Existing Home Sales May 2026: Slow Rise Despite Rates

A mild recovery in existing home sales was good news considering the latest inflation headwinds in CPI and PPI.

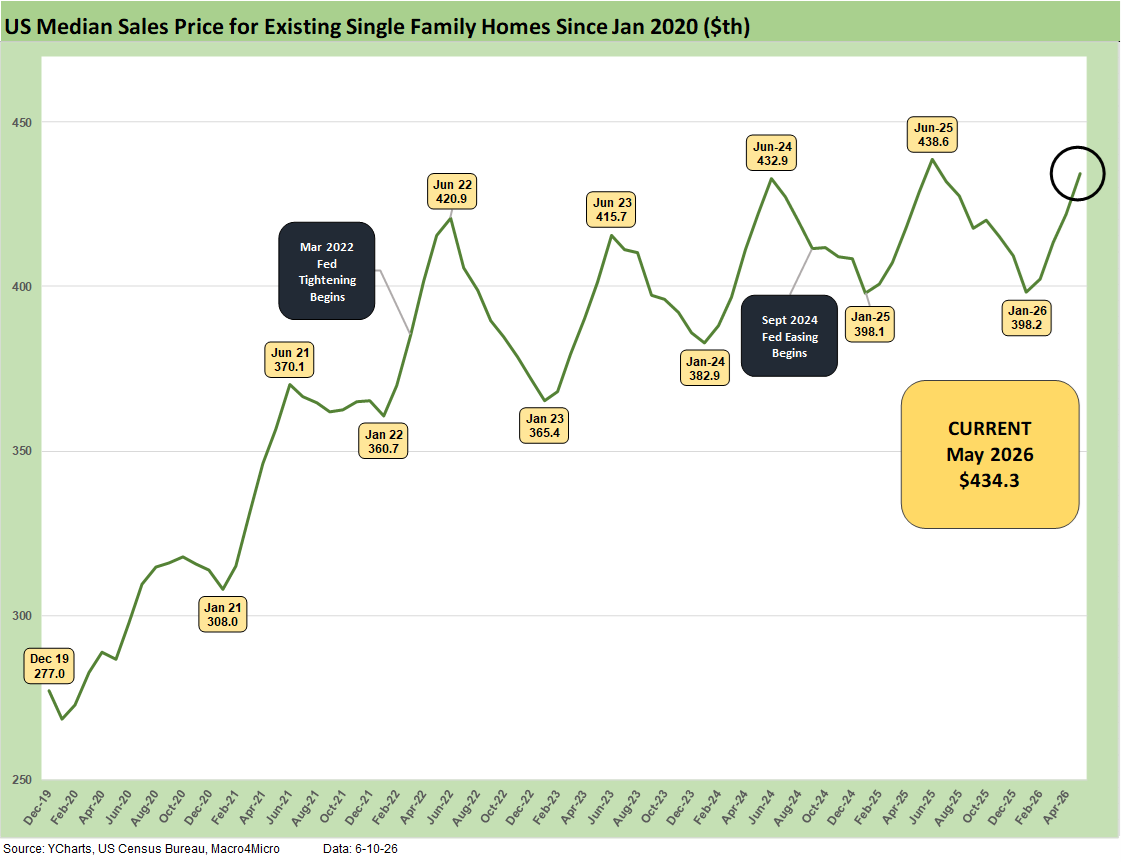

The spring season is bringing modest increases for May MoM and YoY. Inventory rose and median prices were higher YoY at $429.3K for total existing home sales and $434.3K for single family. The NAR cites improved YoY affordability indexes across all four regions.

The UST curve has not been friendly at around 6.6% mortgage rates, and curve dynamics are still working against lower rates with odds heavily favoring 1 hike or no action with negligible odds of easing at this point. More oil price increases or inflation pressure in a US-Iran escalation would put further upward pressure on longer rates and mortgages.

