Existing Home Sales June 2026: The Stall is On

Sustained weak existing home sales volume was accompanied by a record high median home price.

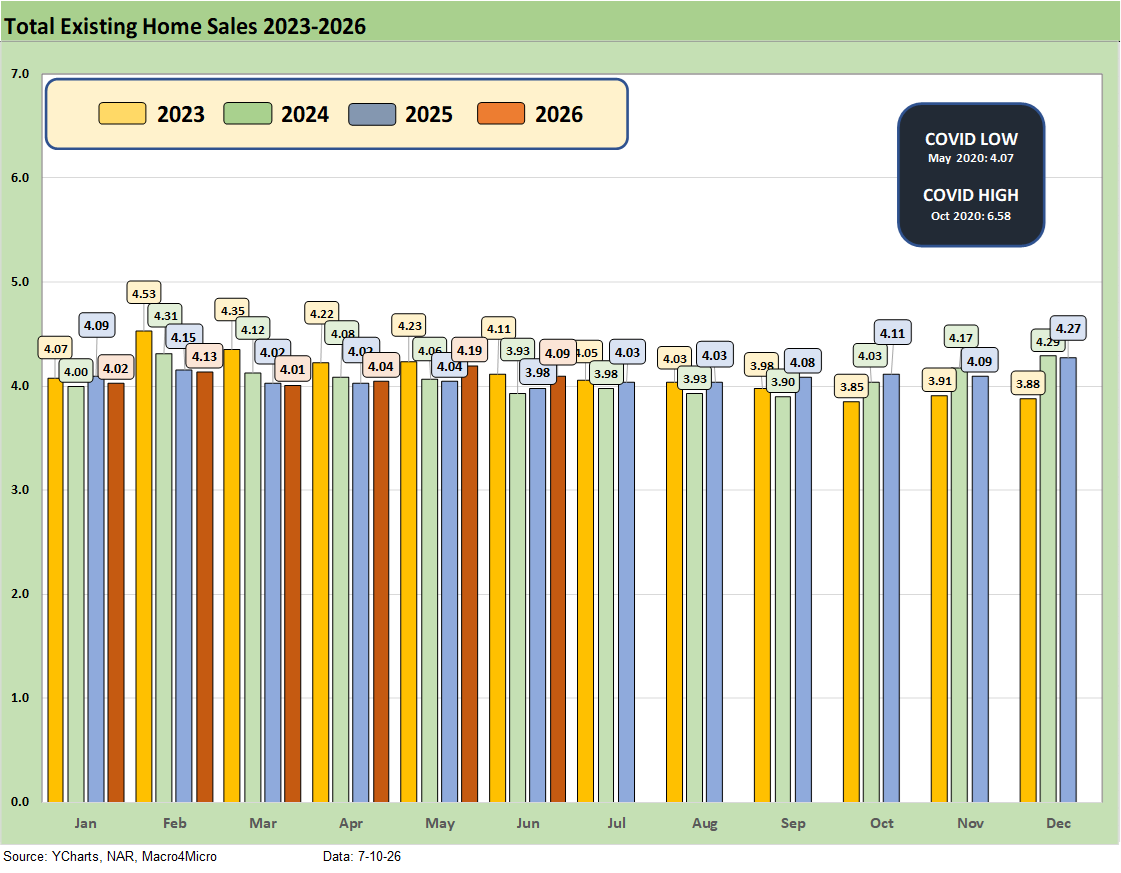

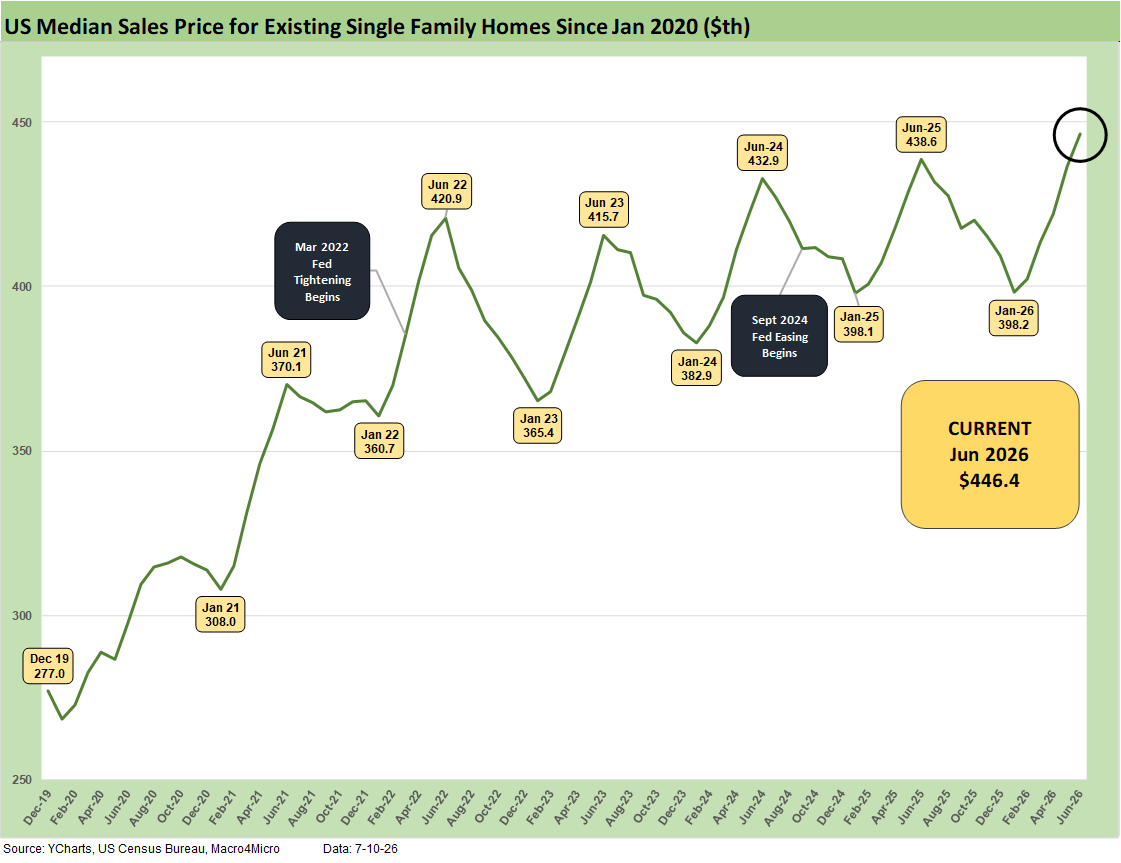

A major stall in existing home sales remains the order of the day with existing sales volumes at -2.4% MoM but +2.8% YoY. Existing home sales are mired in the low 4 million handle range at 4.09 million vs. 4.19 million in May 2026 and 3.98 million in June 2025 when numbers looked more like 2023 when mortgage rates were even higher. The median price hit a record high for total existing homes ($440,600) and single family ($446,400) as prices keep affordability strained even as inventory ticked lower.

Negative real wage growth is not helping the housing sector story line at the macro level. The cost of the household goods and services basket relative to consumer cash flow is a different challenge than the inflation debate (recurring price increases). The affordability headlines often prompt semantic exercises from economists and policy makers on inflation vs. one-time moves, but the purchasing power problem remains in place for consumers even if headline CPI and PCE price indexes get under control. For now, the current 4% handles for CPI and PCE are grim (see Personal Income & Outlays May 2026: Bad Inflation, Balanced Spending 6-26-26, CPI May 2026: The 4% Rubicon 6-10-26).

The inflation anxiety will necessarily remain high and unpredictable with the setbacks in Iran and renewed problems for the Strait of Hormuz supply bottlenecks (oil, LNG, aluminum and various materials side effects including copper, etc.). We get CPI and PPI updates this week along with Housing Starts and Industrial Production, so the cyclical color will offer some fresh visibility at the same time the wave of bank earnings is streaming out and 2H26 guidance will be getting digested. The earnings expectations are bullish so the inflation handicapping will heat up with it.

