Durable Goods Jul24: Transport U-turn

We look at the usually volatile durable goods release for a Transportation-led ‘best since’ month following a ‘worst since’ month in June.

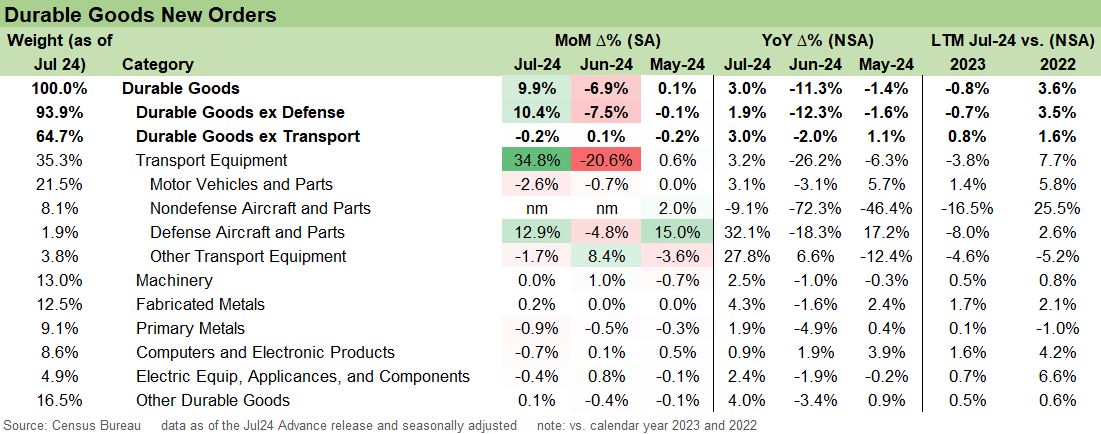

The surprise factor from a 9.9% month-over-month durable goods order comes on the heels of a major decline and largely can be traced to a bounce-back in transport goods. The ‘ex-Transport’ line has been much less volatile over the two months and registered a minimal -0.2% in July.

Durable goods orders overall on the year are just treading water with headline YTD down -1.4% vs. 2023 with the ‘ex-Transport’ line at least positive at 1.4%

The prospects for a rate cut and potential easing cycle raised by Powell last week means that capex cycles may get pushed back further and Durable Goods orders will limp on for a few months.

On a silver lining note, soft manufacturing indicators on balance give the FOMC more room to still cut even if PCE stays resilient.

The recent month-over-month changes in durable goods orders shown above have remained highly volatile. While the 9.9% increase this month is significant and ranks as the 7th largest monthly change, it barely surpasses the December 2023 level by 0.8%. In other words, this strong performance barely compensates for the losses experienced in January and June.

Stripping out what has been an extremely volatile transport line in recent months that has been a case study on the impact of Boeing on US economic data, the above chart shows Durable Goods ex-Transport. It changes the directional sign of the last two months but does not change the narrative: timid durable goods growth reflecting current restrictive monetary policy. Though we do not expect likely upcoming September policy changes to flip the switch, it could bring some capex planning off the sidelines.

Shipments flow into the GDP numbers but the capex planning ahead in the fall could be subject to capital budgeting headwinds if companies await more clarity on the tariff plans and fate of various major investment programs that had been supported by the Biden team and often opposed by Trump. That is notably the case in clean energy and EV programs. In addition, the certainty of tariffs in 2025 if Trump is elected could lead to more decision delays on capex programs. Those are just some considerations that need monitoring as election season plays out.

The line items for the Durable Goods release are listed above with the wild swings in Transport equipment on display. Away from the aircraft-related lines, the motor vehicles and parts line comes in at -2.6% MoM after and the past three months show decline for an industry with a lot of future investment still needed. The remainder of the line items below show broad softness with only Fabricated Metals with a small positive for the month.

For the tariff questions, the auto sector could be ground zero for revisions and new plans on spending rates heading into 2025. We have already seen material changes recently at Ford with more likely to come in the quarters ahead for the domestic capex planning in autos and the supplier-to-OEM chain for 2025 outlays.

We include the Durable Goods shipments lines above since they flow into the GDP calculations. The overall picture shows a decent month after a positive finish to Q2. Shipments operate at a lag so some of the recent weaknesses are still to be seen in the numbers above.

See also:

Footnotes & Flashbacks: Credit Markets 8-26-24

Footnotes & Flashbacks: Asset Returns 8-25-24

Footnotes & Flashbacks: State of Yields 8-25-24

Existing Home Sales July 2024: Making a Move? 8-23-24

Payroll: A Little Context Music 8-22-24

All the President’s Stocks 8-21-24

Footnotes & Flashbacks: Credit Markets 8-19-24

Footnotes & Flashbacks: State of Yields 8-18-24

Footnotes & Flashbacks: Asset Returns 8-17-24

Housing Starts July 2024: The Working Capital “Prevent Defense” 8-16-24

Retail Sales: Third Wind? 8-15-24

Industrial Production: Capacity Utilization Trends 8-15-24

Total Return Quilt: Annual Lookback to 2008 8-14-24

CPI July 2024: The Fall Campaign Begins 8-14-24

Credit Crib Note: PulteGroup (PHM) 8-11-24

Credit Crib Note: D.R. Horton (DHI) 8-8-24

HY Industry Mix: Damage Report 8-7-24

Volatility and the VIX Vapors: A Lookback from 1997 8-6-24

HY Pain: A 2018 Lookback to Ponder 8-3-24

Payroll July 2024: Ready, Set, Don’t Panic 8-2-24

Presidential GDP Dance Off: Clinton vs. Trump 7-27-24

Presidential GDP Dance Off: Reagan vs. Trump 7-27-24

|

|