market Lookback: Healthy Banks, Mixed Economy, Poor Governance 10-18-25

Credit Markets: Toxic Brew? New or Old Recipe? 10-13-25

Mini Market Lookback: Event Risk Revisited 10-11-25

Credit Profile: General Motors and GM Financial 10-9-25

Credit Markets: The Void Begins 10-6-25

The Curve: Blind Man’s Bluff 10-5-25

Mini Market Lookback: Chess? Checkers? Set the game table on fire? 10-4-25

JOLTS Aug 2025: Tough math when “total unemployed > job openings” 9-30-25

Credit Markets: Cone of Silence Ahead? 9-29-25

Mini Market Lookback: Market Compartmentalization, Political Chaos 9-27-25

PCE August 2025: Very Slow Fuse 9-26-25

Durable Goods Aug 2025: Core Demand Stays Steady 9-25-25

2Q25 GDP Final Estimate: Big Upward Revision 9-25-25

New Homes Sales Aug 2025: Surprise Bounce, Revisions Ahead? 9-25-25

Credit Markets: IG Spreads Back in the Clinton Zone 9-22-25

Mini Market Lookback: Easy Street 9-20-25

FOMC: Curve Scenarios Take Wing, Steepen for Now 9-17-25

Home Starts August 2025: Bad News for Starts 9-17-25

Industrial Production Aug 2025: Capacity Utilization 9-16-25

Retail Sales Aug 2025: Resilience with Fraying Edges 9-16-25

Credit Markets: Quality Spread Compression Continues 9-14-25

Mini Market Lookback: Ugly Week in America, Mild in Markets 9-13-25

CPI August 2025: Slow Burn or Fleeting Adjustment? 9-11-25

PPI Aug 2025: For my next trick… 9-10-25

Mini Market Lookback: Job Trends Worst Since COVID 9-6-25

|

|