As of Saturday morning, the FOMC odds remain grim according to FedWatch CME models. The odds of 1 cut by the Dec 2026 FOMC meeting date are 0% while the odds of 4 hikes are higher than that at +1.6% with the odds of unchanged at 14.6%. With respect to the hike odds, we see 1 hike at 37.8%, 2 hikes at 33.7%, 3 hikes at 12.3%. The 30Y mortgage rate stood at 6.64% as of late Friday per the Mortgage News Daily survey. The new Thursday Freddie Mac benchmark was set at 6.49%, up from 6.43% last week and down from 6.72% last year at this time.

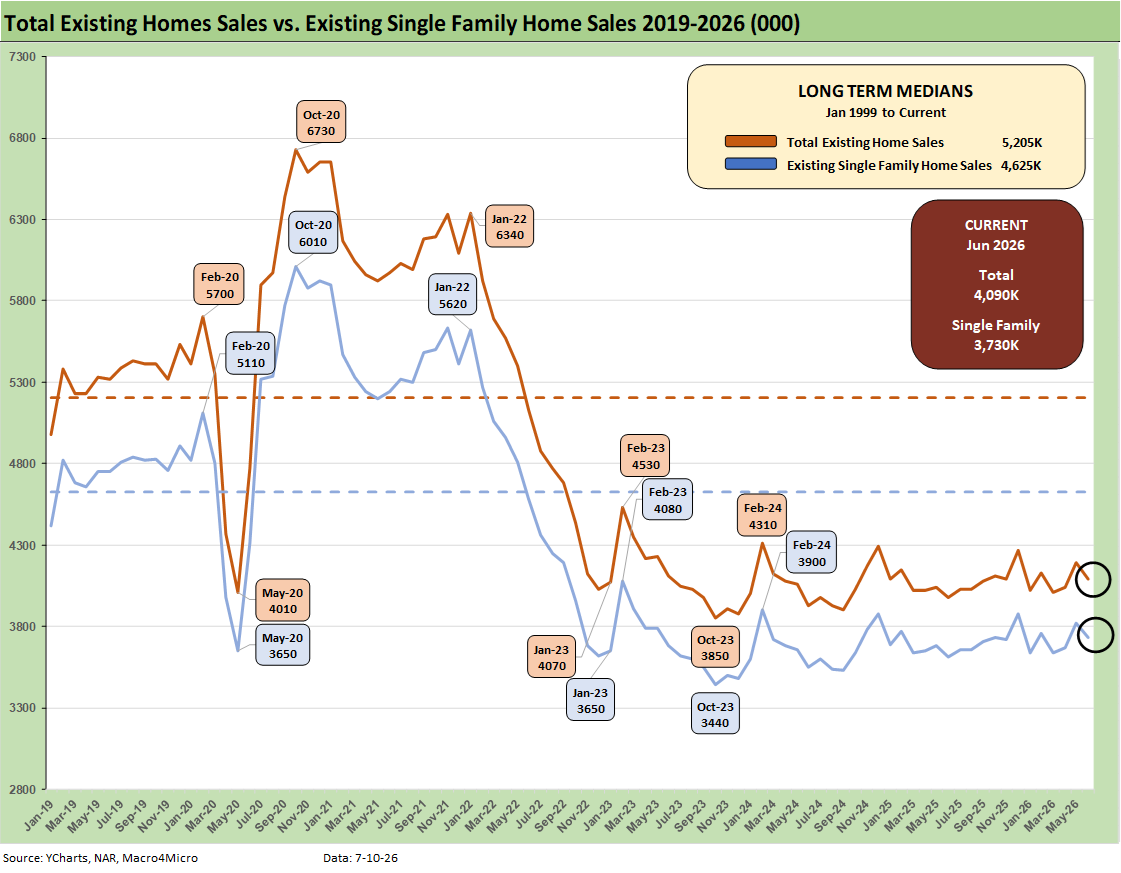

The above chart details existing home sales SAAR run rates by month from January 2023 to June 2026 with 4.09 million in June 2026, down from 4.19 million in May 2026. As a frame of reference, in 2022 the market was posting 6 million and 5 million handle sales volumes in the first half of that year.

