US-Mexico Trade: Import/Export Mix for 2024

We break out final import/export products for Mexico in 2024 as tariff uncertainty remains in the red zone.

No stinking tariffs!

We update the final US-Mexico import/export trade numbers with the top product categories for each that remind us of the scale of the stakes for both countries in terms of economic activity.

The leading import categories remind us how much of the trade is tied to labor costs but also how much of the export volume is dependent on that. In other words, hammer the imports and the exports will tank as well. That will cost both sides.

We also highlight that there are more alternatives that do not entail the sudden appearance of heavy investment in US production and reshoring and such an assumption of “all good news” on the other side of the tariff spike is flawed to the point of simplistic.

The picture at the top is from the classic Bogart film, The Treasure of the Sierra Madre. There is no treasure in high tariffs on Mexico.

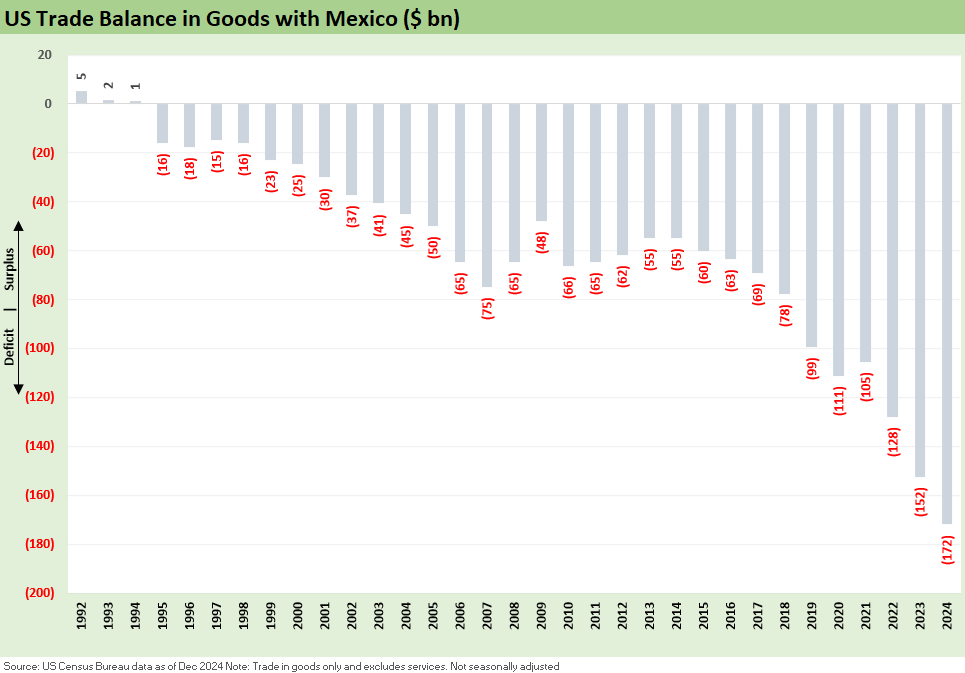

The above chart updates the economic activity between the US and Mexico for 2024. The import/export line items as laid out below will get more than a little focus if the goal is to move the top line above (imports) lower without considering what it means for the lower line (exports). Less economic activity in the chart above should be an easy forecast if we stay on the current path of proposed high tariffs.

Assuming there will be favorable multiplier effects on growth on the US side of the border by gutting the south side of the border is part of a long list of assumptions and forecasts that might be ignoring a lot of other potential outcomes. Retrenchment and cost cutting is potentially at the top of the list of options if a supplier chain shock flows into a company’s expense line.

Analysts have heard more than a few times over the decades “that was not in my model” from headline events such as the LTCM unraveling or RMBS crash. Maybe lower exports to Mexico is an obvious risk? Lower exports to Canada? Is there a chance that companies trim capex and focus on efficiency, buybacks, or debt-financed M&A?

Just admitting there is more than one potential outcome in a tariff war (or a one-sided national economic slaughter) would be a concession too far for policy advocates. “Winning the point is all” in the case of extreme economic views. Things do not always work out as planned from Lenin to Hoover, from “WIN buttons” in the stagflationary 70s to wage-price controls.

The above chart updates the final stats for the trade deficits with Mexico with a substantial amount of activity driven by US corporate sector decision making as opposed to Mexico “ripping us off.” The relocation of many manufacturing jobs can be traced to labor costs with computer assembly (#2 Mexico import) was one that unfolded “early and often” with the Auto line (#1) expanding throughout the post-NAFTA/USMCA period.

The chart hammers home the problem for US manufacturing recovery with 3 years of record US-Mexico trade deficits in the Biden years following 3 years of record US-Mexico trade deficits during Trump 1.0. Auto jobs were natural “exports” to Mexico over the decades with assembly line workers paid a fraction of US auto workers. Commodity-like components especially saw jobs sent to Mexico or China.

For a frame of reference on Mexico auto production, Mexico produced 3.86 million light vehicles in 2024 vs. 10.82 million in the US and 1.37 million in Canada (Source: Automotive News).

The ultimate questions on light vehicles go something like this (except no one in the GOP Congress will ask them with their outside voices):

· If we slap punitive tariffs on vehicles, will that just lead to less vehicles produced in North America rather than higher capex and “reshoring”? Downsizing is an option and then waiting to see where the political winds are blowing. An auto assembly plant and related supplier chain projects entail multiyear time horizons. Waiting, raising prices, paying down debt and buying back shares is an option in a free economy.

