Industrial Production May 2026: Steady, Balanced Utilization Levels

The slight uptick in Industrial Production and Total Industry Capacity Utilization saw both at the highest levels in calendar 2026.

Now if manufacturing would only add more jobs (still lower YoY)…

The industrial production and capacity utilization trends offered some cyclical reassurance by showing the capex boom seen in the GDP lines and resilience in the consumer durables sector (16M handle light vehicle expectations in 2026) has offered macro support. The overall mix of factors has helped ease some of the recurring and justified worries around the consumer (see GDP 1Q26 Second Estimate: Shrunk in the Dryer 5-28-26).

The +1.4% PCE growth in 1Q26 (through 2nd estimate), plunging savings rates (see PCE Inflation: Income and Outlays April 2026 5-28-26), and eroding credit card metrics will keep macro watchers on edge. PCE remains around 68% of GDP and we get the final estimate for 1Q26 next week.

The collective battering of tariffs on the durables sector cost structures and post-Iran energy cost hammering from industrials to households reminds everyone that it takes an “awful lot of awful” to drive a contraction. The capex cycles and well-known appetites of the US consumer “to consume” is hard to derail even with unsound (incoherent?) trade policies and top-down political instability.

Inflation has been the main consumer worry, and the deal getting to the finish line is more important than Trump selling the story that it is a better deal than Obama’s (good luck) even before tabulating the damage on so many fronts.

The best news in the industrial production mix was that the durables sectors we routinely detail in the charts ticked higher sequentially – even if minimal in some cases.

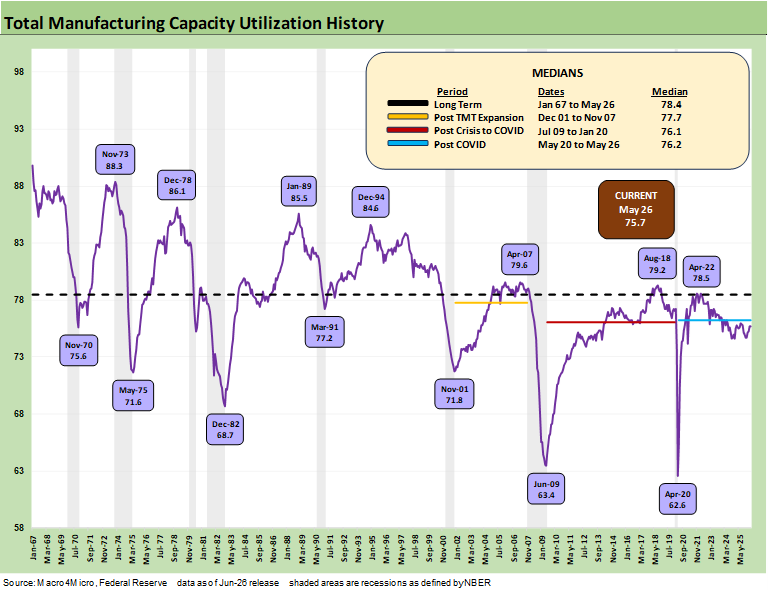

The above chart is somewhat of a regular replay of the history of the industrial production cycles across time from 1967 through today. We have covered much of this in the past, but we roll the historical recap forward for convenience. We get new readers and students all the time. It is a mini history.

As an “old guy” who covered such industries as autos and steel credits back in the 1980s (and worked on a few audits of resources and energy companies) and came of working age in the first stagflation wave and oil spikes of the 70s and early 1980s, we see much of the “old and new” these days to consider. Cyclical change and secular trends always get mixed in, and the evolution (or collapse) of industries is not new.

The current 75.7% for total manufacturing is well below the long-term median of 78.5% and below the post-COVID median of 76.2%. The industrial production and capacity utilization numbers are among many metrics that take the label of “greatest economy in history” off the table right now. Whether GDP growth or payroll trends, the current economy is a bottom quartile economy when the growth of the 1980s and 1990s are factored in (see Presidential GDP Dance Off: Clinton vs. Trump 7-27-24, Presidential GDP Dance Off: Reagan vs. Trump 7-27-24).

