Mini Market Lookback: When in Doubt, Get Forcefully Ambiguous

Another week dominated by trade themes saw bonds underperform and equities with a slight negative bias.

Anime? Looks like a national security threat to me! 100% tariffs!

The week saw mild weakness for duration on a small adverse curve move while credit spreads tightened, bringing HY OAS back to -108 bps below the long-term median and early April 2025 peak.

Equities saw the S&P 500 and NASDAQ in the red with the small cap Russell 2000 and Midcaps posting a modestly positive week. The 11 S&P 500 sectors saw 6 positive and 5 in negative range.

Trade still rules sentiment with Trump talking about a “total reset” this weekend in his social media “information.” The state of China talks will be more in the eye of the beholder after the Carney visit earlier did not bring much new to the table other than a modicum of awkward relative civility (Trade: Uphill Battle for Facts and Concepts 5-6-25). The latest we have from the China talks is Bessent saying they were “productive” and he would offer details on Monday.

A loose framework for a UK-US trade deal was set this past week that still came with major unresolved issues in critical areas such as pharma and some infill details needed on Section 232 “alternatives.” A consistent US goods trade surplus with the UK over the past decade did not hurt, so the value of UK extrapolation is limited if the real target is the trade deficits of other nations (see US-UK Trade: Small Progress, Big Extrapolation 5-8-25).

The coming week brings CPI, Retail Sales, Industrial Production, and Housing starts on the priority list for economic activity, but it is hard to get past the waiting game as the initial waves of high tariff inventory arrive and the impact of existing stockpiles and inventory liquidation start to get tested at the transaction level into the summer. The EU fight could just be starting while Canada remains under Trump’s tariff siege. Canada can wait for China progress (or lack of) and a response from the EU before it wades into the retaliation battle.

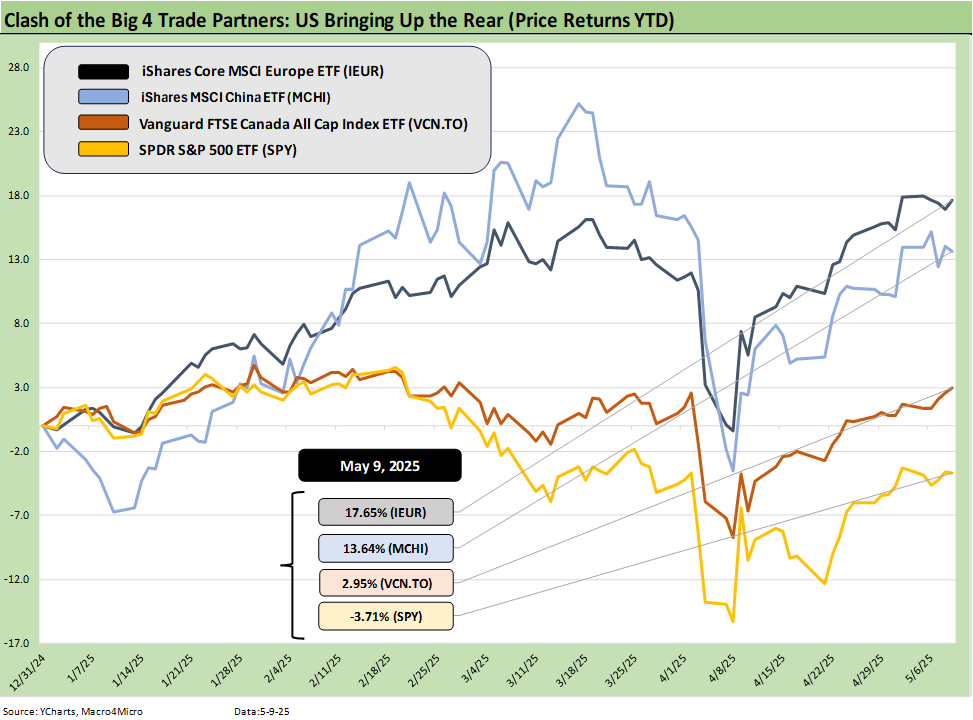

The above is our usual ETF stock chart covering the clash of the US with 3 of its biggest trade partners. (We leave out Mexico, which has somewhat of an EM asterisk.) We look at this mix as somewhat of a proxy for confidence in economic policies each week as the equity markets cast their votes YTD for US vs. China vs. Canada vs. Europe.

The ETFs we selected are diversified across industries and market caps with the exception of the US broad market large cap S&P 500 (SPY). Given the weakness of US small caps YTD, we were generous to the US. The S&P 500 is still pulling up the rear as #4 out of 4 with Europe #1, China #2, and Canada #3. Canada is around 7.7 points ahead of the US.

