Retail Signal Read Part Deux 6-1-26

Another retail earnings wave shows a mix of good and bad performance in the consumer story.

Gasoline costs how much?!

After our earlier look at the performance of retail equities last week with a wave of earnings reports, we update a broad group of retailer equity returns for the past week (see Retail Equity Comps: Looking for Signals 5-26-26).

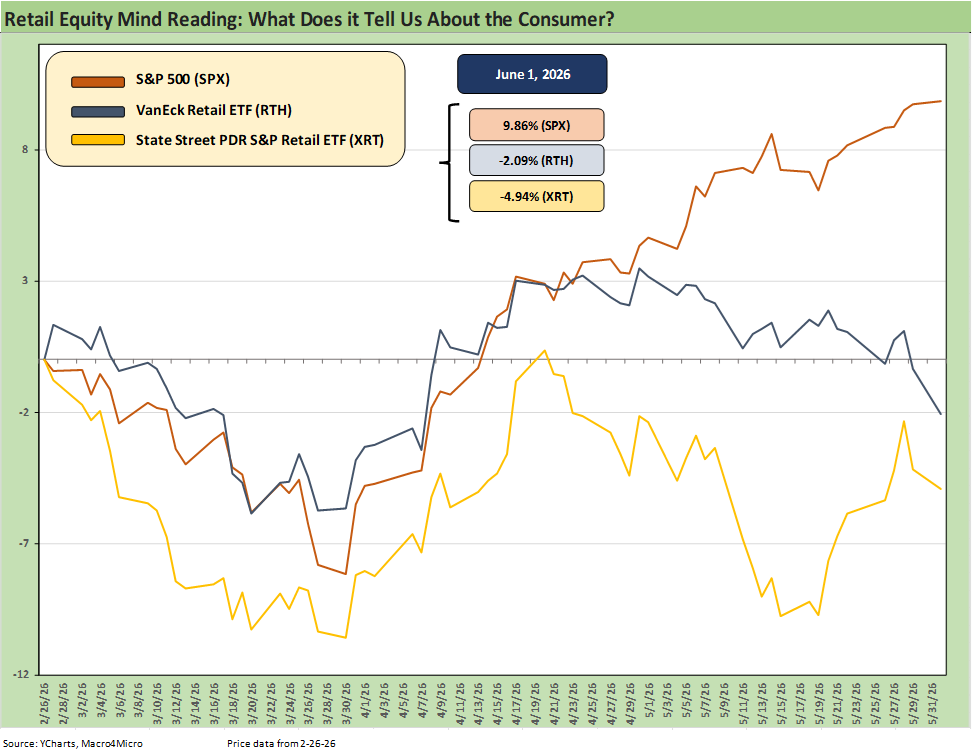

The Hi-Lo range of around 36% (30% if we toss out the Hi and Lo data points) and a positive-negative score of 13-19 tell a very mixed story. The two bellwether retailer ETFs (XRT, RTH) split the difference for the 1-week period with a +1% handle return for XRT (very well diversified) and -1% handle return for RTH (heavy weighting of Amazon and Walmart).

We excerpt some quotes from the management calls that signal the impact of tariffs or summarize their view on the consumer. It is just a flavor sampler.

We discussed the two major Retail ETFs plotted above in a brief retail commentary last week. This update above uses price returns and starts just before the Iran adventure (aka “war”) kicked into gear. RTH is very exposed to Amazon (AMZN) and Walmart (WMT) at around a 35% weighting while the XRT is exceptionally diverse with the largest holding well under 2%.

The negative trend is evident in both. Retail equities are mostly in negative return range since Iran. That is not a surprise given the cost fallout. The chart below for weekly total returns from this past week can be read in conjunction with the earlier note that includes that week as well as a YTD cut of the data. The takeaway is one of winners and losers (as is usually the case in retail peer groups) but also a theme of resilient consumers that are shifting gears on affordability challenges but not in sales contraction mode.

The lower economic tier consumers and value seekers are not a new theme by any stretch, but the news of late has been about strain in credit card debt service starting to appear. Those are more important than soft sentiment indicators. The recent PCE release also flagged a plunge in savings rates to the lowest since 2Q22 at the inflation peak. That is not good news in this case if the pressure on household costs increases from here (see PCE Inflation: Income and Outlays April 2026 5-28-26).

