Mini Market Lookback: FOMC Spoke Clearly, Iran and Trump up next 6-21-25

Fed funds did not surprise but FOMC forecasts were unkind. The focus is back on “What’s next for the US in the Middle East and when?”

Those chips are not weeks. The game is not risk-free.

Asset moves this past week were very mild in the credit markets with flat spreads on IG and a minimal compression of -5 bps in HY. The broad market equity benchmarks saw 3 positive (NASDAQ, Russell 2000, MidCap 400) and 1 negative (S&P 500). The Dow was flat.

The FOMC and dot plot and Summary of Economic Projections (aka “SEP”) stung. Upward revisions in forecasted medians for PCE inflation and Core PCE continue the upward trends seen in March from Dec. The 3.9% median fed funds forecast for 2 cuts in 2025 remained unchanged and flat to March 2025 and Dec 2024. The challenge this time on the 3.9% median was that the number of dots in the gang of 19 that saw “no change” in 2025 moved higher from 4 to 7.

We saw another round of downward revisions from the Fed for GDP growth in 2025, 2026 and 2027 with across-the-board sub-2% projected growth. That includes only 1.4% for 2025. Important economic releases during the week included Retail Sales, Industrial production, and Home Starts, and those came in modestly negative overall (see Home Starts May 2025: The Fade Continues 6-18-25, May 2025 Industrial Production: Motor Vehicle Cushion? 6-17-25, Retail Sales May 25: Demand Sugar Crash 6-17-25).

The Iran bombing handicapping and related price action was muted with Trump’s oft-heard “2-weeks” timeline. Trump used the words “unconditional surrender” in imprudent fashion and delivered early and often. The unsurprising sense of machismo seemed to ignore the fact that the main “condition” is in fact quite clear – elimination or complete cessation of the nuclear program. The connotations of “unconditional” could arm Iran’s leadership in gaining support on the domestic front. It’s an extreme opener when time is short.

The unconditional surrender gambit…

The old unconditional playbook (see Casablanca Conference 1943) is rare for a reason. Nazis and Japan fascists started the war, so the US had rational reasons to use “unconditional surrender” in WWII. In 2025, that is really not the case. In 1943, there was a goal to reassure the Soviet Union so they did not bail out as they did in WWI. Other theories included reassuring China to keep tying up Japanese troops in the wide expanse of China as Japan faced both Chiang Kai-shek and Mao with their respective armies (theories vary materially on who gave less than full effort).

In the case of this current use of “unconditional surrender”, there are plenty of other conditions and trade-offs that will also undermine popular Iranian support for the radical leaders without the US making the “all or nothing” opening gambit. That is especially the problem, when “all” is not defined.

It is easier to play armchair geopolitics along the ride, but the checklist of trade-offs start with “all nukes must go immediately with 100% solid verification rules.” From there, the process has a lot of room to trade after that demand with sanctions lifted and oil sales freed up as long as state sponsorship of terrorism and the history of “war proxies” ends. There is much up for grabs if done the right way. But nukes rank #1, #2 and #3. Most believe (esp. MAGA) that the US is out of the regime change business.

The credit market OAS delta for 1-week and 1-month are broken out above, and aggregate Index OAS trends have been favorable and steady with the exception of the more volatile CCC tier looking back 1-month. The HY OAS of +313 bps is just -3 bps under the early 2018 cyclical lows (+316 bps) and below the June 2014 low levels of +335 bps. As a reminder, Jan 2020 hit +338 bps and Dec 2021 +301 bps while Jan 2025 plunged all the way down to June 2007 type levels at +259 bps (see Footnotes & Flashbacks: Credit Markets 6-16-25).

