Retail Sales: Third Wind?

We look at the latest round of strong retail sales that in theory provide more flexibility for a slower FOMC approach on the scale of cuts.

FOMC Working Group on Rates… Feel the Cuts, Be the Cuts

Other than inflation metrics, no single or double set of numbers wag the Fed ‘s decisions, but Retail Sales get a lot of focus from the market and FOMC with the 2Y to 10Y UST up by double digit bps as we go to print.

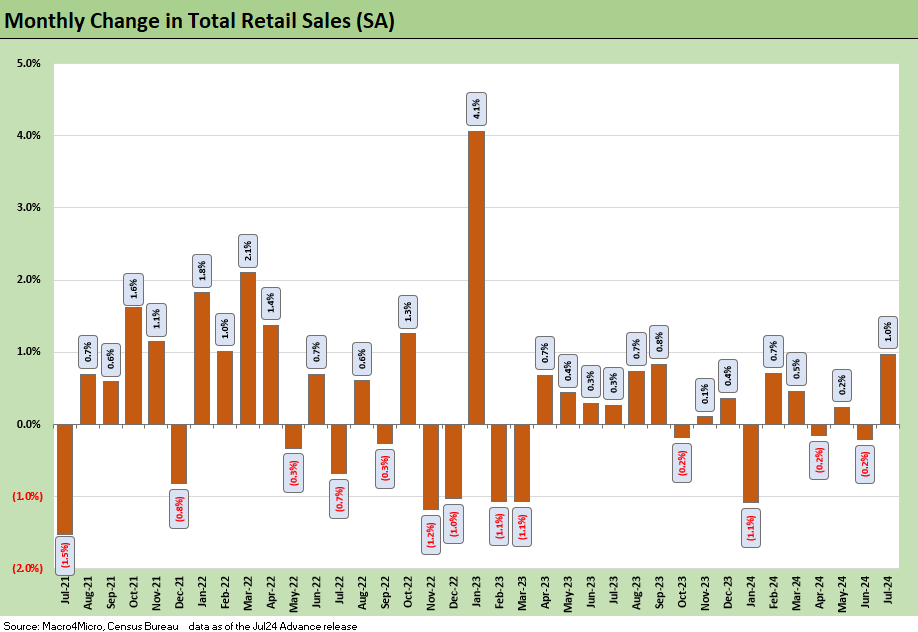

Retail sales for July came in above expectations this month at +1.0% with Autos making a big comeback for the month after a mediocre June print.