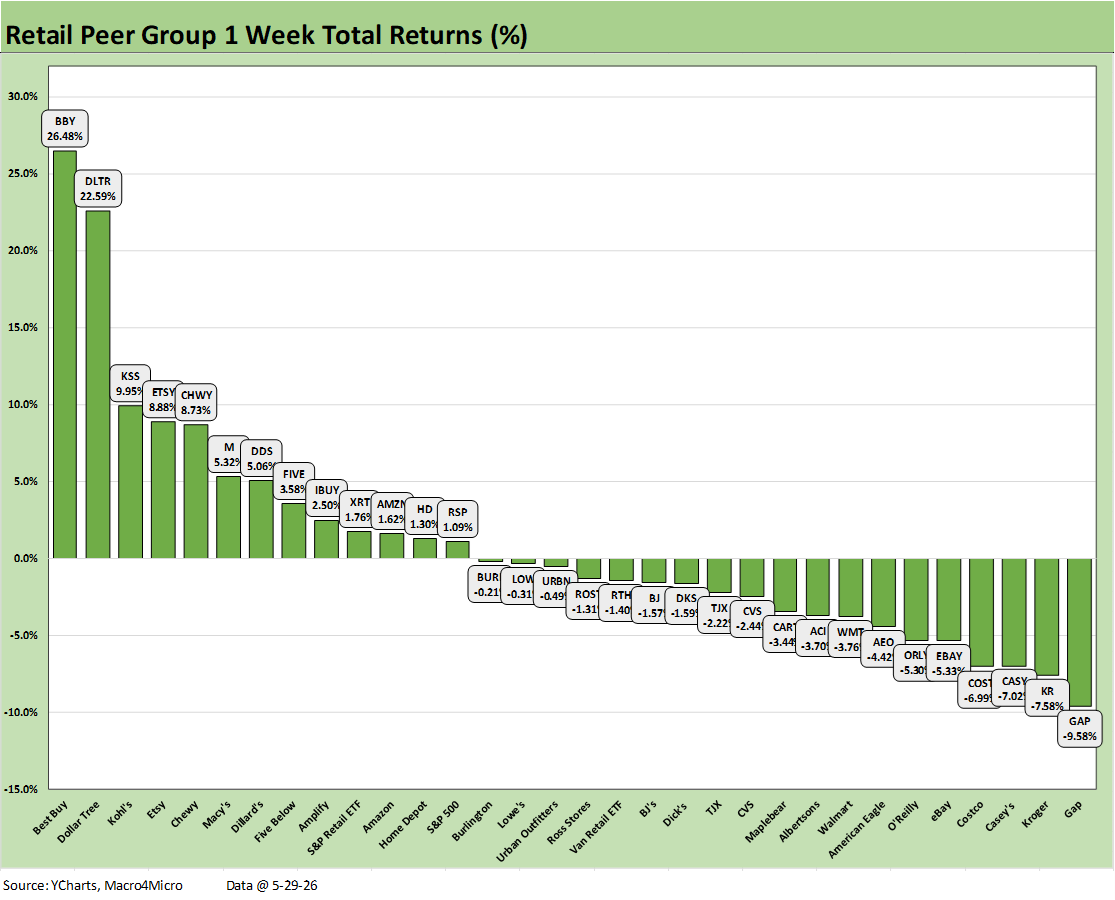

The above chart follows up on what we posted after the first big round of retail earnings. Two weeks ago, earnings releases included bellwether Walmart along with a range of other key players such as BJ’s, Home Depot, Lowe’s, TJX, Ross Stores, Target, and Urban Outfitters among others (see Retail Equity Comps: Looking for Signals 5-26-26).

This past week brought a fresh batch of earnings that provided a mixed but balanced picture with some clear winners and losers. Among the stellar performances on the week as posted above was Best Buy (BBY) and Dollar Tree (DLTR) along with the much smaller cap Kohl’s (KSS) who beat on their numbers and rallied by almost 10% on the week. That doesn’t change the fact that KSS is running at almost -29% YTD.

The profile of returns above shows a lot of negative numbers on the week with The GAP on the bottom. The 13-19 score in the mix shows the Equal Weight S&P 500 ETF (RSP) on the bottom of the positive asset lines at +1.1%. The weighting toward negative returns is suboptimal for retail but not anything resembling a panic button. We ran through a range of press releases and transcript excerpts and looked for brief statements on a few high-level topics to find some cut-and-paste material:

· How do they see their customer base narrowly or the consumer broadly?

· What is happening with tariffs? (they are always very cautious on that political hot button).

We use some from the past week and some from the prior week. We found The GAP disclosure among the more extensive on the topics.