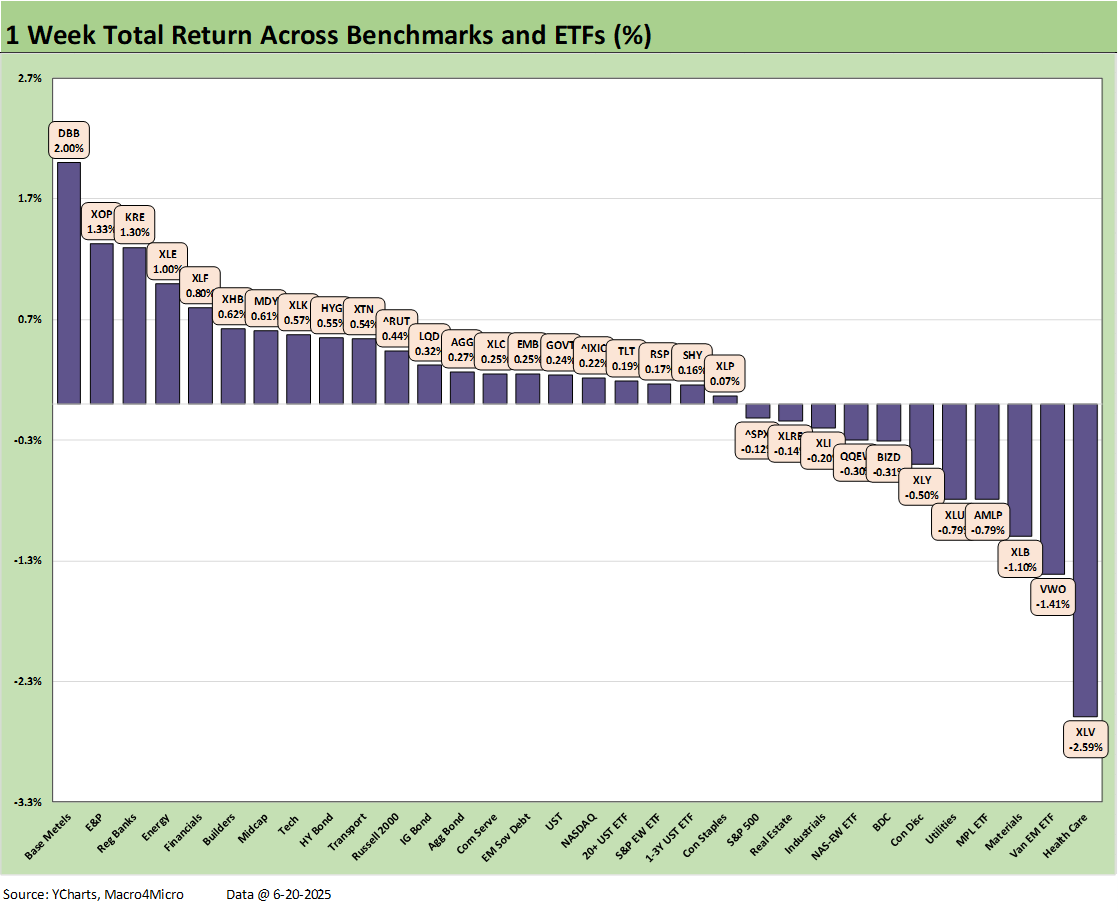

The relatively uneventful 1-week returns for the 32 broad benchmarks and ETFs we watch weighed in a healthy 21-11 with all 7 bond ETFs in positive range. We see only 4 of 32 beating +1.0% while it only took -0.3% to make the bottom quartile. The Hi-Lo range was only 4.59 points, down from over 10.8 points last week with its 15-17 score. Right now, the market seems to be saying “call me when Iran impairs shipping on the Strait of Hormuz” or “let me know when the bunkers get busted (or the US fails trying).”

Failure of a dramatic, nuke-site bombing decision is the Trump nightmare. His base might not be too happy either, which in turn leads to higher forms of destabilization in the White House and raises the risk of “overcompensation” (a polite term) in domestic policy actions to please the MAGA hard core (escalate in LA, Chicago, New York and go after the next tier of blue state cities and maybe another dozen “elitist” colleges).