The wildcard for this current cycle is the scale of the fixed investment that is now ramping up around the AI ecosystem. The multiplier effects cut across the full array of products and services and extend across many major trade partners with Taiwan at the top of the list (see Taiwan: Stakes are High, US Awareness is Low 5-17-26, US-Taiwan Trade: Risks Behind the Curtain 2-1-26).

The consumer sector and PCE have been unimpressive, but fixed investment is now soaring (see 1Q26 GDP Advance Estimate: Consumer Fade, Investment Boom 4-30-26). If you like comparing numbers (not a Washington thing) as opposed to spewing partisan adjectives, Trump 1.0 did not even frame up all that well vs. Carter and Biden – let alone the 1980s and 1990s (Gut Checking Trump GDP Record 3-5-25, Trump’s “Greatest Economy in History”: Not Even Close 3-5-25). Trump 2.0 is off to a slow start on GDP growth and payroll additions relative to the earlier glory years of the 80s and 90s.

A brief cyclical lookback on replay…

The chart shows the material swings across expansion booms and busts. That includes the aftermath of some highly damaging oil spikes that brought on cyclical weakness and later saw capacity utilization plunge. There were a lot more structural changes underway in those cycles than just oil and gas price pressures.

The pace of industry restructuring was notably the case in the 1980-1982 double dip as well as the recession of late 1973 to early 1975 when the Arab Oil Embargo set off chain reactions that turned the post-1973 period into an ebb-and-flow of macro nightmares for inflation and the consumer. Currency trends and labor costs were going through major changes across many years.

The May 1975 low of 71.6% followed the first bout of severe stagflation that unfolded after the Arab Oil Embargo. The 1980-1982 double dip recession came after the 1979 inflation spike took off with the Iranian oil crisis.

Capacity utilization saw a 68.7% low in Dec 1982 as the economy was just coming off the recession trough. The first Gulf War came after the August 1990 invasion of Kuwait with capacity utilization hitting a low in March 1991 at 77.2%, which is above where capacity utilization stands now in 2026.

Bring on the tech boom and excess…

The age of tech and credit excess in the late 1990s brought some new swoons with 71.8% in Nov 2001 after the TMT meltdown and HY default wave rolled in. The Utilities and Power sectors and Telecom capex all took a beating in that time frame.

Then came the post-credit crisis low of 63.4% at the recession trough in June 2009. Mortgages and derivative excess caused a very real systemic panic and deep risk aversion from the Lehman Sept 2008 period and well into 2009. That period was famous for the bankruptcy and bailout of GM and Chrysler and how that reverberated across supplier chains from materials to components. The credit contraction was very real, and the recovery in payrolls was slow to unfold with the consumer hammered by housing sector pain.

COVID edged out the June 2009 utilization bottom with a record low of 62.6 in April 2020 and a wild 2-month recession. That pandemic period saw ZIRP, supply-demand imbalances and later the Russian invasion of Ukraine and ensuing oil spike that set off inflation and a tightening cycle that still did not trigger a 2022 recession. The Fed should get some credit for navigating that timeline even if late to the party.

Time for the new age transition to AI plus some old school crises…

As we detail below in the recession histories, the idea of what is low or high for capacity utilization in the context of corporate sector profitability is not as direct as one might think. Breakeven volumes, cost structures and pricing power are key drivers of profits. The tariff excess as a core Trump policy only makes that unit cost analysis more complicated as we head into a new round of energy related cost pressures in 2026. Material costs, operating costs for companies, and consumer discretionary household cash flow headwinds make for a tricky set of moving parts shaped by erratic geopolitical decisions.

