CPI Dec 2024: Mixed = Relief These Days

Absence of bad news can sometimes be a good enough day with the real test to the trend still tied to the massive policy shifts ahead.

The CPI report was mixed with headline YoY up sequentially to 2.9% from 2.7% but core still at 3.2%. We see a muted MoM move of +0.2%, which is the lowest since July 2024.

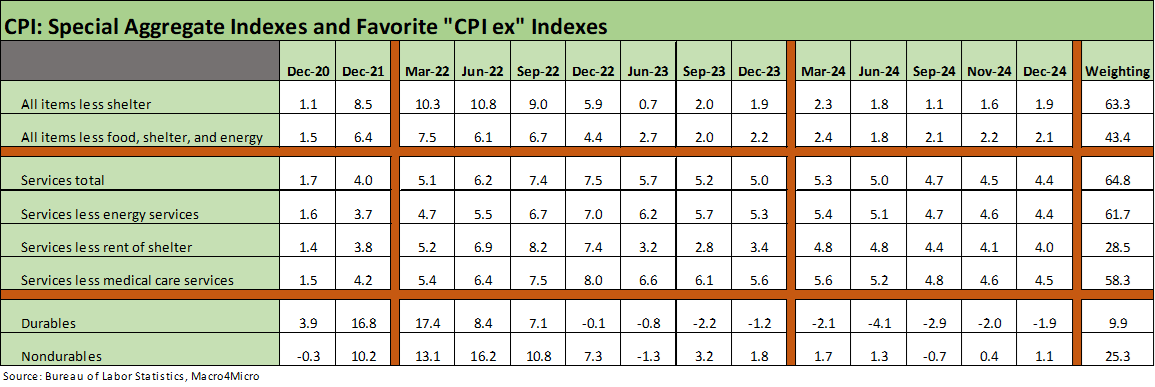

Services remain a headache with all Services at +4.4%, Services less Energy at +4.4% (61.7% of CPI index), Services less Rent of Shelter at +4.0%.

“All items less shelter” at +1.9% (63.3% of CPI index) always helps ease the worst of inflation tensions with Shelter the usual story at +4.6% with MoM trends flat at +0.3% vs. Nov and a tick below the +0.4% in Oct. Owners’ Equivalent rent posted +4.8% at 27.2% of the CPI index.

The needle seems to be moving around on FOMC expectations for 2025 timing, and the worry needle could turn into spikes soon on tariffs and labor risks. The deportation issues could flow into Shelter costs in homebuilding subcontractor constraints and undermine the price and supply variables at a time of massive rebuilding needs after the weather and fire calamities (see KB Home 4Q24: Strong Finish Despite Mortgage Rates 1-14-25).

The chart shows trend lines for some of the Special Aggregate Lines the BLS breaks out each month. These aggregates offer a few more prisms to look through.

The intrinsically strange nature of how shelter is measured vs. the household cash-in, cash-out rates of households always puts an asterisk on measures such as Owners’ Equivalent Rent. We have covered that enough in the past, but such quirks make All items less shelter a good one to at least look at. At +1.9%, this measure is low in absolute terms, but we also see a sequential rise on the YoY metric from 1.6% last month.

In a Services economy, a few more angles on Services CPI is helpful. Total Services YoY is down sequentially from 4.5% to 4.4% and Services less energy YoY is down sequentially from 4.6% to 4.4%. The same is true for Services less rent of shelter to 4.0% from 4.1% and Services less medical care services to 4.5% from 4.6%. It is not much to lean on with so many 4% handles, but it all counts.

The above chart updates the Big 5 categories we look at each month including our own version of Automotive (see Automotive Inflation: More than Meets the Eye10-17-22), which is a far more important part of household budgets than many think about given how many line items are impacted (even without considering gasoline).

The lines across time pretty much tell their own story as we have updated along the way. Vehicles are in deflation mode but that comes with a qualifier around the high absolute financing costs in the markets. Insurance had gained a lot of headlines in 2023-2024 and remain brutal.

Medical care services ticked lower sequentially for YoY, but that topic will loom large considering what could unfold for the household sector in any attacks on Obamacare and/or retrenchment in Medicare and Medicaid. That is where the impact of inflation ends and the actual coverage of any sort weighs in for many households.

The Energy lines are likely to remain volatile in 2025 subject to some major questions on tariffs (i.e. tariffs on Canadian crude oil imports) Headline energy sector deflation for YoY comes with the reality of a Dec 2024 MoM number of +2.6% on Total Energy and +4.4% MoM for Gasoline. As we all know, energy lines can move very quickly and reverberate across the system in raw material costs, heating costs, etc., that can be reflected in goods and services pricing, transport costs, etc.

The above chart wraps up the monthly CPI moves with some line items near and dear to many households. The biggest sequential move was airline fares. In the rest, we see a mix of minor moves higher and lower. Internet was deflating but deflating by less. Recreation services dropped off YoY and is now much lower than 2022-2023.

See also:

Inflation Related:

Payroll % Additions: Carter vs. Trump vs. Biden…just for fun 1-8-25

JOLTS: A Strong Handoff 1-7-25

PCE, Income & Outlays Nov 2024: No Surprise, Little Relief 12-20-24

Fed Day: Now That’s a Knife 12-18-24

Inflation: The Grocery Price Thing vs. Energy 12-16-24

CPI Nov 2024: Steady, Not Helpful 12-11-24

Payroll Nov 2024: So Much for the Depression 12-6-24

Trade: Oct 2024 Flows, Tariff Countdown 12-5-24

Mexico: Tariffs as the Economic Alamo 11-26-24

Tariff: Target Updates – Canada 11-26-24

The Inflation Explanation: The Easiest Answer 11-8-24

Tariffs: The EU Meets the New World…Again…Maybe 10-29-24

Trump, Trade, and Tariffs: Northern Exposure, Canada Risk 10-25-24

Trump at Economic Club of Chicago: Thoughts on Autos 10-17-24

Inflation Timelines: Cyclical Histories, Key CPI Buckets11-20-23