Trump’s temporary and reversed ICE plan to spare farms, hotels and many retail employers could return and his “war on blue” could get uglier. That would take a toll on inflation and exacerbate imbalances and cause freight and logistics problems if it gets too out of control. LA’s protests are mild in the context of the 60s. LA was mild as a protest, property damage, and zero deaths. Jan 6 was much worse. Memories of 1967 (Detroit, Newark) and 1968 (Baltimore, Boston) and LA experiences in 1965 (Watts) and 1992 LA.

It is clear that Trump’s policy actions were not grading on the danger curve and were used as a means to practice his mass immigration plan and road test his authoritarian options to get by a stacked SCOTUS. US political risk will be seen in a negative light internationally. At some point, offshore investors will balk, the dollar will be a worry, and the UST yields and slope might need to adjust to clear record supply. Earnings and stock valuation multiples will not be happy. Duration will be a concern. The stagflation risk will stay hot in the debate.

Health Care (XLV) brought up the rear this past week as the market braced for EU clarity on reciprocal tariffs with a Section 232 process also in the queue for pharma, which is the largest import from Europe into the US. The bottom quartile included a diverse mix across Equal Weighted NASDAQ 100 ETF (QQEW), Consumer Discretionary (XLY), and BDCs (BIZD) with floating rate exposure and a high mix of small-to-mid private sector businesses. The high-dividend Midstream Energy ETF (AMLP) and Utilities (XLU) posted moderately negative numbers for the week. Cyclical Materials (XLB) and EM equities (VWO) rounded out the bottom tier.

DBB (base metals) came in as a winner at 2.0% with E&P (XOP) and Energy (XLE) making the top 5 with Regional Banks (KRE) and Financials (XLF)

We line up the tech bellwethers above in descending order of returns for the week. Tech limped through the week as mixed headlines with US-EU non-tariff discussions were rumored to be making headway (those tend to target tech). EU has raised targeting services as a defense against Trump trade war risks.

The FOMC news was net negative for some with easing still a mixed picture but helpful for some bellwethers. The rising consumer worries and lower GDP growth will be a headwind for Alphabet, Amazon, and Tesla on the bottom. For the Mag 7, the week posted 3 positive, 1 at zero, and 3 negative.

The weakness in growth and daunting tariff pipeline threats will flow into IT budgets for some and especially small businesses with the least budget flexibility. The Section 232 tariff lineup of pharma, semis, commercial aircraft/parts, copper, and lumber in addition to the final reciprocals (when they ever get released) and potential trade partner retaliation will strain purchasing managers and capital budget planning. Most of that lies ahead and some tariffs just started. The pro-tariff crowd plays with the trailing numbers, but the job is to be forward-looking – even if just into the fall. All the PCE inflation forecasts from the Fed this week are going away from the 2.0% target.

The 1-week US delta chart above translates into a mild bull steepening on the week even with the more guarded Fed report on the direction of inflation and economic growth (see FOMC Day: PCE Outlook Negative, GDP Expectations Grim 6-18-25).

The YTD UST deltas remain in a variation of the bull steepener YTD with the 30Y breaking ranks and moving higher YTD. That steepener risk and its ties to the Japan story line and bearish currency moves are not helping duration risk appetites. Those themes will remain on the front burner as the budget gets finished and numbers more ingrained in investors’ minds outside the usual disinformation efforts of tax bill supporters. The Fed, the OECD, and World Bank all took some of the steam out of the White House and GOP leadership complaints about CBO growth assumptions.

The CBO has rendered some hard verdicts on the direction of the deficits that keep getting reworked in the headlines as the Big Beautiful Bill terms keep moving. The easy takeaway is “good for high income taxpayers and corporations” and “bad for Medicaid dependent states and households/consumers.”