The AI upside as well as the fallout and related fears is also a new variable in the mix that cuts across both the services and goods sectors. What AI will mean for productivity improvement vs. payroll contraction will be an ongoing test of theories. Even if AI proves true to the valuation promises and brings a “revolution” to the economy, many will also pay the price. Revolution is a term often associated with a body count (even if jobs and not KIA). We have been getting a taste in the recent SaaS services panic. Those SaaS services markets consume a lot of goods and have a lot of employees.

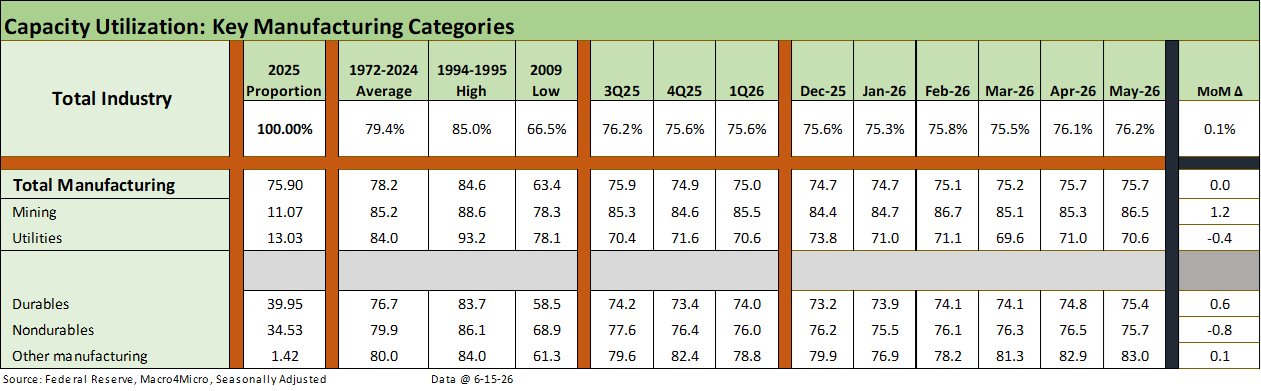

The above table breaks out the high-level groupings with total industry and total manufacturing posting a mix of positive and negative variances in May 2026. We include a “delta column” on the right.

Mining and Utilities were mixed for the month, but a rational expectation is that utilities will see more capacity added and more demand. The data center and power supply issue is more pressing and getting more political by the day in an area where there has been working class bipartisan anger around the side effects of such projects on power costs and water threats among other issues. That controversy has spread to Canada.

It may be local on a center-by-center basis, but it will find its way into an assessment of data center adequacy at some point for growth valuations, revenue models, and costs. Any sense of faltering optimism around volumes (e.g. international restrictions on AI), pricing power, and regulatory backlash or political risks (elections have consequences, etc.) could roil valuations.

We see Durables and Nondurables as the main events to track, and durables showed notable strength this month. The durables sector is especially important with all of the supplier-to-OEM multiplier effects. That also is the sector more meaningfully tagged by the Trump tariff policies.

The IEEPA SCOTUS setbacks and recent attempts by Trump to counterattack by creatively using existing tariff legislation is struggling in the courts. Trump goes to “Plan B” and “Plan C” in his attempts to cut Congress out of the tariff decisions. He is hanging his hat on Section 301. This week he threatened France with triple digit wine tariffs even without IEEPA. He seems to forget the EU works as a bloc.

Looking back from 2025 into early 2026, we see Manufacturing in a relatively narrow range and the same for Durables. Tariffs have not moved the production needle much so far, but that does not tell the profitability story on the tariff cost impact. Most people (outside the White House) know that buyers/importers write the check for the tariff, so that implies a higher breakeven volume or some offsetting action on other costs or pricing.

Those tariff impacts will only play out over time across working capital cycles. Pricing decisions are more likely to come at a lag given the White House pressures, so there is a lot more to play out in 2026 earnings seasons and in company color.

The inflation story has turned negative for the macro picture in 2026. The “good news, bad news” aspect of a resilient industrial sector is that higher input costs can lead to the exercise of pricing power that flows into inflation. That beats the stagflation alternative but will keep life challenging for the FOMC and “Team Warsh” (if he can assemble a supportive voting team). We get our first taste of Warsh this week.