As we go to print, Trump says a deal is done, but that has become a punchline at this point. If it happens there could be some mortgage relief. The debates among industry experts on the lingering effects in the physical markets even with a “real truce” and open Strait are on balance still flagging a lot of oil and refined product price risk into the summer.

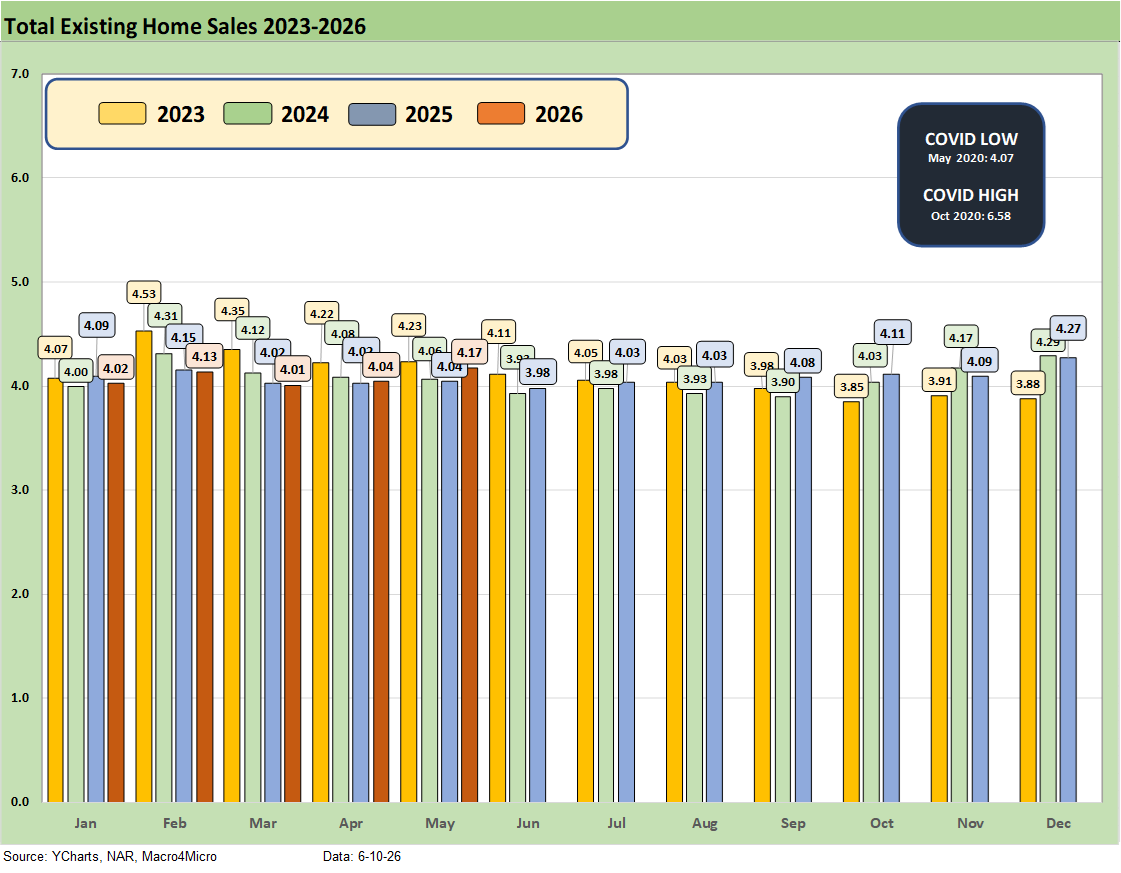

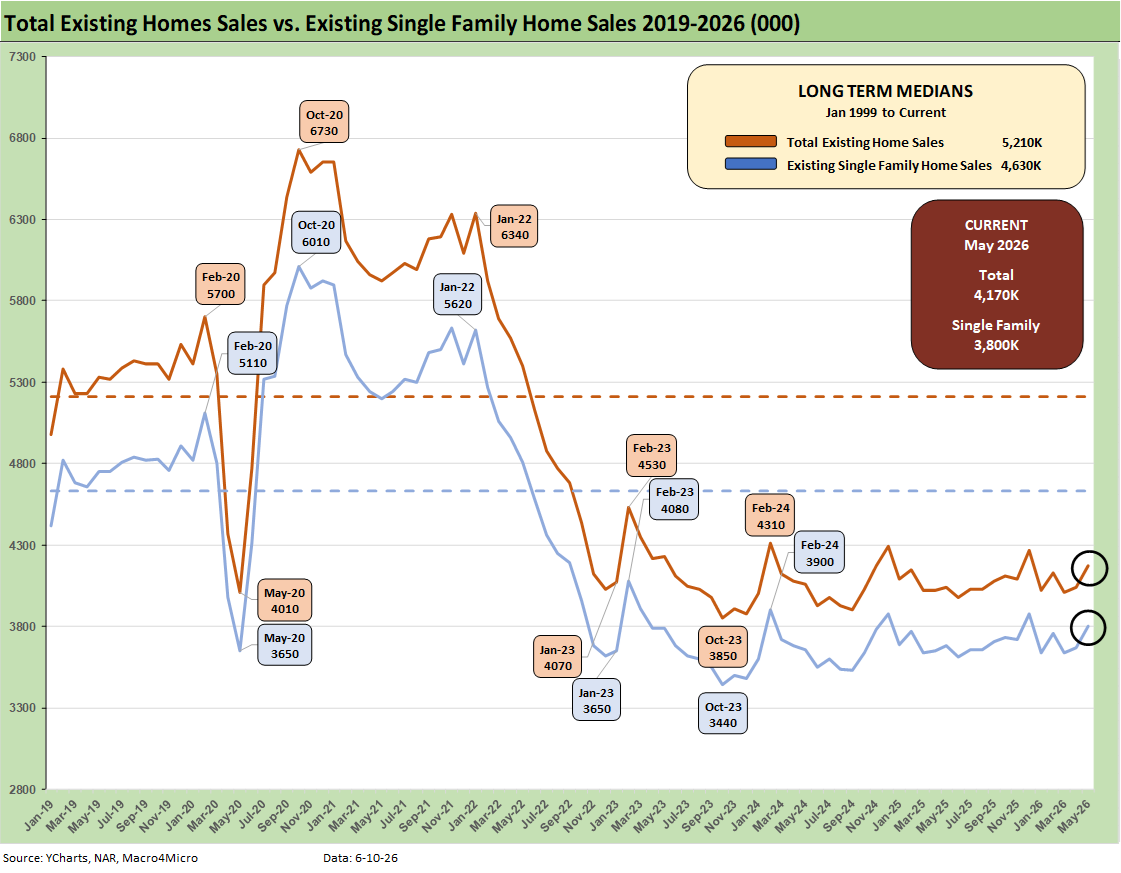

The above chart details existing home sales SAAR run rates by month from January 2023 to May 2026 at 4.17 million, up from 4.04 million. As a frame of reference, in 2022 market was posting 6 million and 5 million handle sales volumes in the first half of that year.

The early read on peak selling season ahead is off to a guarded start with mid-6% handle 30Y mortgage rates remaining a headwind, and the consumer sector shaky and less confident this year than last spring as inflation and payroll anxiety remain factors in 2026.

The recent numbers look more like the late 2023 period when mortgages had peaked (see Existing Home Sales Dec 2023: Rerun of Multi-Decade Low 1-19-24). The 30Y mortgage rates have moved within a 200 bps range since the Oct 2023 peak when Freddie Mac 30Y hit 7.8% and many mortgage offerings were near 8%.

The modest move in existing home sales is set against a fairly grim set of numbers from the CPI and PPI releases (see Producer Price Index May 2026: Too Many “Since 2022” References 6-11-26, CPI May 2026: The 4% Rubicon 6-10-26). The PPI and CPI headline inflation numbers spell back-to-back trouble even if the markets are not reacting much to the sustained evidence of rising inflation. The new Fed Chair will be somewhat hamstrung by economic reality and the need to convince a committee in the voting process.