The separate topic of tariffs (aka “border taxes”) is what is bad for many corporations, small businesses and consumers. Just try to get Trump, Bessent, or Lutnick or leaders of key committees (e.g. GOP head of House Ways and Means) to admit the buyer writes the check to customs. They say the opposite and are now somewhat caught in that Trump “seller pays” fantasy. That the buyer pays the tariff is an explicit fact.

Then the analysis is about who bore that cost that the buyer pays from the seller to the end customers. Did the seller cut price? Does the buyer eat it? Does he pass it on? “Who pays the tariff” is reframed by the economist PhD wordsmiths who like playing with the question to change it into the question that they want to answer. Intellectually, it is slimy, but those are the rules of engagement in partisan policy advocacy (“You lie, I’ll swear to it!”) They have embraced the playbook that “it is better to be loud and repetitive than factually correct.”

The above chart plots the Freddie Mac 30Y mortgage benchmark vs. the 10Y UST. The mortgage rates remain stubbornly high, and the 10Y UST remains well above the Sept 2024 lows as we cover each week in our Footnotes publication on the State of Yields (see Footnotes & Flashbacks: State of Yields 6-15-25). The updated version will be posted later this weekend.

The housing markets are still in a steady fade as we heard from Lennar (one of the Big 2 homebuilders) this week (see Lennar 2Q25: Bellwether Blues 6-20-25). The broader home starts data also highlights the relative weakness of the spring selling season (see Home Starts May 2025: The Fade Continues 6-18-25).

HY spreads tightened -5 bps to +225 bps with the BB tier flat, the B tier -8 bps tighter and CCCs -13 bps tighter. We discussed the historical context vs. past credit market peaks at the top of this note. Current spreads are slightly under (by -3 bps) the early Oct 2018 lows.

HY-IG quality spread differential tightened by -5 bps to +225 bps this week on -5 bps tighter HY and flat for IG on the week.

“BB OAS minus BBB OAS” quality spread differentials were flat at +72 bps on the week with both the BBB tier and BB unchanged.

See also:

Lennar 2Q25: Bellwether Blues 6-20-25

FOMC Day: PCE Outlook Negative, GDP Expectations Grim 6-18-25

Home Starts May 2025: The Fade Continues 6-18-25

May 2025 Industrial Production: Motor Vehicle Cushion? 6-17-25

Retail Sales May 25: Demand Sugar Crash 6-17-25

Footnotes & Flashbacks: Credit Markets 6-16-25

Footnotes & Flashbacks: State of Yields 6-15-25

Footnotes & Flashbacks: Asset Returns 6-15-25

Mini Market Lookback: Deus Vult or Deus Nobis Auxilium 6-14-25

Credit Snapshot: Hertz Global Holdings 6-12-23

CPI May 2025: The Slow Tariff Policy Grind 6-11-25

Mini Market Lookback: Clash of the Titans 6-7-25

Payrolls May 2025: Into the Weeds 6-6-25

Employment May 2025: We’re Not There Yet 6-6-25

US Trade in Goods April 2025: Imports Be Damned 6-5-25

Past-Prologue Perspective for 2025: Memory Lane 2018 6-5-25

JOLTS April 2025: Slow Burn or Steady State? 6-3-25

Tariffs: Testing Trade Partner Mettle 6-3-25

Mini Market Lookback: Out of Tacos, Tariff Man Returns 5-31-25

PCE April 2025: Personal Income and Outlays 5-30-25

Credit Snapshot: Meritage Homes (MTH) 5-30-24

1Q25 GDP 2nd Estimate: Tariff and Courthouse Waiting Game 5-29-25

Homebuilder Rankings: Volumes, Market Caps, ASPs 5-28-25

Durable Goods Apr25: Hitting an Air Pocket 5-27-25

Mini Market Lookback: Tariff Excess N+1 5-24-25

New Home Sales April 2025: Waiting Game Does Not Help 5-23-25

Existing Home Sales April 2025: Soft but Steady 5-22-25

Credit Snapshot: Lithia Motors (LAD) 5-20-25