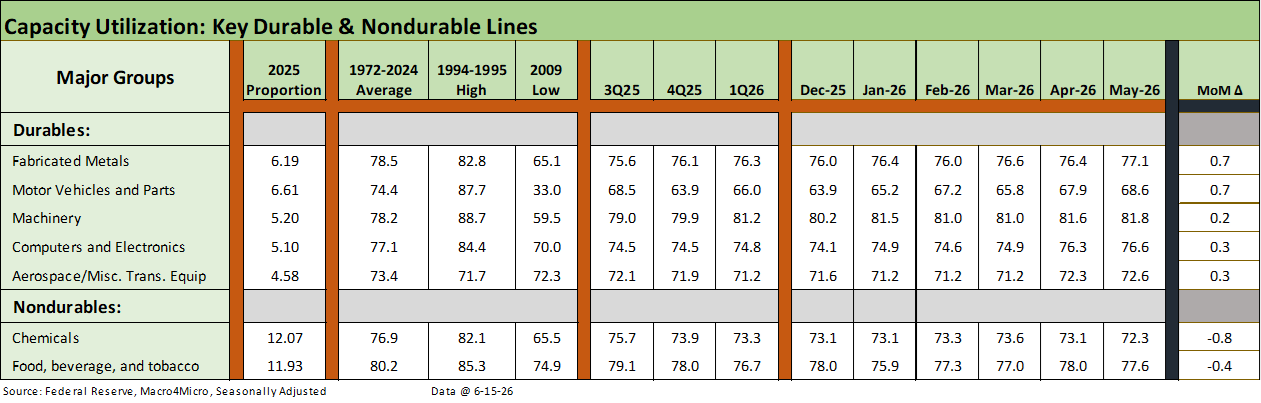

The above table breaks out the details for the top 5 Durables lines and the two largest Nondurables lines. We include the capacity utilization deltas in the column on the right. We see positive moves across all the major durables industries presented with “Fabricated Metals” and “Motor Vehicles and Parts” making the more notable moves. The two major Nondurables lines were both lower with Chemicals down by more than Food, Beverage and Tobacco.

