GDP 1Q26 Second Estimate: Shrunk in the Dryer

A downward revision in GDP leaves the PCE line as the weak link in the GDP growth story with Fixed Investment soaring.

Fixed Investment looms large, but the imbalance with consumer growth remains.

A downward revision in GDP growth from 2.0% to 1.6% offers minimal bragging rights in the line item that is over 68% of GDP. The fixed investment line is a very different story with GPDI at +7.0% including +10.1% in Nonresidential investment. Government weighs in at +4.4%.

Residential remains under a cloud at -6.2% and offers a prism to view how interest rates dampen consumer big tickets on financing costs. Mortgage rates at a 6.6% handle are not helping. The FOMC easing story line and bull flattener theories are taking a beating unless the Iran situation gets to a more constructive conclusion. The 1Q26 headline PCE price index still weighed in at +4.5% while the Core PCE price index ticked slightly higher to +4.4% from +4.3%.

The Personal Consumption Expenditure line at +1.4% is weak in historical context with Goods at only +0.4% and Services at +1.8%. That is even with saving rates hitting post-2022 lows at 2.6% (vs. 3.2% in March and 4.3% to start the year in January). Savings rates are above the 2.2% lows of June 2022 and flat to the 2.6% in April and May of 2022.

Fixed asset investment is booming with Equipment at +17.2% and Intellectual Property Products at +11.6% partially offset by -5.4% on Structures and -6.2% on Residential.

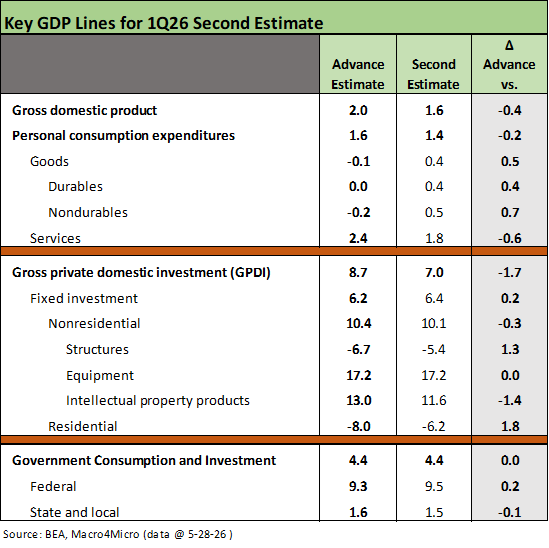

The above chart updates the GDP line item deltas to reflect the 2nd estimate for 1Q26. The main moves include a downward revision of Gross Private Domestic Investment (GPDI) from “extremely high” to “slightly less extremely high.” The negative growth in Residential was less negative. PCE was clipped by a material revision to the large Services line. Goods as revised higher, which was a positive signal considering tariffs.

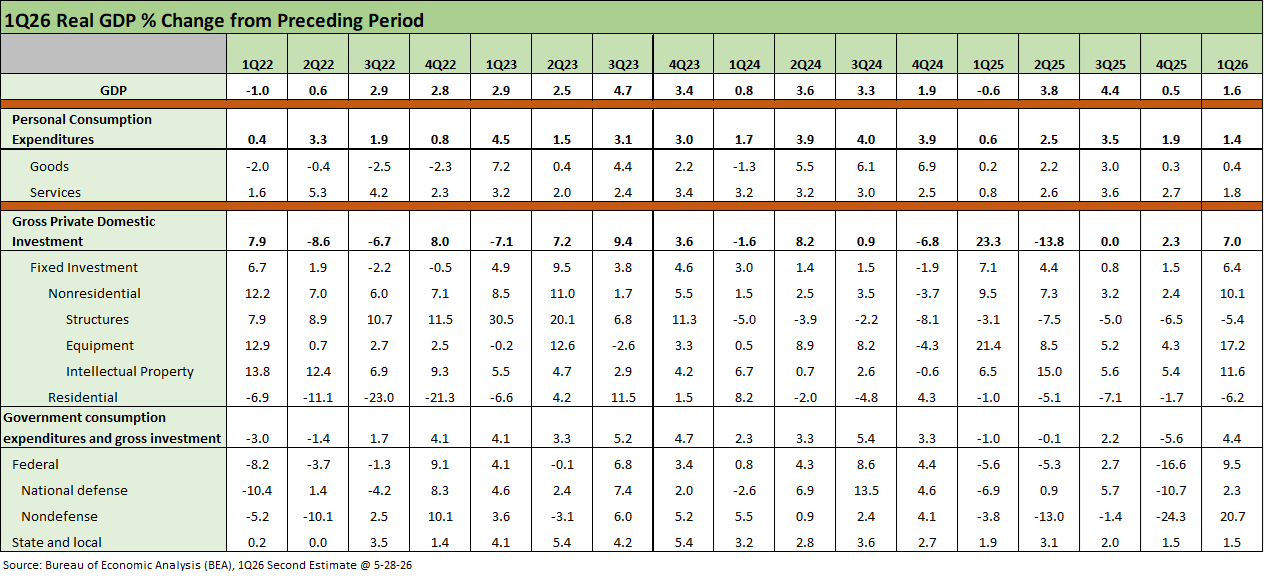

The above table updates the running GDP line items beginning in 1Q22 during the quarter when ZIRP ended, inflation was kicking into gear, and the tightening cycle got busy in the following quarters. The easing cycle started in 3Q24.

See also:

1Q26 GDP Advance Estimate: Consumer Fade, Investment Boom 4-30-26

4Q25 GDP: More Adverse Revisions in the Golden Year 4-9-26

3Q25 GDP: Morning After Variables to Ponder 12-27-25

2Q25 GDP Final Estimate: Big Upward Revision 9-25-25

1Q25 GDP: Final Estimate, Consumer Fade 6-26-25

Trump’s “Greatest Economy in History”: Not Even Close 3-5-25

Gut Checking Trump GDP Record 3-5-25