The inflation metrics and Iran War fallout remain critical to the consumer story line with savings rates plunging to 2Q22 levels. We see consumers continuing to “show up” as framed in the monthly income and outlays reports (see PCE Inflation: Income and Outlays April 2026 5-28-26), but consumers remain vulnerable as evident in credit card quality metrics and balance trends.

PCE growth rates in the GDP accounts comprise 68% of GDP, and that PCE line has clearly slowed down in the 1Q26 GDP reports at 1.4% in the 2nd estimate GDP (see GDP 1Q26 Second Estimate: Shrunk in the Dryer 5-28-26). That is weaker, but it is not a contraction.

Trying to handicap UST levels and shapeshifting has been a challenge when we started the year with a lot of focus on easing and the new FOMC regime. Mortgage rates have been a headwind, and gauging what the FOMC might do is important even if the 10Y UST is what drives mortgage rates.

The odds as shown in the FedWatch CME models frame the odds of a single fed fund easing by the FOMC Dec 2026 meeting as well below 1%. By Thursday evening, the odds of 3 hikes (2.9%) are higher than the odds of 1 cut (0.6%). The high odds FOMC scenarios point at 1 hike (42.9%) or no change at 40.2% and 2 hikes at 14.4%. These odds whip around with Iran headlines and inflation and payroll releases.