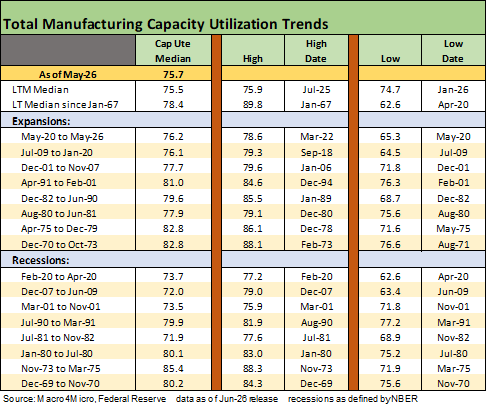

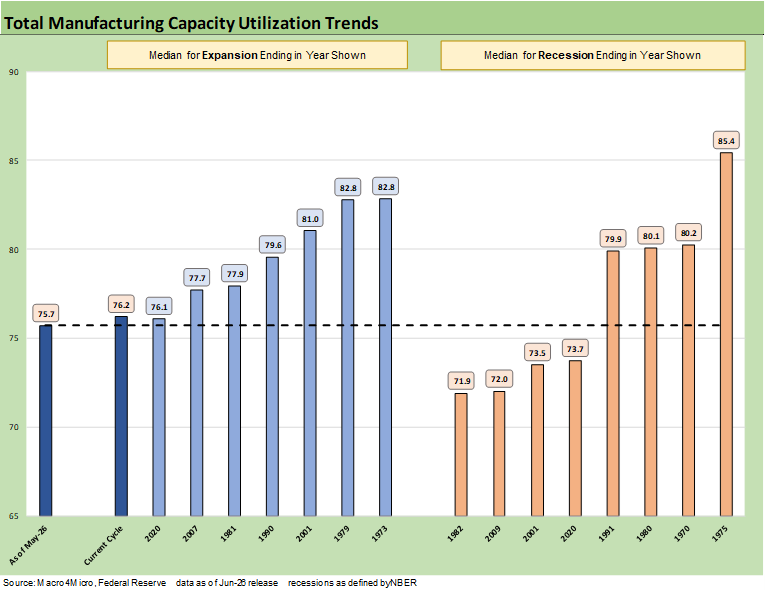

The above table updates the capacity utilization history for expansions and recessions. As we routinely discuss, the ability of companies to generate solid profits at lower capacity utilization in today’s markets relative to past cycles is tied to both automation and the evolution of low-cost global supplier chains.

Low-cost supplier chains are getting undermined by tariffs and are now facing supply chain headwinds from the Iran War energy effects and the supply-demand imbalances. The latest round of news on a “deal” will ease some worries along the supplier to customer chain, but there are always lags while more tariffs are rolling in.

The “AI story” and what it all means for productivity and headcount will be a big part of the risk analysis ahead. The natural outcome will be less jobs in a service intensive economy such as the US. The irony is that the most immediate impact on jobs has been in tech, but that can easily spread.

The above chart details economic expansion and recession averages and lines them up by height as a frame of reference. We see the current level on the left at 75.7%. The fact that the current capacity utilization is below numerous recession averages posted on the right side of the chart also scoffs at the recurring “Golden Age” and “hottest country” rhetoric.

In the context of the tariff priorities and reshoring ambitions, the slack capacity implied by the chart in historical context underscores that the analysis is a lot more complicated than just “build more plants” and “keep tariffs high” to force reshoring. That is a story told on an industry-by-industry basis. It gets into themes around pricing power, cost structures and sourcing risks (tariffs, etc.). These days the topical questions revolve around “AI winners and losers” in productivity and the relative ability to adjust and engage in tariff cost mitigation strategies.

The multiplier effects are important, but the relocation of supplier chains and OEM assembly relocation and retooling is by definition very slow to unfold given intrinsic lag times, tooling equipment, and contracts in place. Manufacturing jobs edged slightly higher this month on a MoM basis but remain lower YoY (see Employment May 2026: Big Rebound, Low Multiplier Bias 6-5-26).

There is also the fact that the cost of relocation has risen with all the tariff effects for materials, components, and qualified labor. Autos are the main relocation stories, but that is generally going to be tied to existing infrastructure and not a strategy of all-new greenfield plants. In the end, many companies can just wait for Trump to “move on” and revisit plans later.

The issues around the USMCA review and its fate effectively make planning much more difficult if not impossible to do with clear economic certainty on trade rules. Trump’s signaling that he may terminate the USMCA entirely regardless of any legal interpretations on whether his sole-actor decision is even legal. That adds more drama to a policymaking framework that does not lack drama in the best of times and even injects surprise endings.

See also:

Market Commentary: Asset Returns 6-14-26

Geopolitical risk: Trump’s Nuclear Saber Rattling? 6-14-26

Producer Price Index May 2026: Too Many “Since 2022” References 6-11-26

CPI May 2026: The 4% Rubicon 6-10-26

Remembering D-Day: June 6, 1944

Employment May 2026: Big Rebound, Low Multiplier Bias 6-5-26

The Fall of CBS 6-3-26

JOLTS April 2026: A Modestly Positive Turn 6-2-26

Retail Signal Read Part Deux 6-1-26

New Home Sales April 2026: Slow Start to Spring 5-28-26

PCE Inflation: Income and Outlays April 2026 5-28-26

GDP 1Q26 Second Estimate: Shrunk in the Dryer 5-28-26

Retail Equity Comps: Looking for Signals 5-26-26

Housing Starts April 2026: Soft Starts in Single Family 5-22-26

D.R. Horton: Financial Powerhouse Despite Cyclical Softening 5-20-26