These ETFs in theory are forward-looking, and the valuation trends do not seem optimistic on the timing of the promised “New Golden Age.” The direction in month #5 of 2025 does not seem to be buying the story line of “billions and billions being brought into the US” by the Trump Tariffs. The fact is that billions are not “coming in” but are being paid by the US-based importer and not the seller. That is, tariffs are “American Peter” paying “American Paul.” Then Peter has to figure out how to recover that cost. Finding a GOP leader who will state that as simple fact is like a journey in the wilderness (see Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25).

Trade and tariffs had a busy week…

We had an updated round of news the past week that sought in part to promote a sense of forward progress. Carney was in the White House (the guest got minimal airtime), and there were few specifics of any sort on the other side of the meeting apart from a sustained interest in annexation. The short form on the week looks like this:

Carney in the White House: Carney of Canada was smooth while Trump rambled. The bottom line from Trump on Canada remains unchanged: “We subsidize Canada to the tune of $200 billion a year (our note: that number tends to float in his rhetoric). I don’t think the American public wants “me” to pay $200 billion a year to subsidize Canada.”

The fact is clear. The Goods deficit is not a subsidy, and Trump did not pay anyone anything. US buyers (businesses and consumers) bought the Goods from Canada, and they made the free choice to buy for a reason. Based on Trump’s logic and the fact that the US has a good surplus ex-crude oil, all he has to do is stop buying crude oil. Then (based on “Trump logic”), Carney would be “subsidizing him.” He can see how that move plays out with inflation numbers and his swing state votes in 2026. It would not be pretty. On a side note, Trump also ruled out small business exemptions. Otherwise, he might be admitting that the buyer pays.

Trump’s “I pay” subsidy mentality on trade deficits is the crux of the problem in trade policy and tariffs broadly at this point. The level of dishonesty and/or conceptual/factual ignorance will not be cured any time soon. It has morphed into political doctrine and is part of a loyalty test that “the leader” demands. The GOP Senate bobbleheads and bleating sheep in the House thus make it a theory that is borderline religion.

Section 232 on commercial aircraft, engines, and parts: The Commerce Dept has opened another investigation. This is one that could be used for EU horse-trading. The move will raise the stakes even further in the coming clash. The UK framework made some loose allowances for the category given the role of Rolls Royce in the UK. The Commerce Dept cited the concentration of US imports (read “Airbus” and Japan parts).

This will be a tough one given the duopoly of Airbus and Boeing and the regional jet players (includes Canada, Brazil) among other national flagship companies. Messing around with aircraft components/parts tariffs would also raise the costs of aftermarket services and maintenance, and that would flow into airfare pricing and costs in the air transport sector at some point. We will be watching the industry response on that one. It presumably will make life harder with the EU and Japan.

Movies, Film, and 100% tariffs: The main issue around this headline has been that it is a signal of what we call “Tariff Tourette Syndrome” that brings Trump to scream “tariff!” whenever someone highlights a loss of business for the US anywhere. This one confused many media industry watchers and trade law types since it was a services sector and left open the question of “100% of what?”

The film industry targeting will be seen as one more attack on Canada since that also came up in Bush 2.0 as an unfair trade practice (Section 301). It was not pursued back then since the case was weak. That was back in the days of more open trade, more interest in WTO compliance, and a bit less ally hostility and tariff fixation. The national security rationale is a tough case, but Trump may be concerned about some of the evil anime characters. They look like radical foreign, leftist violent lunatics. Therefore, IEEPA or Section 232 apply.

Court of International Trade (CIT): there will be a hearing this week in the CIT on the legality of the Trump tariff strategy. There are a range of suits working their way through the courts and notably Trump’s use of the IEEPA to exercise virtual dictatorial control of tariffs. The theory is that it is abuse of legislative intent and should not be allowed. Section 232 is more demanding and slower. The CIT case from the states look to make the case that the tariff actions undermine the ability of the States to plan and budget and manage their state and local needs, etc. That in theory gives the States standing. That is the theory. A group of Democratically run states are bringing the suit.

The busy week reminds us that potential Section 232 maneuvers (notably Pharma and Semis) are on the list of targets that will keep tariffs a major risk factor for months to come. The old tariffs will be rolling into new price impacts as the pause and negotiations move on and new tariffs assigned will set off a fresh round of ticking clocks. Additional attacks on commercial aircraft and the aero supply chain will certainly get more nations (i.e. voters) pushing their leaders to fight back. EU will not be happy with that one and pharma is on the way.

US-UK “deal” (aka “general framework with major open items”) was the headliner…

The US-UK deal generated some excitement just by being framed as a “deal.” The title on the White House Fact Sheet was “US-UK Reach Historic Trade Deal,” but the larger font subtitle on the cover page was closer to accurate: “Establishing a New Paradigm for our Special Relationship.” The relationship in trade is “special” just given the fact the US had a trade surplus for a decade (see US-UK Trade: Small Progress, Big Extrapolation 5-8-25).

