Consumer Sentiment: Inflation Optimism? Split Moods

We dig into the UMich consumer sentiment survey showing minor improvements tied to improving inflation views.

OK, we will agree to disagree on inflation expectations…

Consumer sentiment saw another small improvement this month after plunging from post-COVID highs earlier this year.

This month marks a fifth consecutive month of declining short-term inflation expectations towards pre-inflation crisis territory. The lack of bad news from recent CPI prints is beginning to normalize inflation expectations as they return to a more benign reading.

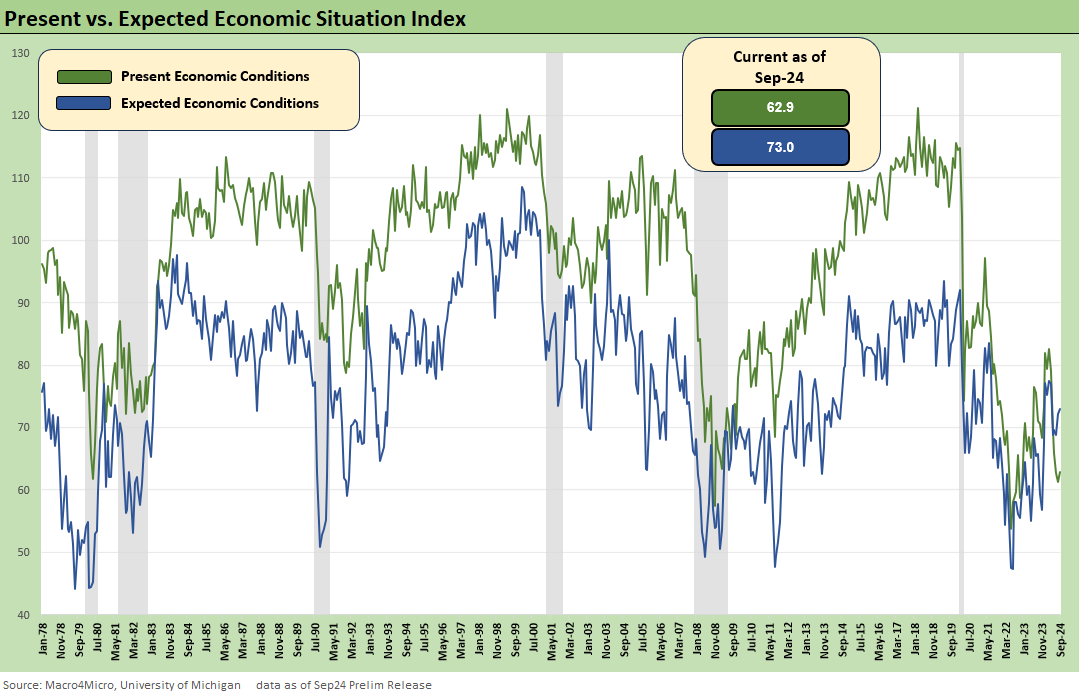

The economic situation piece of the survey also saw minor improvements. The bifurcation between political parties remained as each saw economic conditions diverge further with the boost from Dems carrying this month higher.

This month’s small tick up in consumer sentiment is tied to improvements across the board with the exception of long-term inflation readings which remain anchored to their historical range. This most recent dip in sentiment is differentiated by being driven more by the economic situation section of the survey rather than ballooning inflation expectations. Bridging the disconnect between economic situation borne from the data versus and consumer’s perception is the next challenge in sentiment readings improving further towards past medians.

Recent CPI data showed good news for latest trends coming down to 2.5% for headline. However, the affordability piece of the puzzle and sticker shock after a period of such high inflation remains at the front of consumer minds. Sticker shock on home prices linked to the double whammy on rates and prices also weighs where homeownership is out of reach for swaths of the middle class. We at least saw a drop to 6.2% this week on the Freddie 20Y mortgage benchmark, so that is moving in the right direction. 6% handles are still a long way from the majority of mortgage holders at 4% or below.

The most recent jobs numbers, though positive in the longer timeline context, still have been slowing over 4 of the last 5 months and have been below the longer-term median. Those mixed headlines around what is generally “good-enough” economic data weigh on sentiment. Election stress is a wildcard both in terms of policy divergences and the related risks and also a key sentiment movers given the polarization factor that can be its own self-fulfilling reality.

With a rate cut cycle kickoff almost assured to begin with next week’s FOMC meeting, some consumers could start to see relief on the monthly interest line. Even if they have locked in low fixed rate mortgages, financing in autos and consumer durables (e.g. major appliances etc.) might get some relief. Consumer credit readings have been mixed as the divergence across economic situations becomes more pronounced with Ally Financial earnings this past week making headlines as it reported sizeable increase to auto delinquencies. More money in the pockets of those with variable interest obligations should play out into the consumer sentiment line even if it takes some time to work through.

As we have discussed in previous notes, the division between political parties in the survey remains very stark and is an important driver to the mediocre performance for headline sentiment. The reading for headline sentiment for the month is 92.6 Dem vs. 47.9 Rep, but the gap really widens for current economic conditions where the gap widens further to 90.8 Dem vs. 32.6 Rep. The nation is being driven to distraction (literally and figuratively) by disinformation and political propaganda. Numbers are seldom used in context and with balance, and objective assessment of “higher of lower” is a lot like votes and GDP growth. That is, the numbers and the facts are irrelevant; it is how you feel and who you believe.

The chart above updates the short-term and long-term inflation lines. Short-term inflation expectations are worth highlighting this month as they travelled a long road back down below 3%. The recent reading is the lowest since Dec-20 when we were down at 2.5% and hovering in the neighborhood of 2019 levels. Long-term inflation remains above where it was last cycle but in line with historical expectations and anchored to around 3% in this most recent inflationary environment.

Finally, the above chart plots the history of present and expected economic conditions components of the headline number. Though recovering from a large slide at the beginning of the year, this still remains closer to past recessionary levels. The present economic conditions reading is actually lower than the low during COVID (62.9 vs. 74.3 Apr-20). That is a sign of the times and the state of the political cesspool and mass manipulation.

See also:

CPI Aug 2024: Steady Trend Supports Mandate Shift 9-11-24

Facts Matter: China Syndrome on Trade 9-10-24

Tariffs: Questions that Won’t Get Asked by Debate Moderators 9-10-24

Footnotes & Flashbacks: Credit Markets 9-9-24

Footnotes & Flashbacks: State of Yields 9-8-24

Footnotes & Flashbacks: Asset Returns 9-7-24

Another Volatile Week: Mini Market Lookback 9-7-24

August 2024 Payrolls: Slow Burn, Negative Revisions 9-6-24

Trump's New Sovereign Wealth Fund: Tariff Dollars for a Funded Pool of Patronage? 9

5-24

Goods and Manufacturing: Fact Checking Job Rhetoric 9-5-24

JOLTS July 2024: Mixed Bag, Hires Up, Layoffs/Discharges Up, Quits Flat 9-4-24

Construction Spending: A Brief Pause? 9-3-24

Labor Day Weekend: Mini Market Lookback 9-2-24

PCE July 2024: Inflation, Income and Outlays 8-30-24

2Q24 GDP 2nd Estimate: The Power of 3 and Cutting 8-29-24

Harris Housing Plan: The South’s Gonna Do It Again!? 8-28-24

New Home Sales July 2024: To Get by with a Little Help from My Feds? 8-25-24

Payroll: A Little Context Music 8-22-24

All the President’s Stocks 8-21-24

CPI July 2024: The Fall Campaign Begins 8-14-24

Total Return Quilt: Annual Lookback to 2008 8-14-24