Will the OEMs just settle for less vehicles produced in North America and raise prices on favorable supply-demand imbalances like we saw in 2022? Will that supply-demand imbalance flow into used car inflation also?

Will dealers suffer on the lack of supply? Will real estate investment and waves of jobs in the auto retail sector suffer?

Will the light vehicle supply flows (some part of “round trips”) to Mexico tied to autos hurt US steel companies (e.g. the steel trade surplus with Mexico on steel broadly but higher quality auto flat rolled steel narrowly)?

Will steelmakers and suppliers raise prices domestically on the back of the Mexico tariffs shrink a key market and in turn pressure raw material costs for US manufacturers (including steel and aluminum narrowly)?

Will aluminum tariffs getting rolled in by Trump mean unit cost pressure on vehicles? Aluminum is an important commodity for “vehicle weight loss” to improve mpg performance by vehicles, so will this be one more setback in fuel efficiency? (Clearly not on the Trump priority list.)

Last but not least, will the changes in the structure of the industry and potential reshoring of assembly line locations and cost structures inevitably lead to more labor discord? Will there be wage inflation on a limited pool of workers?

There is obviously going to be a lot going on during 2025 across a range of moving parts tied to trade policy. The only forecast that is assured is that both the GOP and Democrats will both insist they are the friends of the American worker.

The above chart updates the Top 30 imports from Mexico, and there is little surprise that Autos & Light Duty Vehicles by far comprise the #1 category. We have looked at this plenty of times over the years, and the migration of jobs has always been a major point of contention from Trump to Bernie Sanders. We have looked at the Mexico tariff issues in other recent commentaries as it heated up during the election cycle (see Mexico: Tariffs as the Economic Alamo 11-26-24, Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24).

People often forget that NAFTA was a GOP initiative with very strong support from the GOP-heavy border states (ex-CA) and was signed by George HW Bush in 1992 and shepherded through Congress and eventually signed by Bill Clinton during 1993 in a bipartisan vote despite some heavy pro-union Democratic opposition. I was covering autos at the time, and the debate was not pretty.

The rise of non-union transplants accelerated and especially in right-to-work states as the politics grew more acrimonious as the years went by. One theory is that the transplant capacity will grow with the supplier chain on the US side of the border and not the UAW capacity in purple states.

Auto sector tariffs and the multiplier effects could threaten the supplier tiers (Tier 1, 2 and 3) with disruptions (components, materials, etc.) and infect OEM health and spread downstream (dealers, finance, insurance, real estate, etc.). The full chain has a lot riding on the status quo since the Mexico OEM capacity is heavily owned by the legacy Detroit 3, the Japanese OEMs (notably Nissan), and the EU OEMs (notably Volkswagen). South Korea has a much smaller presence.

The above chart details the Top 30 exports to Mexico. A lot of the line items look like a supplier chain shipped by US corporate interests to Mexico for outsourcing finished goods assembly. Trump has a history of making the problem about Mexico rather than US corporate sector purchasing decisions. In other words, it is the brown guy speaking Spanish and not the middle-aged white guy in the air-conditioned office with his collection of “lean manufacturing” books on his shelf. We always recommend The Machine that Changed the World.

The tariff actions being attempted in theory would lead to a radical downsizing of some Mexican industrial subsectors and cause material economic contraction. Those “buyers” are on the other side of the US export lines. Weakness in exports in the end will mean lower trade deficits but also materially less exports by producers in the US (just think simply of the steel or the components sent down for more assembly in Mexico). The immediate effect will be to produce less of both. That means volume pressure and weaker revenue. There are causes and effects.

The effect of less economic activity should not be ignored since that gets back to the “If A, then B, and then C, etc.” aspects of slamming Mexico. Trump is one of those decision makers who would put his hand in the flame and then find an excuse to blame the maker of the stove. So, he is not thinking that far ahead.

The wish list of a sudden appearance of new greenfield or even increased brownfield capex and supplier reshoring ignore the alternatives. Meanwhile, Canada will be unraveling at the same time as Trump’s policies are mirrored in the North. As game theory goes, this is a “trade war game” and there is an economic body count to evaluate. That does not lend itself to Washington soundbites. To make matters worse, Trumpian soundbites make Washington soundbites sound like Shakespeare.

Tariff links:

Trade Exposure: US-Canada Import/Export Mix 2024 2-7-25

US Trade with the World: Import and Export Mix 2-6-25

The Trade Picture: Facts to Respect, Topics to Ponder 2-6-25

Tariffs: Questions to Ponder, Part 1 2-2-25

US-Canada: Tariffs Now More than a Negotiating Tactic 1-9-25

Trade: Oct 2024 Flows, Tariff Countdown 12-5-24

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariff: Target Updates – Canada 11-26-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Facts Matter: China Syndrome on Trade 9-10-24

Trade Flows: More Clarity Needed to Handicap Major Trade Risks 6-12-24

Trade Flows 2023: Trade Partners, Imports/Exports, and Deficits in a Troubled World 2-10-24

Trade Flows: Deficits, Tariffs, and China Risk 10-11-23