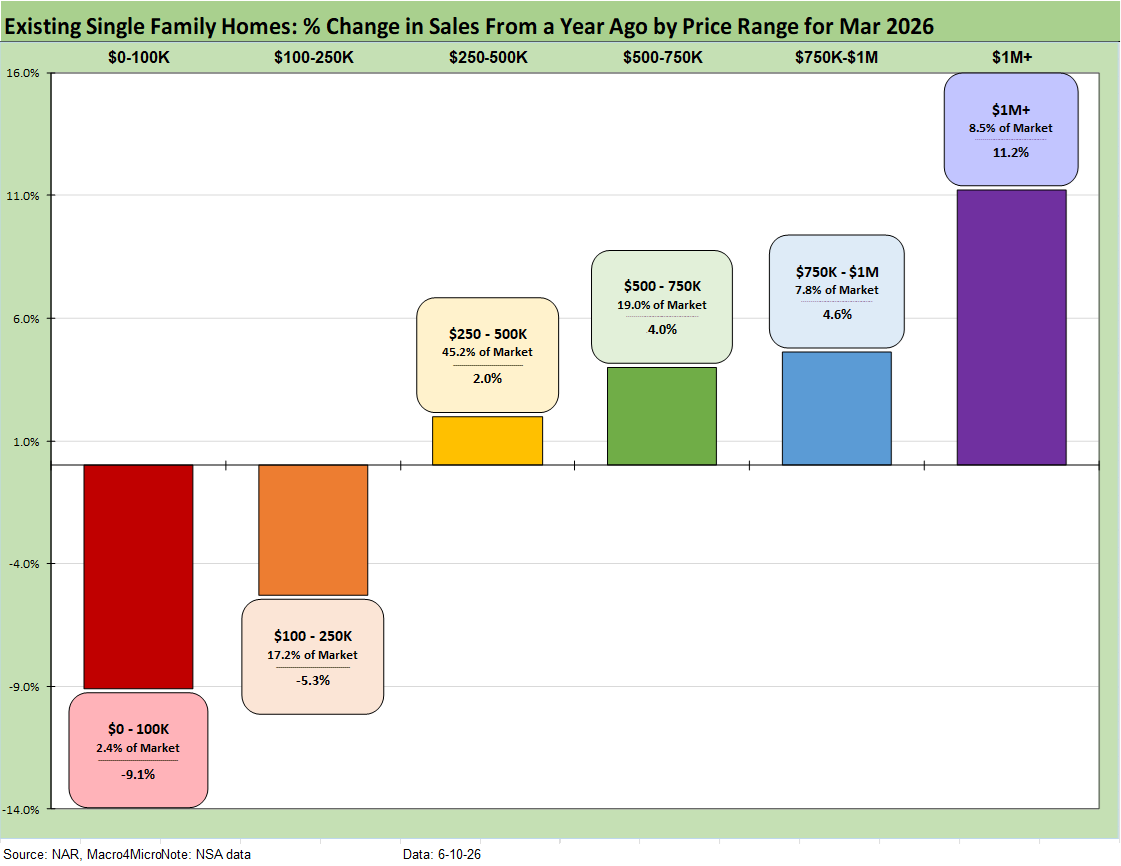

The above chart shows the sales volume delta by price tier for May 2026, and we see 4 of the 6 price tiers posting positive growth with only the two lowest price tiers posting declines. That was the same mix of deltas as last month. Note: We use “not seasonally adjusted data” for this chart.

For existing home sales, the monthly payment math is still not working well for those looking to cash out, move up, or simply relocate. Expectations for a bull flattener in the UST market that would translate into low to mid 5% mortgage rates have been thwarted and are highly unlikely to resurface. It is a very challenging leap of faith to see any probability of the conditions for easing getting better from here given steady payrolls and rising inflation.

An easing would require a macro backdrop that hits payrolls and homebuyer confidence to make the FOMC move to ease. Such a move by the Fed could also drive a UST steepener subject to the underlying reasons used by the FOMC. The oil spike and price swings since Iran plus the documented inflation pressures will make life a challenge for Warsh. The years of “repricing of the household basket” under Biden and again under Trump has made life a struggle for many and now we are looking at negative real wage growth.