The recent existing home sales totals look more like the late 2023 period when mortgages had peaked (see Existing Home Sales Dec 2023: Rerun of Multi-Decade Low 1-19-24). The 30Y mortgage rate has moved within a 200 bps range since the Oct 2023 peak when Freddie Mac 30Y hit 7.8% and many mortgage offerings were near 8%.

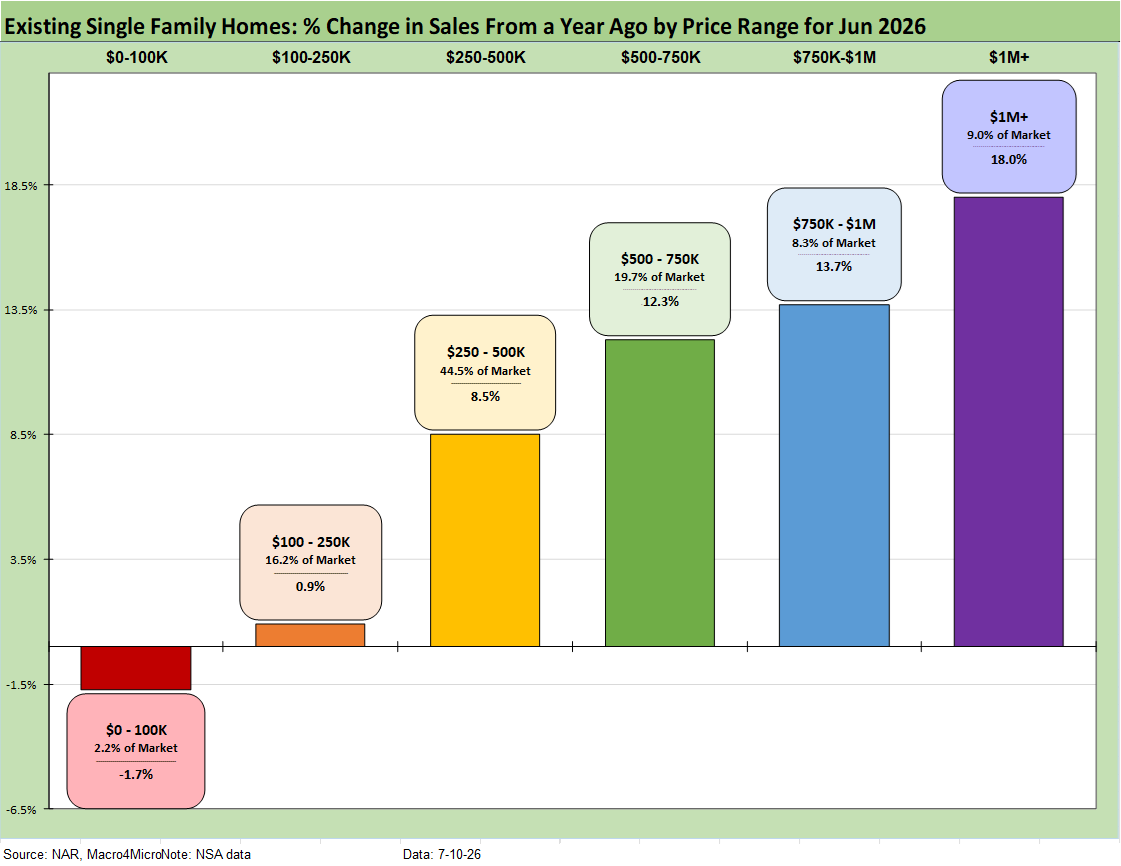

The above chart shows the sales volume delta by price tier for June 2026, and we see 5 of the 6 price tiers posting positive growth with only the lowest price tier posting a decline. Note: We use “not seasonally adjusted data” for this chart.

For existing home sales, the monthly payment math is still unfavorable for those looking to cash out, move up, or simply relocate. Expectations for a bull flattener in the UST market that would translate into low to mid 5% mortgage rates have been crushed at this point for 2026 after major setbacks for that same scenario in 2025.