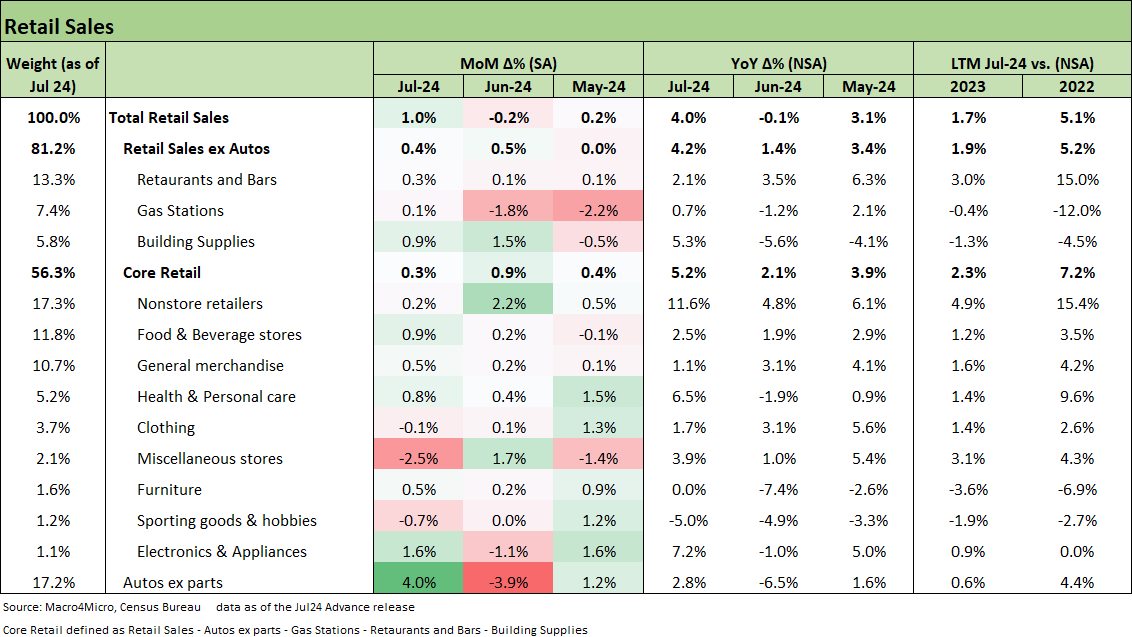

The core retail goods data stayed positive, though not as strong as last month, and the overall recent trend signals a consumer that is still healthy despite some warning signs from other consumer data and credit card quality data.

After yesterday’s CPI print with headline inflation finally at a 2-handle and a consumer not in dire straits (yet), the addition of today’s Retail Sales provides more cover for the Fed to push back on calls for -50 bps cuts but enough room to justify their eventual decision subject to next set of PCE inflation data and with employment.

Retail sales growth this month reached their highest level in a year and a half, since January 2023 saw over 4.0% growth. This strong performance comes on the heels of a period marked by weak consumer sentiment and rising delinquencies, which had raised concerns about consumer health. The heavy concentration of growth from Autos spending underlying the strong reading today is noteworthy, pointing towards where there is appetite to take on financing in today’s rate environment. In theory the rate environment for consumer durables will be better in the fall and not 2025.

Whether this reflects well thought-out budgeting decisions at the household level or some blind optimism remains to be seen. We again heard replays this morning of “never bet against the US consumer.” That said, the credit card loan reserve policies better be up to the challenge. At the rates being charged, even high reserves leave plenty of room for profitable lending. That said, beware the excess from some consumer lenders.

Breaking down the headline retail sales reveals the significant impact of auto sales growth this month. The swing factor for the +1.0% MoM headline increase, compared to the -0.2% in the prior period, largely comes down to the auto sales line, as the "ex-Autos" lines were almost flat at +0.4% and +0.5%, respectively. This marks two consecutive months of solid pushback against consumer softening narratives.

Core retail cooled off this month but still posted a respectable +0.3% MoM growth. Online shopping (Nonstore retailers) saw minimal growth this month, but the meteoric growth over the past year has left this line 11.6% higher than the same time last year (NSA). The next largest components of core retail (Food & Beverage, General Merchandise, Health & Personal Care) remain solidly in the green.

Overall, the importance of retail sales this month is the absence of bad news and the ability for the Fed to maneuver without a looming specter of imminent PCE slow-down or a sharp contraction in payrolls. The equity markets are rallying sharply today as we go to print the UST curve seeing rates jump. There is a lot of year left and the stakes are rising with so many risks still left to play out.

See also:

CPI July 2024: The Fall Campaign Begins 8-14-24

Footnotes & Flashbacks: Credit Markets 8-12-24

Footnotes & Flashbacks: State of Yields 8-11-24

Footnotes & Flashbacks: Asset Returns 8-11-24

HY Industry Mix: Damage Report 8-7-24

Volatility and the VIX Vapors: A Lookback from 1997 8-6-24

Footnotes & Flashbacks: Credit Markets 8-5-24

Footnotes & Flashbacks: State of Yields 8-4-24

Footnotes & Flashbacks: Asset Returns 8-4-24

HY Pain: A 2018 Lookback to Ponder 8-3-24

Payroll July 2024: Ready, Set, Don’t Panic 8-2-24

Employment Cost Index: June 2024 8-1-24

JOLTS June 2024: Countdown to FOMC, Ticking Clock to Mass Deportation 7-30-24

Footnotes & Flashbacks: Credit Markets 7-29-24

Presidential GDP Dance Off: Clinton vs. Trump 7-27-24

Presidential GDP Dance Off: Reagan vs. Trump 7-27-24

2Q24 GDP: Into the Investment Weeds 7-25-24

GDP 2Q24: Banking a Strong Quarter for Election Season 7-25-24

|

|

8 out of 9 months get negative adjustments...certainly helps July after June adjusted lower but agree the 1% number looked good...will be very interested to see August once July gets adjusted...especially with alot of mentions about a more careful consumer in 2Q results