Notable tariff and cost commentary from retailers…

We spot checked for tariff color in terms of margin impact and how some retailers see the world in the post-IEEPA period after the SCOTUS decision and how they are gauging what comes next with Team Trump scrambling to replace the IEEPA tariff revenue.

The apparel companies were especially exposed to the tariffs slapped on low-cost Asian suppliers by IEEPA. The companies see plenty of the same risks ahead with Trump determined (as confirmed by a few of the Cabinet including Bessent) to get tariff revenue back up to their original levels using existing legislation (without any additional use of Congress of course).

The GAP and tariffs:

“Gross margin of 40.5% declined 130 basis points versus last year, coming in ahead of guidance…The 100 basis point decline in merchandise margins reflects an expected headwind from the net impact of tariffs of approximately 200 basis points implying 100 basis points of underlying merchandise margin expansion.”

“First quarter reported operating margin was 12.7%. On an adjusted basis, operating margin was 5.2%, down 230 basis points compared to last year, primarily reflecting the net impact of tariffs.”

“We are updating our assumptions today to reflect Section 122 tariffs at a 10% rate on goods received after February 24 through the July 24 deadline. For the remainder of the year, we’ve assumed tariff rates revert back to IEEPA level rates incorporated in our original plan.”

“Tying these pieces together, we now expect approximately $80 million or 50 basis points of year-over-year net tariff relief to our gross and operating margin relative to our prior outlook for tariffs to be net neutral for the year. Given the timing of receipts -- this benefit is expected to be weighted towards the second and third quarters”

“We are keeping a close watch on the extent to which companies may reinvest this year’s tariff upside into pricing actions.”

Costco on tariffs:

“Our plan is to return to our members in some form, the portion of tariffs that were passed on to them. How much we return and when depends on a variety of factors, including how much refund money we receive and when it arrives as well as developments in the lawsuit filed against the company regarding the return process.”

“We’re closely monitoring the longer-term inflationary impacts of higher oil prices as well as the future impacts of tariffs. Our buyers continue to demonstrate their ability to adapt and are using their significant experience and expertise to try to reduce the impact on prices for our members. Our goal is to be the first to lower prices and the last to raise them…”

Best Buy on costs and prices:

“In Q1, our blended computing ASP was flat to last year, largely as a result of product mix and the staggered implementation of these product price increases.

“I will touch on how we are navigating the impacts of memory cost increases, which mostly impacts our computing category. As expected, product costs have been increasing and product price increases have been flowing into our assortment.”

“We’ve seen evidence of this with our customer behavior in the past situations, most recently in response to tariffs. We have also made some strategic decisions to pull forward supply in certain areas to alleviate these impacts, as you can see from the growth in our inventory on our balance sheet in the first quarter.”

Dollar Tree on costs and tariffs:

“Against a backdrop of ongoing uncertainty around fuel costs and tariffs, we will continue to protect value while strengthening the quality and relevance of our assortment. In this environment, our powerful combination of value, convenience and discovery continues to resonate with customers across all income levels and a wide range of shopping occasions.”

“…we are assuming that the current tariff rates remain in place through July and then increase in the back half of the year to the levels predating the February 20 Supreme Court decision. Additionally, we’ve not included any tariff refunds in the outlook.”

Burlington Stores:

“…we expected tariffs to be less disruptive to pricing and supply this year. Well, check, that is what we are seeing. The supply of off-price merchandise is excellent right now.”

Kohl’s:

“The total tariff refunds we are eligible to receive is $190 million. We did not receive any tariff refunds within the first quarter… There’s no tariff refund in any of the estimates that we had given today. Obviously, we talked about the fact that we did apply for those but we haven’t received those refunds yet. So those will be all on top of the numbers that we have guided today.”

“We serve a middle to lower-income customer. So this is very important to them. So we’re going to make sure that we continue to lean in on that. So I think those kind of become your balancing factors, and that’s really where you get to the guide of that flat to slightly down giving us some room”

Walmart:

“on tariffs, we are availing ourselves of the process to get refunds. We would definitely bias and try to prioritize price investment for that, given what we’ve seen both in terms of the pressure on consumers from fuel prices, but importantly, as well as the retention and the share gains that we’ve had, we think the single best return that we can have on a $1 of capital right now is to invest in the customer and invest in price.”

BJ’s:

“…we invested considerably in value during the quarter by returning tariff refunds to our members through pricing… we made the investments in price not really in response to any particular competitor, but really just to use the opportunity we had from the tariff refund to invest in our membership for the long term.”’

