Mini Market Lookback: Burners on Full 10-27-24

We look at a subset of market metrics from the past week as tariff talk and political acrimony are overheating.

Fat Man with Little Boy brain has a plan: Let’s nuke global trade…

The week had a very rough ride with 30 of the 32 benchmarks and ETFs that we watch landing in negative return range, and the only two positive lines were less than +1%.

UST rates took a hit as stocks sold off (9 of 11 S&P 500 sectors in the red), bond duration was again negative, and more aggressive rhetoric on tariffs still was coming out daily and making more than a few investors nervous given the tone.

Excuse the metaphor of a “trade nuke” above, but the apparent ego and pride in repeated actual misstatements on “who pays” the tariff is disturbing given the ability to execute from the White House to the exclusion of Congress (see Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24, Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24).

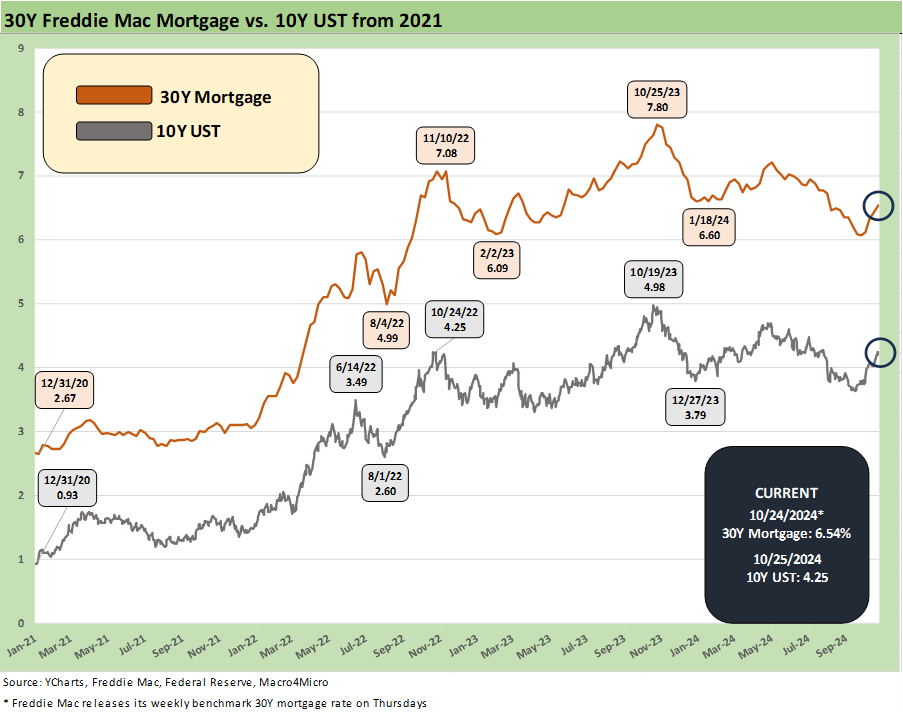

The adverse UST shift has sent 30Y mortgage rates back up closer to the 7% line in the broader market even if only in the 6% mid-range using the Freddie Mac 30Y benchmark.

Given the wide array of cyclically diverse bellwethers who reported earnings last week, the headlines saw a mix of good, bad, and ugly with 5 of the Mag 7 reporting earnings this coming week along with JOLTs, 3Q24 advance GDP, the Employment Cost Index, Personal Income & Outlays (PCE price index), and payroll.

The above chart shows a relatively bleak positive vs. negative score of 2-30 across our 32 benchmarks and ETFs. All the bond ETFs are modestly negative, but some interest rate sensitive sectors that had been rallying to bullish valuation levels took a bigger blow on the week as we see with Homebuilders (XHB), Financials (XLF), and Regional Banks (KRE).

We will dig into more time horizons in our broader Footnotes publication on asset returns, but the Homebuilder ETF (XHB) certainly jumps off the page above at -7.2% with rates higher and despite some respectable earnings reports (see New Home Sales: All About the Rates 10-25-24, PulteGroup 3Q24: Pushing through Rate Challenges 10-23-24). The existing home sales sector is the one with more problems at the macro level with mortgage rates going the wrong way again (see Existing Home Sales Sept 2024: Weakening Volumes, Rate Trends Worse 10-23-24).

In the bottom quartile, we see some valuation anxiety, industrial worries, and interest rate nerves with Materials (XLB), the small cap Russell 2000 (RUT), Midcaps (MDY), Industrials (XLI), Regional Banks (KRE) and Financials (XLF) taking a breather in the weekly bottom quartile.

The cycle is looking steady and solid (thus the rate debate) but the overlap with the valuation debate is going to make for some noise. The tariff plan as “proposed” (as little conceptional thought and specifics that exist) will crush some industries and companies and will escalate trade battles and adverse handicapping in rates.