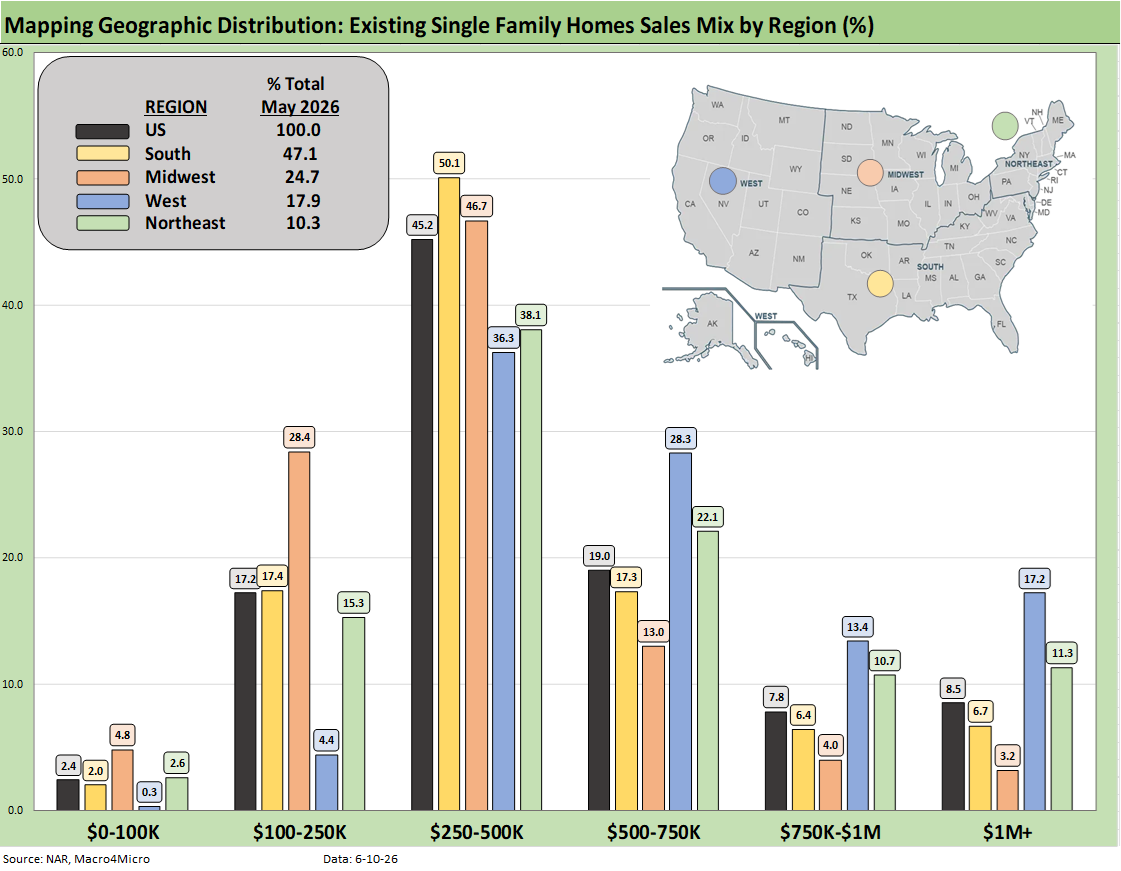

The above chart shows the geographic mix of volumes and details on price mix by region. The South is the main event in single family volumes whether new or existing at almost 47%.

For the bar chart, we break out the mix for each region by price tier. For example, the South shows around 50% of its existing home sales volume in the $250K to $500K range and over 17% of its sales in the $100K to $250K bucket.

The high cost of homes in the West (notably California) is clear enough just by glancing at the bar chart with over 17% at prices over $1 million. The second highest in the $1 million club is the Northeast at over 11%.

We see a major concentration across the regions in the $250K to $500K although the $100K to $250K bracket for the Midwest stands at over 28.4%. The West shows a high share of 28.3% in the $500 to $750K bracket, which again underscores how expensive the West region price tags remain in national context.

The map explains what states are in each Census region. There is a very wide range of home price profiles in the West and Midwest states.