TXJ:

“we have submitted for tariff refunds, but our guidance currently does not assume any benefit from any potential refund and nothing more to add on that…”

Home Depot:

“obviously, as we stand today, we could say we could see potential cost pressures building in the form of fuel prices and other commodity input costs, new tariffs have been introduced. But the environment is changing almost every day. And so it’s hard to see where all of that winds up and where it settles…”

“…we see increased fuel costs, not only hitting us directly. Obviously, we obviously have a considerable amount of transportation expense in our P&L but also in the form of input costs. At the same time, number one, it’s still very early in the year. And number two, there are some potential tailwinds here. We’ve talked in our sector about tariff refunds. We have filed for those tariff refunds. And while we don’t disclose the amount and while we have received an immaterial amount to date, we have assumed… that could provide a significant offset to those costs.”

Sample comments on consumers generally…

The GAP:

“From what we can see today, the consumer remains resilient…”

Costco:

“…we don’t give guidance on what we expect future trends to look like…I would say, in broad terms, what we’re seeing at the moment is just a continuation, I should say, of the trends that we’ve seen in really the last year or so, members being very willing and having the capacity to spend.”

Dollar Tree:

“…we recognize the consumer environment remains dynamic, especially for lower income households, navigating higher fuel costs and broader macro uncertainty. Customers are shopping thoughtfully and closer to need, with a continued focus on affordability, convenience and trip efficiency. Customers value the ability to shop nearby and quickly to stretch their budgets through smaller and more affordable pack sizes and to still find a compelling assortment and discovery throughout the store.”

“On your question about fuel, there was some sort of small volatility in the quarter, but it really wasn’t a factor so much this quarter because of the timing of the conflict and the increases in the fuel rate. We’ll start to see that coming in the back part of the year.”

Burlington Stores:

“…we’re perhaps a little more wary now than we were in March, based on higher gas prices and the potential impact on inflation. We’re watching the trend very closely and looking for any change in consumer behavior, we haven’t seen it yet. But as an off-price retailer, that is what we do. We watch to see how the trend changes. And the benefit of the off-price model, when it’s well executed, is that we can tap the brakes or we can hit the accelerator if we need to.

Kohl’s:

“We continue to see choiceful discretionary spending from our core low to middle income consumer as they remain financially pressured.”

Dick’s Sporting Goods:

“We continue to see a healthy consumer across income demographics with no signs of trading down alongside particularly strong engagement from our younger athletes. Our consumer is really responding to newness and innovation, which is showing up throughout the DICK’S business with broad-based growth across footwear, apparel and hard lines. Given our continued confidence in the DICK’S business, we are raising the low end of our expectations for comparable sales and now expect growth of 2.5% to 4%, up from 2% to 4% previously.”

“…the outlook that we have provided continues to kind of indicate that level of confidence around the core strategies, and we are balancing that against the macroeconomic and the geopolitical landscape.”

Walmart:

“the consumer, especially here in the U.S., they’re telling us they’re feeling some pressure, and they’re looking to Walmart for value… the consumer, increasingly, it depends upon which consumer you’re talking about. We see with our customers that the high income customer is spending with confidence into many categories, while the lower income consumer is more budget conscious and perhaps navigating financial distress.”

BJs:

“While the consumer in the broadest sense has been resilient in the face of continuing challenges, we continue to see a more pressured environment for the lower income households. Elevated costs are weighing more heavily on that segment, and we’re seeing more value-seeking behavior as a result.

TJX:

“… our values and merchandise assortment resonated with consumers across all of our retail banners, and that each of our divisions grew their customer base. Looking ahead, the second quarter is off to a good start, and we have many initiatives underway that we believe can continue to drive sales and customer traffic… we’ll have more consumers looking for value is an opportunity for us going forward…”

Home Depot:

“The underlying demand in our business was relatively similar to what we saw throughout fiscal 2025 despite greater consumer uncertainty and housing affordability pressure.”

“underlying demand was relatively similar to what we saw throughout 2025. So that suggests that our consumer has been remarkably resilient. There’s been a lot thrown at them. But if you look at PCE growth year-over-year, that was similar in the first quarter, that was similar to all of last year. Employment is hanging in there. Wage growth has been reasonably strong. And you look at our core customer, they’re probably amongst the healthiest of all consumers. So they tend to own their homes. They did have that 50% value pop in the value of their homes over the past several years. And their portfolios of equities have also improved