As noted in the bullet points at the top of the commentary, the market is pricing in 0% chance of Fed easing, and it is a very challenging leap of faith to see any probability of the conditions for easing getting better from here given steady payrolls and rising inflation. The Iran setbacks along with sustained inflation pressures do not offer much hope for a sharp move lower in the 10Y UST, which in turn dictates moves in 30Y mortgage rates.

An easing scenario would require a macro backdrop that hits payrolls and homebuyer confidence to make the FOMC take such action. That would require a radical event at this point. Such a move by the Fed could also drive a UST steepener subject to the underlying reasons used by the FOMC.

The oil spike and price swings since Iran plus the documented inflation pressures will make life a challenge for Warsh. The years of “repricing of the household basket” under Biden and again under Trump has made life a struggle for many and now we are looking at negative real wage growth.

We read a comment in Housingwire that highlighted slower home price growth vs. wages, but the funding costs (mortgages) and broader expense base that comes with home ownership and relocating undermines such a household budget assessment. The cash-in, cash-out analysis still says home ownership is mired in an affordability crisis in terms of the cost of ownership when considering financing and operating costs.

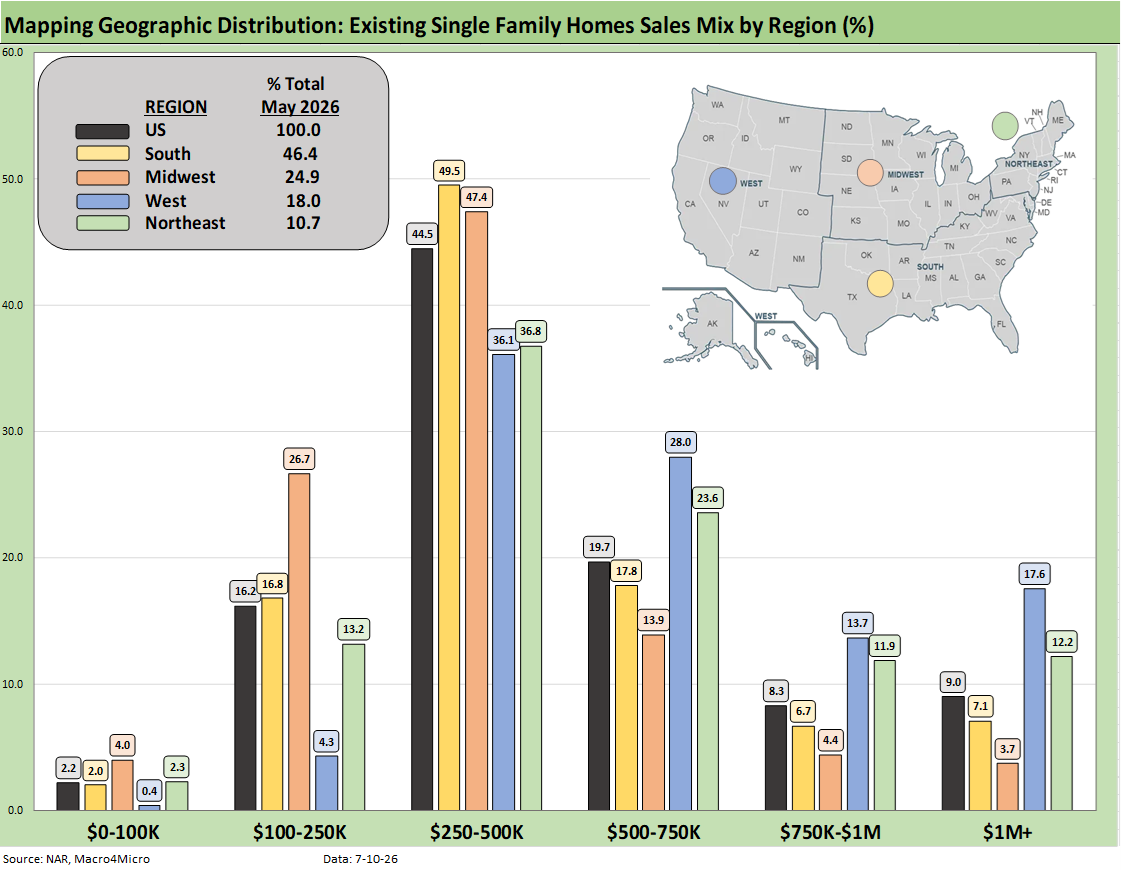

The above chart shows the geographic mix of volumes and details on price mix by region. The South is the main event in single family volumes whether new or existing at over 46% of total volumes.