The week gave the market a fresh reminder that the post-earnings hope for a uniform, downward shift is not playing out and would need much lower inflation or cyclical setbacks to get there. The parallel downshift curve rally idea was a big ask. Such bullishness is downright unrealistic at such low absolute rates in multicycle context when looking back at periods outside the post-crisis and COVID ZIRP years. We will be looking in more detail at the UST curve in our full Footnotes publication to be posted separately.

The tech markets cleared a low bar for good news this week with the NASDAQ positive (intraday all time high on Friday). We line up the tech bellwether returns for the week above in descending order of total returns. We also include a range of other trailing time horizon returns as noted. The bellwethers include the Mag 7 + Taiwan Semi and Broadcom and we include the broad market benchmarks (NASDAQ, S&P 500) as well as the Equal Weight S&P 500 (RSP) and Equal Weight NASDAQ 100 (QQEW).

As detailed above, we see 4 of the Mag 7 in positive range, but 3 in negative range. Tesla was the banner headline with a 22% return on the week. TSLA was thus able to get its total return YTD back up to +8.3%. TSLA still sits at the bottom of the Mag 7 return list YTD and is the only Mag 7 name in single-digit total returns YTD and the only one negative looking back 3 years.

While headline tech had a better week vs. other stocks, the Equal Weight NASDAQ 100 ETF (QQEW) was in the red (-0.7%) and has underperformed the Equal Weight S&P 500 (RSP) YTD and for the trailing 1 year.

The above chart updates the running Freddie 30Y Mortgage benchmark and the 10Y UST bond that is the key driver of long mortgage rates. We start the timeline at the end of 2020 during the ZIRP period and just as the COVID vaccine was getting rolled into the markets.

The 10Y UST is certainly a very long walk from the sub-1% yield days of the ZIRP but down notably from the 10-19-23 peak rate when the Freddie benchmark was getting close to 8% and numerous mortgage loan providers were above 8%.

The post-FOMC easing move higher of the 10Y UST from the 3.6% area has been a rude awakening on steepening risks out the curve. For those seeking an escape pod from the realities of supply and demand for UST bonds, global interest in UST and the direction of the dollar, the tone of the political discourse since the Sept FOMC easing has only made the situation worse (see FOMC Action: Preemptive Strike for Payroll? 9-18-24).

As we have covered in our housing sector research and single name work on the builders, the creative use of incentives by the large builders with their captive mortgage and financial services units have allowed builders to push right through the 7% handle rates in 2023. The builders can deal with this market and its favorable demographic supply-demand profile. That does not mean to understate the broader housing sector challenge, which is enormous. Harris has a partial plan that needs infill on the hardest part (supply) while Trump thinks mass deportation and his version of lebensraum will cure all ills. The foundation of Trump’s residential real estate plan is essentially nonexistent.

Both Trump and Harris cite plans to ease state and local regulations. Those views lack specifics, but the actual recommendations can just as easily be lifted off the NAHB home page. Nothing original there on regulation reform but that process needs to get in play immediately. Builders and the private sector working closely with Washington need to be a reality to address supply, or it is all talk.

That UST supply challenge will not go away…

The direction of US sovereign debt health is getting scarier in the threats to the deficit and the feeling of unlimited supply growth. The waves of forecasts from economists have been telling a story of “facts and concepts” that are often hard to stumble across in partisan discussions. Political philosophers always flag the death of reality (even beyond just “facts”) on the way to destroying resistance to power seekers. This will spill into serious trade conflicts with the short list of 4 (EU, Mexico, Canada, China) comprising 60% of total trade.

We cite those moving parts of tariffs in this UST and mortgage section not simply to rail on Trump as an economic ignoramus but also to highlight what that will mean for UST demand set against record funding needs. The possible elimination of income taxes and a substitution of tariffs has been a frequent topic. This is not an outlier idea. The “BAT tax” pitch by Ryan and Brady had many of the same “conceptual underpinnings” (the term “conceptual” is generous). The market is facing a debt ceiling test in January to add to the drama of drumming up demand.

The spit-balling around tariffs runs from 10% to 20% for blanket tariffs and then moved up to “maybe 50%” in Trump’s discourse. He apparently did not get the memo that companies can trim capex, retrench, and jack prices up if supply-demand trends get distorted. He also dropped some 100% and 300% punitive tariff threats for those that fight him. He did ring up a 2,000% number also all the while putting in writing on social media that the “abusing country pays” (e.g. China) and not the American consumer.

The above chart updates a very quiet week in spreads with IG OAS +2 bps wider on the week and HY OAS +1 bps wider. As we have covered in earlier commentaries, risk pricing will have a lot more to digest when the lineup of the White House and the Congress gets set. The big difference for a set of economic policies tied to tariffs (i.e. Trump) is that only the White House is required. That raises questions of applications for exemptions with the White House as sole decider with unchecked leverage and powerful economic and partisan interests. Very Putin-esque.