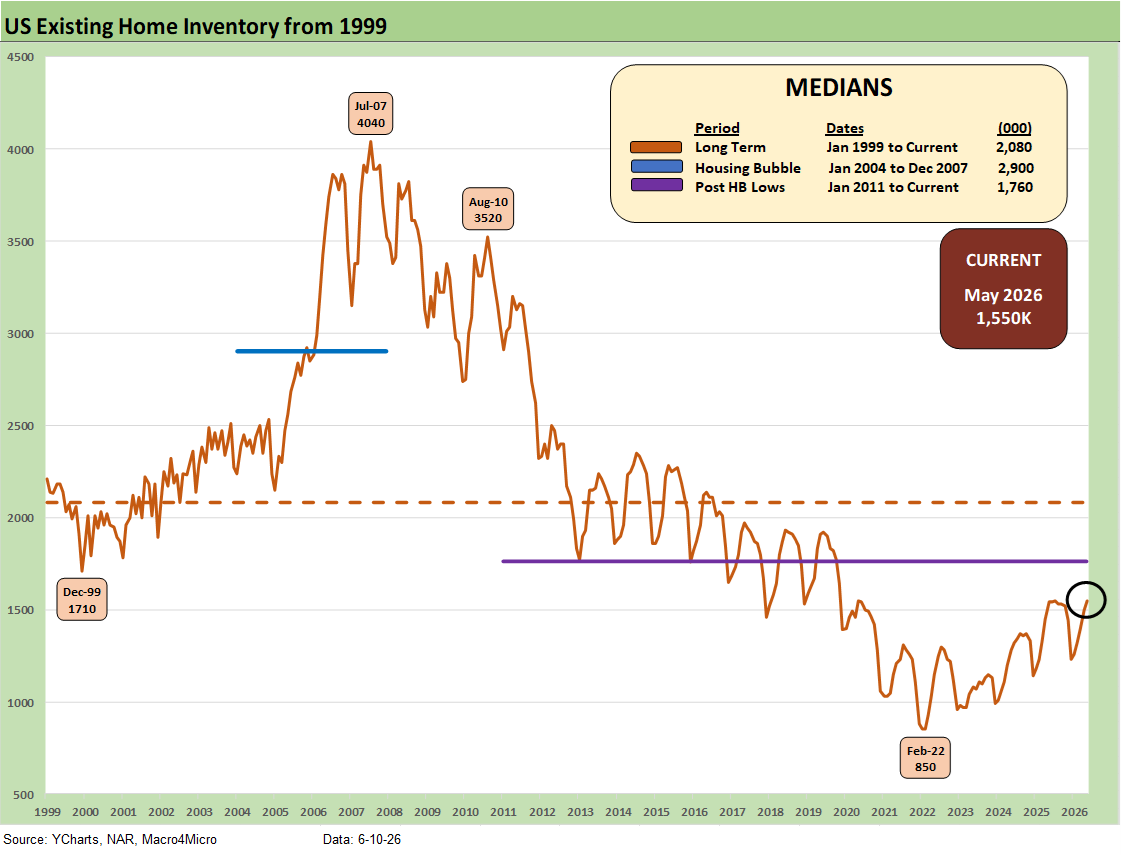

Inventory for total existing homes ticked higher MoM to 1.55 million units for +3.3% MoM and +0.6% higher YoY. Current inventory is well below longer term medians including 2.08 million for the post-1998 median. The median from Jan 2011 (homebuilding low) to current times is 1.76 million. In other words, existing home sales inventory remains low even if the level is materially higher than the stunning low of 850K of Feb 2022 ahead of the end of ZIRP and start of the tightening cycle in March 2022.

The existing home inventory balance had shown a steady rise off the sub-1 million lows of 2022. Inventory had risen to the 1.3 million handle range in 2024 before dipping back down to a recent low of 1.14 million to close out 2024. We bounced off those numbers in 2025 to get back above 1.5 million handles before the recent move lower to 1.2 and 1.3 million handles and then back to current levels above 1.5 million.