For the bar chart, we break out the mix for each region by price tier. For example, the South shows almost 50% of its existing home sales volume in the $250K to $500K range and almost 17% of its sales in the $100K to $250K bucket.

The high cost of homes in the West (notably California) is clear enough just by glancing at the bar chart with over 17% at prices over $1 million. The second highest in the $1 million club is the Northeast at over 12%.

We see a major concentration across the regions in the $250K to $500K although the $100K to $250K bracket for the Midwest stands at almost 27%. The West shows a high share of 28% in the $500 to $750K bracket, which again underscores how expensive the West region price tags remain in national context.

The map explains what states are in each Census region. There is a very wide range of home price profiles in the West and Midwest states.

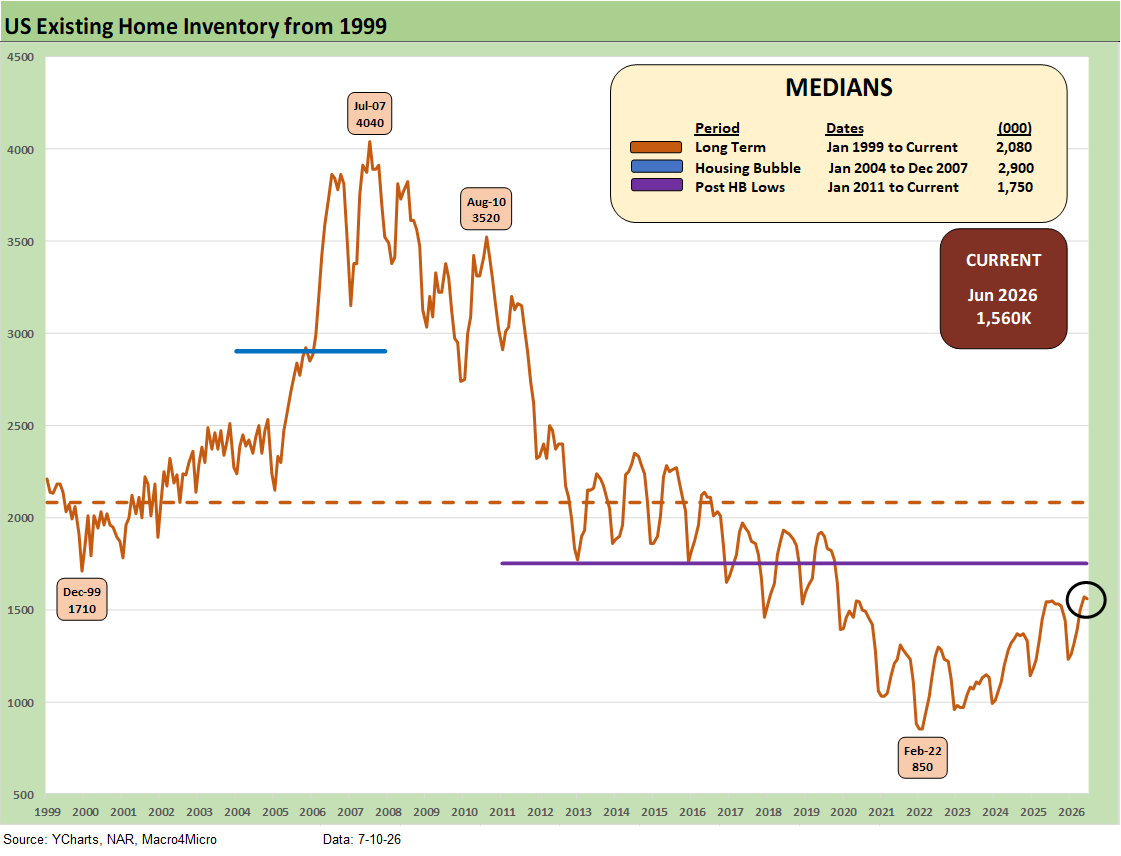

Inventory for total existing homes ticked lower MoM to 1.56 million units for -0.6% MoM and +1.3% higher YoY. Current inventory is well below longer term medians including 2.08 million for the post-1998 median. The