Retail Sales Apr 2024: Get By With a Little Help

Flat retail sales in tandem with a softer CPI gives more hope for FOMC support as risk and rates rally.

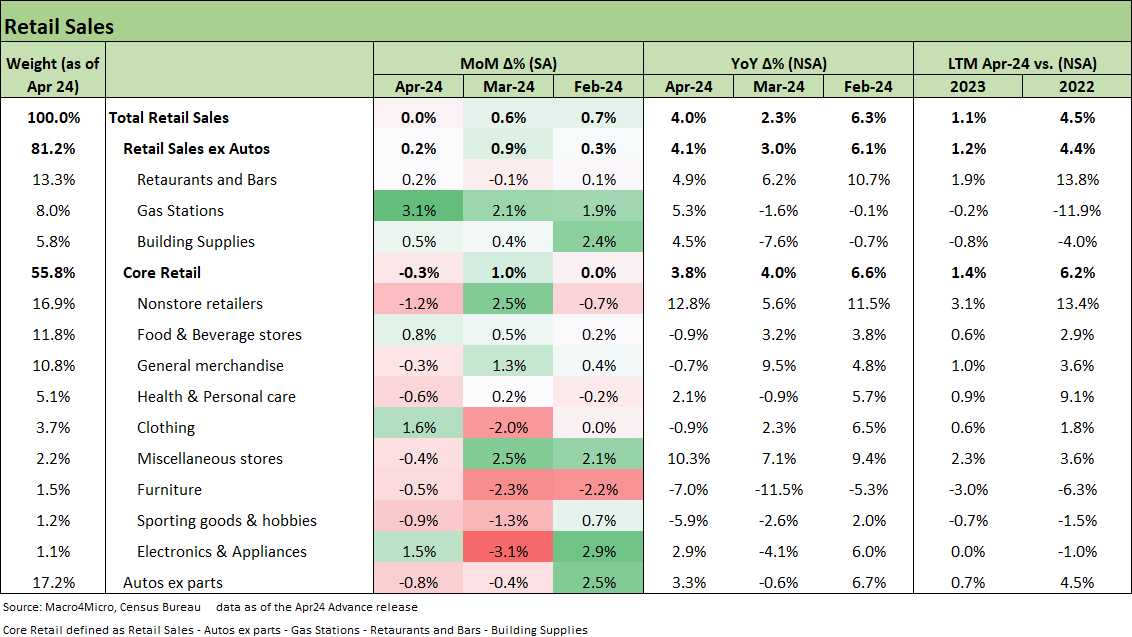

Higher gas prices pulled headline retail sales to flat on the month with a negative print for core retail sales.

After another rise in credit card and auto loan delinquency rates for 1Q24, there may not be cracks just yet but at least consumers are potentially signaling a slowdown.

Consumers are still spending at restaurants and bars and the weak online sales weighed down the month following a very strong March print.

A cooler inflation print with some mixed consumer signals gives some ammo to UST bulls as the UST pushed lower today (see CPI April 2024: Salve Without Salvation 5-15-24).

The Retail Sales release comes in flat and below consensus with downward revisions changing the landscape of the year to one with little net increase since December. The recent history of retail sales has been positive with swings for a consumer sector that has remained steady in the higher rate environment. Recent discussions around savings depletion and overreaching on spending means that increasing delinquencies and a soft retail sales number provides ammo for those more bearish on consumer health.

As detailed further below, the line items are not decidedly negative even with a -0.3% core retail print. The market will shift over to Industrial Production and housing data tomorrow, but we do not have another major consumer-focused round of data until the second estimate on 1Q24 GDP and PCE (Income & Outlays, PCE inflation) at the end of the month.

The above chart breaks out the line items underlying an argument for a better view of the consumer than first glance. Restaurants and bars are still growing this month, even if just at +0.2%. That is a discretionary spending area that would be expected to be an early one to pull back. The growth this month sits within a larger context of 5.5% YoY increase (NSA) vs. last April in a category that has fared well in recent times.

The standout line item in the core retail section is Nonstore retailers (i.e. online retailers) where the growth trend has been very strong and weakness this month could be attributed to a pull-forward of spending leading to a very strong March print.

Both Autos ex-parts and Gas Stations look eerily similar to this morning’s CPI print with gasoline up 2.8% and, new vehicles down -0.4% and used cars and trucks down -1.4%. The connection cannot be ignored since retail sales are reported nominally.

Despite some line items giving a rosier picture of the consumer, this month’s print is still soft and does not provide decisive enough data for a strong vote. It is good enough for both credit and equity markets alike today. The S&P 500 hit a record high as we go to print (NASDAQ +1.3%) and the UST 10Y was in by over -8bps with the 5Y UST almost -10 bps. Homebuilder equities were rallying materially on the news.

See also:

CPI April 2024: Salve Without Salvation 5-15-24

Footnotes & Flashbacks: State of Yields 5-12-24

Footnotes & Flashbacks: Asset Returns 5-12-24

Consumer Sentiment: Flesh Wound? 5-10-24

April Payroll: Occupational Breakdown 5-3-24

Payroll April 2024: Market Dons the Rally Hat 5-3-24

JOLTS March 2024: Slower Lane, Not a Breakdown 5-1-24

Employment Cost Index March 2024: Sticky is as Sticky Does 4-30-24

PCE, Income, and Outlays: The Challenge of Constructive 4-26-24

1Q24 GDP: Too Much Drama 4-25-24

1Q24 GDP: Looking into the Investment Layers 4-25-24

Durable Goods: Back to Business as Usual? 4-24-24

Systemic Corporate and Consumer Debt Metrics: Z.1 Update 4-22-24

|

|