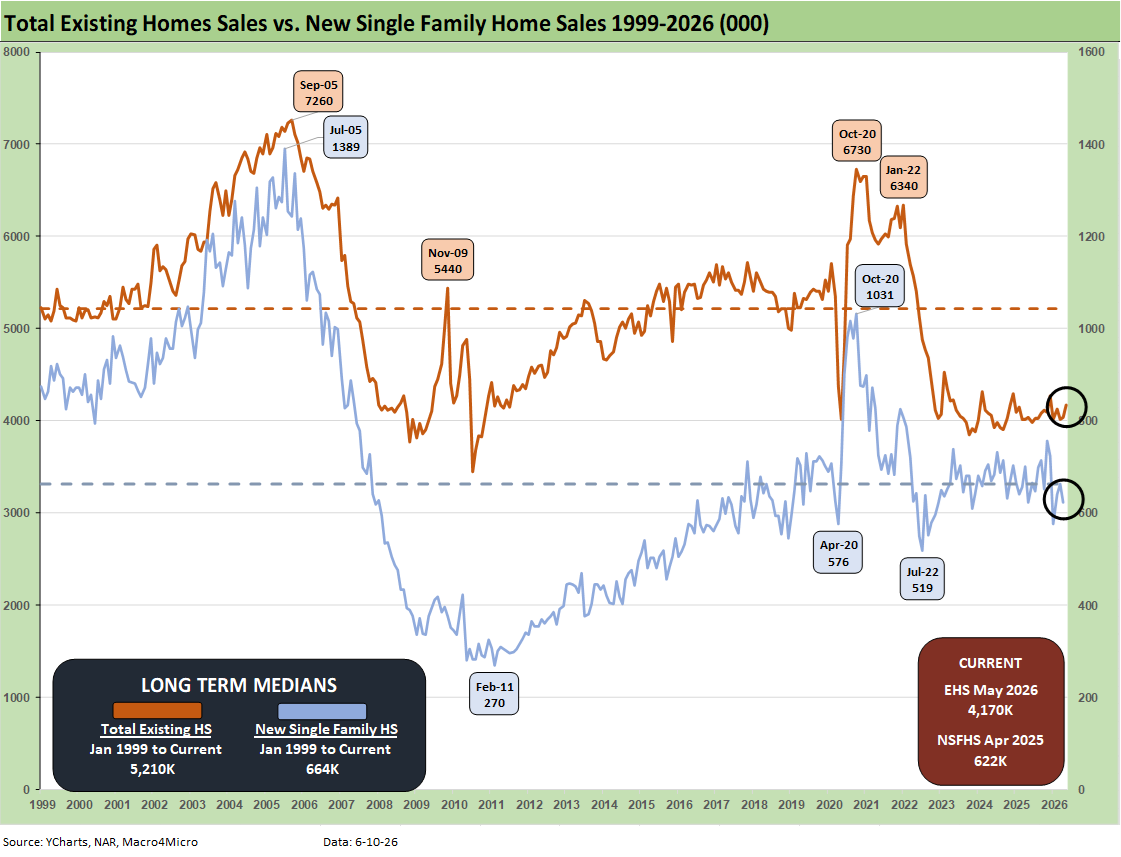

The above two-sided chart updates the trend line in total existing home sales vs. new single family homes. After some material disruptions in the data updates during the shutdown, the new home sales data is current again (see New Home Sales April 2026: Slow Start to Spring 5-28-26).

The above chart breaks out the timeline for existing single family only of 3.8 million vs. total existing home sales of 4.17 million. The 4.17 million total is well below the long-term median (from Jan 1999) of 5.21 million. The total of 3.8 million for single family is well below the long-term median of 4.63 million.

Existing single family growth was 3.5% sequentially and 3.3% YoY (SAAR). The lower line is ex-condo/ex-coops. We saw 370K in condo and coop sales in May 2026, up from 360K YoY and flat to 370K MoM.

The above chart updates the median price for existing single-family homes at $434.3K (vs. $429.3K total) after June 2025 hit a record $438.6K. The median price in May 2026 is dramatically above the $308K level back in Jan 2021 and $277K in Dec 2019 when mortgage rates were in a different zip code and closer to 3.7% for 30Y Freddie Mac.

The above chart shows another angle on the sales mix across the price tiers. We just lift the numbers off the monthly handout for single family homes released by the NAR each month. Higher price homes and wealthier buyers have had a better time across this cycle as the “K recovery” certainly applies in housing given the mortgage pressure on monthly payments.

The $250K to $750K range is comprised of two tiers that add up to almost 2/3 of the market with the $100K to $250K showing a big share in some of the Midwest states as detailed in an earlier chart. We also looked at the growth trends for each tier earlier. Lower price tiers declined while the top 4 tiers rose. The lower price tiers are more on the cusp of where affordability and mortgage eligibility could be strained at 6.6% area handle mortgage rates (today’s Mortgage News Daily survey).

See also:

Producer Price Index May 2026: Too Many “Since 2022” References 6-11-26

CPI May 2026: The 4% Rubicon 6-10-26

Market Commentary: Asset Returns 6-8-26

Remembering D-Day: June 6, 1944

Employment May 2026: Big Rebound, Low Multiplier Bias 6-5-26

The Fall of CBS 6-3-26

JOLTS April 2026: A Modestly Positive Turn 6-2-26

Retail Signal Read Part Deux 6-1-26

Market Commentary: Asset Returns 5-31-26

New Home Sales April 2026: Slow Start to Spring 5-28-26

PCE Inflation: Income and Outlays April 2026 5-28-26

GDP 1Q26 Second Estimate: Shrunk in the Dryer 5-28-26

Retail Equity Comps: Looking for Signals 5-26-26

Housing Starts April 2026: Soft Starts in Single Family 5-22-26

D.R. Horton: Financial Powerhouse Despite Cyclical Softening 5-20-26