median from Jan 2011 (homebuilding low) to current times is 1.75 million. In other words, existing home sales inventory remains low even if the level is materially higher than the stunning low of 850K of Feb 2022 ahead of the end of ZIRP and start of the tightening cycle in March 2022.

The existing home inventory balance had shown a steady rise off the sub-1 million lows of 2022. Inventory had risen to the 1.3 million handle range in 2024 before dipping back down to a recent low of 1.14 million to close out 2024. We bounced off those numbers in 2025 to get back above 1.5 million handles before the recent move lower to 1.2 and 1.3 million handles and then back to current levels above 1.5 million.

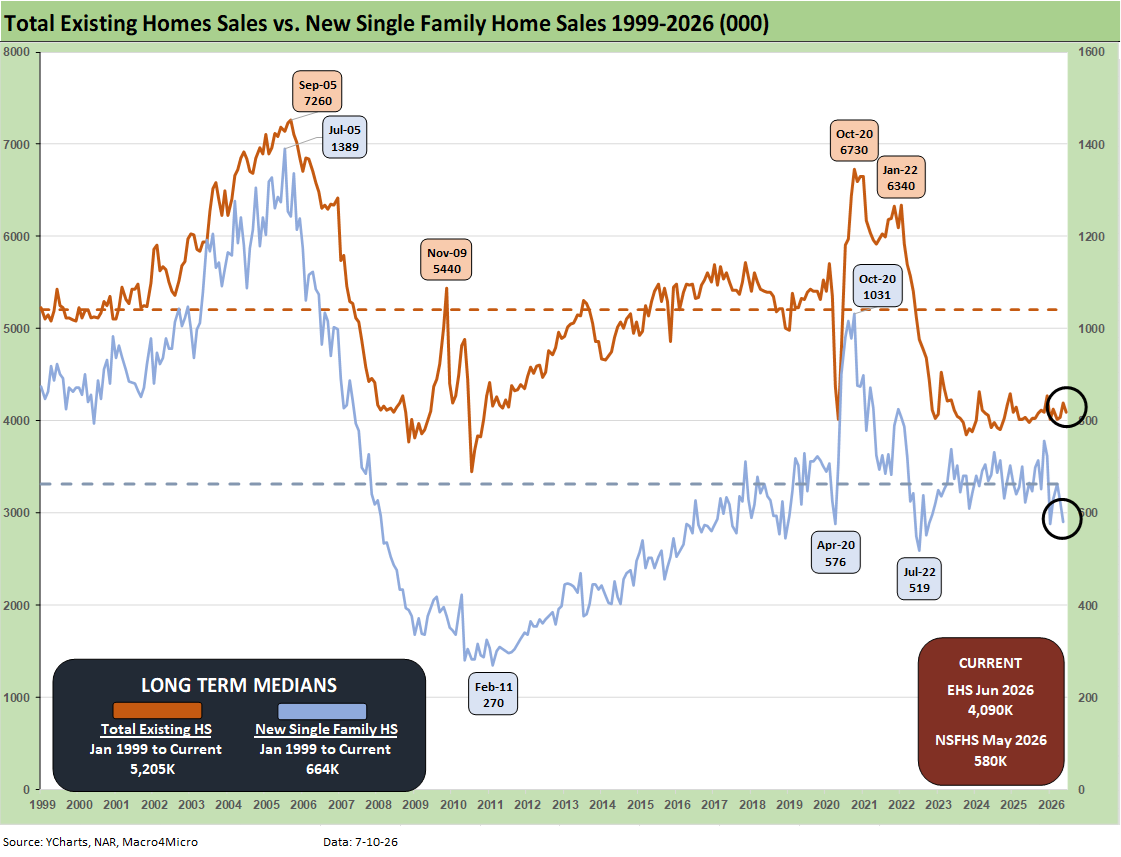

The above two-sided chart updates the trend line in total existing home sales vs. new single family homes. After some material disruptions in the data updates during the shutdown, the new home sales data is current again (see New Home Sales May 2026: Weak Volumes, Stable(ish) Prices 6-25-26). It’s clear that both are low in historical context. Notable exception is the post bubble housing crisis.

