1Q25 GDP Advance Estimate: Roll Your Own Distortions

The 1Q25 GDP numbers have some notable anomalies that work both in favor and against the headline number.

No growth, no cry…

For the rolling 3 months, the bulls can tailor some mitigating factors such as a distorted trade deficit to weave into the drop to -0.3%. The bears can back out some inventory excess and inflated pre-buying in GPDI. The key is to lock in on what can roll into 3Q25 action as inventory gets liquidated, tariff-driven price increases impact PCE, and the trade deficit gets whipsawed by all the tariff effects.

The two distortions you always need to look at each quarter are the trade deficit and the private inventory investment. For 1Q25, the pre-buying drove a -4.83% deduction from GDP while the change in private inventories tacked on +2.25%. Those two could allow one to add back 2.6% net (if you are axed). There could in theory be some big reversals in both of those in 3Q25.

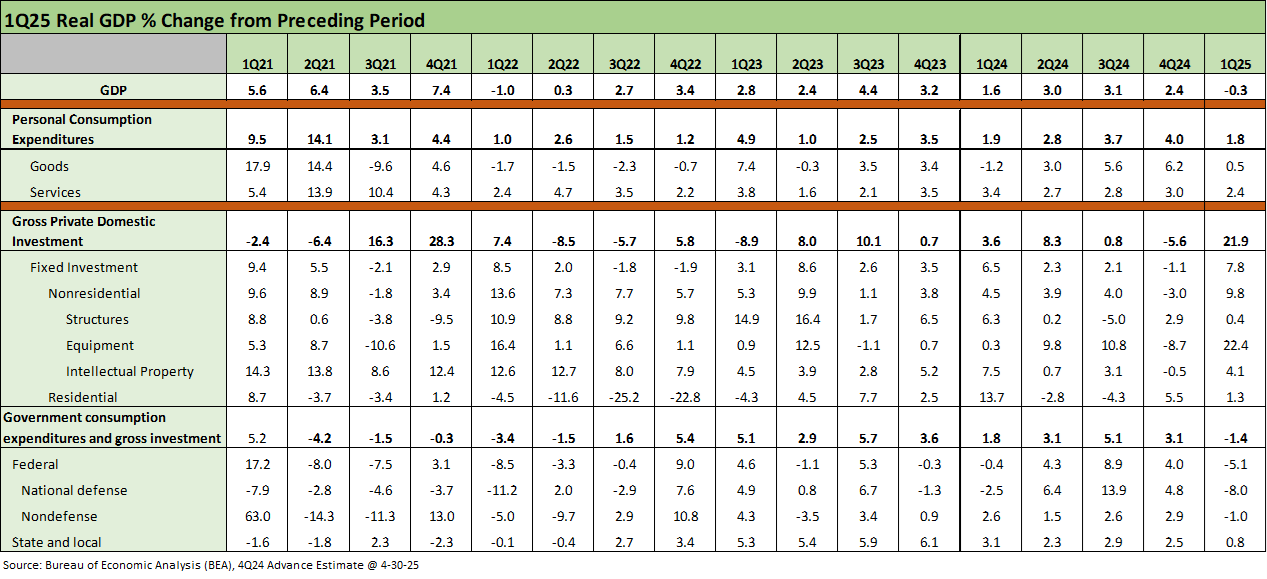

PCE growth of +1.8% was a major sequential drop from 4Q24 (+4.0%) and 3Q24 (+3.7%). Goods dove to +0.5% from +6.2% in 4Q24 with Durables at -3.4%. The Services line was modestly lower at +2.4% from +3.0% in 4Q24. The PCE price index for the quarter was +3.6%, which is a bad number for the stagflation story line. March PCE was released later and tempered that number. We cover this separately.

The Equipment growth line of Gross Private Domestic Investment (GPDI) went off the charts at +22.5% (that number needs some peeling back) on what is likely many of the same catalysts of accumulating ahead of trade war escalation. The GPDI number was +21.9% with Nonresidential at +9.8% under that broader umbrella.

Government weighed in at -1.4% with Federal at -5.1% with Defense at -8.0% and Nondefense -1.0% driving that number. State and Local slid to +0.8% from +2.5%.

The above table breaks out the line items across the PCE and GPDI lines. The 21.9% looks strange but we saw similar magnitudes back in 3Q21 and 4Q21. The Fixed Investment lines can whip around as we have seen often in the past and notably on the way into downturns. The Residential line was positive in 1Q25 and that is one that historically can move very quickly and in “size.” Mortgage rates and jobs are the critical drivers there.

We will do our usual drill-down into the Nonresidential subcategories in a separate piece later today. Based on our preliminary review of that data, there was a lot of action in the “Information Processing Equipment” bucket, which would be logical given the tension with Asia on tariffs and discussions of semiconductors being a Section 232 candidate or a unilateral tariff even outside Section 232. Trump has a collection of legacy legislation to do whatever he wants. It is all legal even if the legislative intent gets stretched to the limits.

Government consumption and investment is going in the direction that has been promised by Team Trump – as in smaller Federal. The “path to smaller” and the report card on execution turns instantly subjective and political. It remains to be seen how pulling the plug on grants and cutting heads on such a scale and so quickly will translate into multiplier effects in the broader industry mix outside “government investment” (notably in health care industries and biotech). That is a separate topic.

See also:

JOLTS Mar 2025: No News is Good News 4-29-25

Tariffs: Amazon and Canada Add to the Drama 4-29-25

Credit Snapshot: D.R. Horton (DHI) 4-28-25

Footnotes & Flashbacks: State of Yields 4-27-25

Footnotes & Flashbacks: Asset Returns 4-27-25

Mini Market Lookback: Earnings Season Painkiller 4-26-25

Existing Home Sales March 2025: Inventory and Prices Higher, Sales Lower 4-24-25

Durable Goods March 2025: Boeing Masking Some Mixed Results 4-24-25

Equipment Rentals: Pocket of Optimism? 4-24-25

Credit Snapshot: Herc Holdings (HRI) 4-23-25

New Home Sales March 2025: A Good News Sighting? 4-23-25

Footnotes & Flashbacks: Credit Markets 4-21-25

Footnotes & Flashbacks: State of Yields 4-20-25

Footnotes & Flashbacks: Asset Returns 4-20-25

Mini Market Lookback: The Powell Factor 4-19-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Home Starts Mar 2025: Weak Single Family Numbers 4-17-25

Credit Snapshot: Service Corp International (SCI) 4-16-25

Retail Sales Mar25: Last Hurrah? 4-16-25

Industrial Production Mar 2025: Capacity Utilization, Pregame 4-16-25

Credit Snapshot: Iron Mountain (IRM) 4-14-25

Mini Market Lookback: Trade’s Big Bang 4-12-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

CPI March 2025: Fodder for Spin 4-10-25

Credit Snapshot: Avis Budget Group (CAR) 4-9-25

Payroll March 2025: Last Call for Good News? 4-4-25

Payrolls Mar 2025: Into the Weeds 4-4-25