For the broader budget issues, the tax cut extension also factors into the budget and borrowing math and how that rolls into the UST supply-demand math and dollar forecasts. If the curve does not rally and the budget deficit explodes, the interest cost line is only going one way…higher.

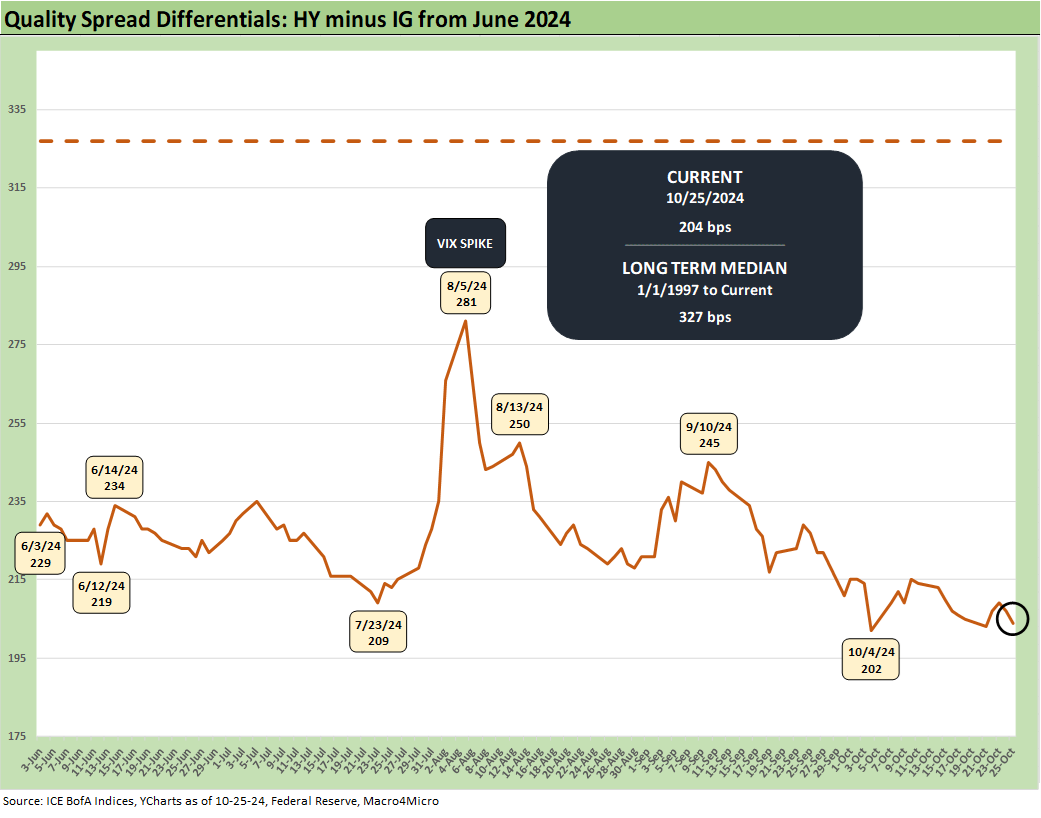

The above chart updates the “HY OAS minus IG OAS” quality spread differentials at +204 bps, or flattish to last week’s +205 bps. The differential still signals credit compensation as down at very low levels vs. the long-term median of +327 bps.

The above chart updates the “BB OAS – BBB OAS” differential for a read along the speculative grade divide. That spread gap is only +72 bps as it barely moved from last week’s +73 bps. The current level is well inside the long-term median of +135 bps and comfortably wide to the recent lows of +55 bps in July 2024.

See also:

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Durable Goods Sept 2024: Taking a Breather 10-25-24

New Home Sales: All About the Rates 10-25-24

PulteGroup 3Q24: Pushing through Rate Challenges 10-23-24

Existing Home Sales Sept 2024: Weakening Volumes, Rate Trends Worse 10-23-24

State Unemployment Rates: Reality Update 10-22-24

Footnotes & Flashbacks: Credit Markets 10-21-24

Footnotes & Flashbacks: State of Yields 10-21-24

Footnotes & Flashbacks: Asset Returns 10-20-24

Mini Market Lookback: Banks Deliver, Equities Feel the Joy 10-19-24

Housing Starts Sept 2024: Long Game Meets Long Rates 10-18-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Retail Sales Sep 2024: Taking the Helm on PCE? 10-17-24

Industrial Production: Capacity Utilization Soft, Comparability Impaired 10-17-24

CPI Sept 2024: Warm Blooded, Not Hot 10-10-24

HY OAS Lows Memory Lane: 2024, 2007, and 1997 10-8-24