Tariffs are like a Box of Chocolates

We update the 1Q25 clash of equity markets across the US, Canada, and Europe for a snapshot on relative performance.

Tariffs are permanent! That’s all I have to say about that. Then again…

We will keep tracking some useful equity market benchmarks from the start of 2025 that tell a story of the great tariff fight between the US, Canada, and the EU for a gut check on how the markets see it playing out.

It is worth watching forward-looking stock valuations for how the market sees the impact on different pieces of the corporate sector and with respect to how those nations will adjust their “economic” models” to grow away from exposure to the US.

Economic releases are intrinsically backward looking, and there is a “lot of game left to play” with rolling tariffs, clarifying the numbers, and in terms of gauging retaliation severity.

Longevity is another major variable when the word “permanent” keeps getting tossed around.

As of 1Q25, the US is losing as they plan a reversal and takedown by punishing the economies of Europe and Canada. They will retaliate of course.

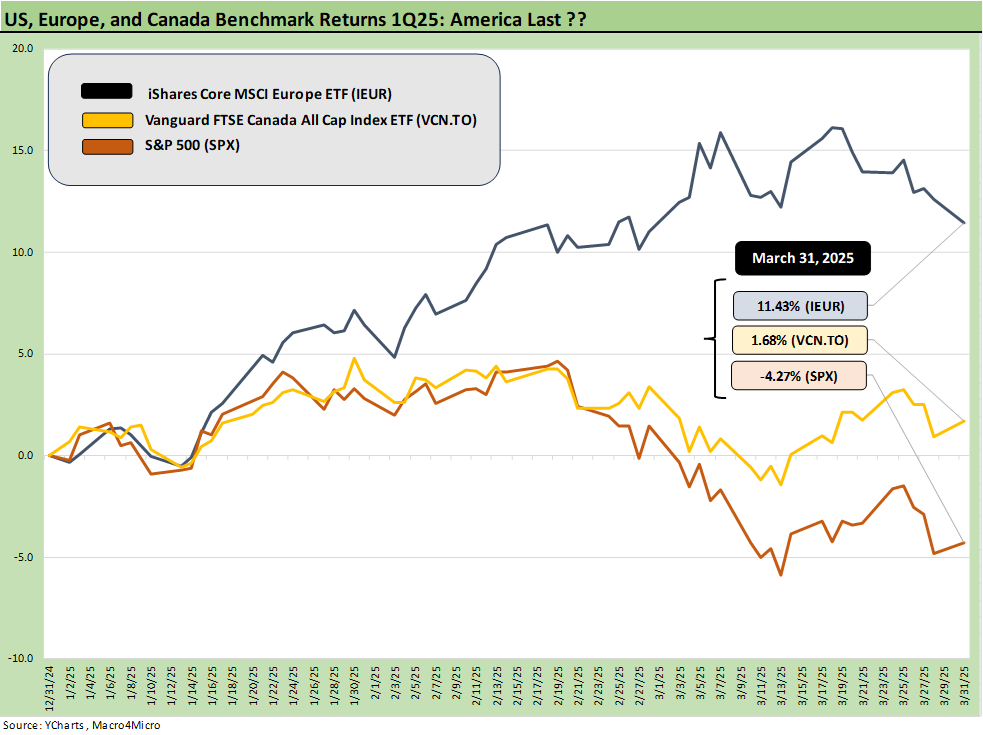

We used the above chart in a recent commentary, and we will update it along the way as the trade battles and perhaps some protracted trade wars break out. We picked ETFs for Europe and Canada that cut across sectors, industries, and market caps and frame them against the S&P 500. One can debate what the best comps might be, but it is only meant as a snapshot.

Across the 1Q25 period (3-31-25), the US is “down in the count” as the trade policies take a toll on the US and even after the S&P 500 hit an all-time high in 1Q25. In the long-ago days of Trump 1.0, the performance of the stock market was all-important. Times have changed. In the long-ago days of the campaign, lower prices were promised and were also all-important. This goes under the heading of “life is like a box of chocolates….you never know what you’re going to get.”

Some of the questions to ponder as we get into the next stage of the trade war are obvious, and some not so obvious. Trump’s Liberation Day announcement is supposedly coming after the bell tomorrow unless he changes his mind overnight. The leaks are all over the place, so we can assume the news will be played by bears as the start of a global financial wildfire and by bulls as a case of “every dip is a buying opportunity” and “this too shall pass.” As we have covered in our tariff research (see links at bottom), there are some very big differences on what tariffs might mean even if the overwhelming consensus is that prices will rise. Trump is sticking with “seller pays.”

In the stock market and sovereign financial health discussions some major questions that will haunt or help many include:

Is this the great opportunity Europe needed to invest in growth and stand on its own feet in defense. Since it will borrow heavily and spend to support intra-European industries from tech to defense, will it focus on private sector growth while using tariffs and non-tariff actions to favor the home team?

If everyone is investing and borrowing in Canada and Europe, then who will be the lenders to all the borrowers? Will competition for sovereign debt issuance undermine the UST as the safe vehicle of choice at a time of record borrowing needs?

Will explosive growth in Canada for energy exports and investment lead to more business with China and Europe that hits the US energy trade demands? Will European and China investment dollars aim at Canadian energy and punish the US for their hostile trade behavior?

Since Trump has been known to change his mind between floors on an elevator ride, does the word “permanent” on tariffs mean anything? Will that unpredictability be a deterrent to fiscal planning and long-term corporate investment economics everywhere?

We will see what tomorrow holds for the almost-final, pre-negotiation, permanent-for-now tariffs where Trump can change his mind any time he wants. Does anyone remember the days when tariffs were the constitutional duty of the Congress?

Tariff and Trade links:

Auto Tariffs: Questions to Ponder 3-28-25

Fed Gut Check, Tariff Reflux 3-22-25

Tariffs: Strange Week, Tactics Not the Point 3-15-25

Trade: Betty Ford Tariff Wing Open for Business 3-13-25

CPI Feb 2025: Relief Pitcher 3-12-25

Auto Suppliers: Trade Groups have a View, Does Washington Even Ask? 3-11-25

Tariffs: Enemies List 3-6-25

Happy War on Allies Day 3-4-25

Auto Tariffs: Japan, South Korea, and Germany Exposure 2-25-25

Mini Market Lookback: Tariffs + Geopolitics + Human Nature = Risk 2-22-25

Reciprocal Tariffs: Weird Science 2-14-25

US-EU Trade: The Final Import/Export Mix 2024 2-11-25

Aluminum and Steel Tariffs: The Target is Canada 2-10-25

US-Mexico Trade: Import/Export Mix for 2024 2-10-25

Trade Exposure: US-Canada Import/Export Mix 2024 2-7-25

US Trade with the World: Import and Export Mix 2-6-25

The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25

Tariffs: Questions to Ponder, Part 1 2-2-25

US-Canada: Tariffs Now More than a Negotiating Tactic 1-9-25

Trade: Oct 2024 Flows, Tariff Countdown 12-5-24

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariff: Target Updates – Canada 11-26-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Facts Matter: China Syndrome on Trade 9-10-24

Tariffs: Questions that Won’t Get Asked by Debate Moderators 9-10-24

The Debate: The China Deficits and Who Pays the Tariff? 6-29-24

Trade Flows: More Clarity Needed to Handicap Major Trade Risks 6-12-24

Trade Flows: Deficits, Tariffs, and China Risk 10-11-23