The above chart breaks out the timeline for June existing single family only of 3.73 million vs. total existing home sales of 4.09 million. The 4.09 million total is well below the long-term median (from Jan 1999) of 5.2 million. The total of 3.73 million for single family is well below the long-term median of 4.63 million.

Existing single family growth was -2.4% sequentially and +3.3% YoY (SAAR). The lower line is ex-condo/ex-coops. We saw 360K in condo and coop sales in June 2026, down from 370K YoY and down from 370K MoM.

The above chart updates the median price for existing single-family homes at $446.4K (vs. $440.6K for total existing). That is above the June 2025 level of $438.6K. The median price in June 2026 is at an all-time high and dramatically above the $308K level back in Jan 2021 and $277K in Dec 2019. Mortgage rates were in a different zip code in Jan 2021 were below 3%.

The above chart shows another angle on the sales mix across the price tiers. We just lift the numbers off the monthly handout for single family homes released by the NAR each month. Higher price homes and wealthier buyers have had a better time across this cycle. The “K recovery” certainly applies in housing given the mortgage pressure on monthly payments.

This pattern feeds the dynamic of builders targeting higher price homes vs. starter homes. Meanwhile, the funding costs of a home purchase (new or existing) are a deterrent to “move-up” sales by existing homeowners facing much higher refinancing costs if they are sitting on 3% and 4% handle mortgages. That remains a major headwind for existing home sales volumes.

The $250K to $750K range is comprised of two tiers that add up to almost 2/3 of the market with the $100K to $250K showing a big share in some of the Midwest states as detailed in an earlier chart.

We looked at the growth trends for each tier earlier. The lowest price tier saw volumes decline while the top 5 tiers rose. The lower price tiers are more on the cusp of where affordability and mortgage eligibility could be strained at 6.6% area handle mortgage rates (based on Friday’s close in the Mortgage News Daily survey).

The existing home sales trends make for overall unfavorable news for the housing sector in terms of volumes and prices.

See also:

Market Commentary: Asset Returns 7-5-26

Happy 250th Birthday America 7-3-26

Employment Situation June 2026: Back to a Crawl 7-2-26

JOLTS May 2026: Openings Flat, Hires Down, Layoffs Up 7-1-26

Music to Ponder: Hope Rising or Blood Simmering? 6-30-26

The Election Gambit: Economic Risk and Policy Uncertainty 6-29-26

JD Vance and Nixon History: Clueless 6-27-26

Personal Income & Outlays May 2026: Bad Inflation, Balanced Spending 6-26-26

New Home Sales May 2026: Weak Volumes, Stable(ish) Prices 6-25-26

GDP 1Q26 Final: PCE Growth Plunge 6-25-26

Trade Deficits: The Moving Parts and Macro Goals Matter Most 6-24-26

The FOMC Dance: Will Warsh and Trump Find a Rhythm? 6-17-26

Housing Starts May 2026: Weaker for both Single Family and Multifamily 6-16-26

Industrial Production May 2026: Steady, Balanced Utilization Levels 6-15-26

Geopolitical risk: Trump’s Nuclear Saber Rattling? 6-14-26

Producer Price Index May 2026: Too Many “Since 2022” References 6-11-26

CPI May 2026: The 4% Rubicon 6-10-26

Remembering D-Day: June 6, 1944

Employment May 2026: Big Rebound, Low Multiplier Bias 6-5-26

The Fall of CBS 6-3-26

Retail Signal Read Part Deux 6-1-26