The “deal terms” were not fully set since the issue of “alternatives” for Section 232 had to be worked out and pharma loomed as a major open item. The planned application of emergency powers and tariffs on non-US pharma still looms ahead, and that is going to be a major battle with the EU and potentially with China as well (see US-EU Trade: The Final Import/Export Mix 2024 2-11-25).

China holds a major weapon in pharma as a dominant supplier of generics and intermediate ingredients. Pharma and semis are still a work-in-process that could be the trigger point for a much larger clash with the EU as the #1 trade partner of the US. The damage China could do to the US through supply actions also has been speculated on for years.

The counterpoint from the tariff architects is that the US needs to be self-sufficient in case of war. They have not explained the strategy in the context of making a lot more enemies in the process and making national security worries a self-fulfilling prophecy. They also don’t point out that we are a nuclear power so the whole “war thing” seems a little strange. Some would argue it is about the ability to “control” everything from a domestic seat (that seat being in the White House for more than two terms).

The above chart updates the rolling 1-week and 1-month credit spread deltas for the IG and HY index and credit tiers from BBB to CCC. The rolling 1-month numbers are moving quickly at this point as the Liberation Day aftermath drops out of the measurement period from the initial peak sell-off (see Mini Market Lookback: A Week for the History Books 4-5-25).

The group of 32 benchmarks and ETFs we track turned in a 17-15 score this past week. We see the 7 bond ETFs at 2-5 with higher credit risk ETFs in positive range with EM Sovereigns (EMB) and HY (HYG). The large cap stock benchmarks (S&P 500, NASDAQ) posted negative returns with the S&P 500 in the bottom quartile and NASDAQ in the 3rd quartile with small caps and midcaps positive.

The E&P ETF (XOP) bounced back to #1 with a $4 per bbl rally in oil from Monday to Friday, but XOP still sits one above the bottom YTD at -9.7%. We detail more time horizons separately in our Footnotes publication on Asset Returns to be published later. The only ETF worse than XOP YTD is Transports (XTN), which sits on the bottom of the YTD return rankings at -14.6%. The Transports ETF (XTN) was also part of the “worst shall be first” rally the past week behind XOP as noted above.

The tech bellwethers were mixed on the week with 4 of 7 positive and 3 sitting at the bottom of the comp table above with Alphabet and Apple getting hit harder. Looking back over 3 months, the table shows only one positive with Microsoft. For 3 months, we see 6 of the Mag 7 with negative double-digit returns.

The UST deltas for the week are captured above with a modestly negative week for duration. The FOMC took some more bullets this week from Trump after Powell freely cited the threat of both weaker payrolls and higher prices on the other side of Trump’s tariffs. The independence of the Fed makes them the only body that can shape policy who can say out loud that tariffs lead to an importer being required to pay the tariff cost to Customs.

In other words, the Fed can deal in facts and concepts even if you disagree with them on timing and their conclusions on growth and future inflation and payroll trends. They know tariffs are an expense paid by a US entity that needs to be recovered or “eaten.” It really is that simple as a fact. It gets much more complicated as you seek to analyze how the costs are disbursed after the tariff is paid by the buyer across the supplier-to-customer chain.

The above chart updates the YTD UST deltas that show an overall bull steepener beyond the 2Y that has left the 7 bond ETFs we track all in positive territory. That is in a mix of 32 benchmarks that are at 17-15 slightly favoring positive YTD.

The above chart updates the running time series for the UST 10Y vs. the Freddie Mac 30Y mortgage benchmark. We start the time series back in Jan 2021 with a sub-1% 10Y UST in the back end of the COVID crisis and during the rollout of the vaccine.

HY OAS moved tighter during the week by -7 bps to +353 bps or -108 bps inside the long-term median. We are still +94 bps above the Jan 2025 lows. In early April the market had hit +461 bps.

The “HY OAS minus IG OAS” quality spread differential tightened by -3 bps on the week to +251 bps. That is a quality spread compression of -90 bps from the April wide levels after “Liberation Day.”

The “BB OAS minus BBB OAS” quality spread differential was flat on the week at +89 with both tiers tightening by -5 bps. That quality spread differential is -69 bps inside the early April wide.

Recent Tariff Commentaries:

US-UK Trade: Small Progress, Big Extrapolation 5-8-25

Tariffs: A Painful Bessent Moment on “Buyer Pays” 5-7-25

Trade: Uphill Battle for Facts and Concepts 5-6-25

Tariffs: Amazon and Canada Add to the Drama 4-29-25

Ships, Fees, Freight & Logistics Pain: More Inflation? 4-18-25

Tariffs, Pauses, and Piling On: Helter Skelter 4-11-25

Tariffs: Some Asian Bystanders Hit in the Crossfire 4-8-25

Tariffs: Diminished Capacity…for Trade Volume that is…4-3-25