United Rentals: Another Billion Out of the Gate

We look at another billion dollar deal for United Rentals as that size transaction starts to look routine.

The Yak Access transaction is just the latest for a company that can now look at billion-dollar transactions as ordinary after over $12 bn in acquisitions since 2011 and the highly successful integration of those deals.

The more significant aspect of the Yak deal was the description as a “new adjacency” and “cross-sell” opportunity as URI looks to expand in a bullish construction market with a heavy slate of power and energy investment ahead no matter who wins the election.

The latest United Rentals deal for $1.1 bn has by this point taken on the nature of routine business in terms of size. The deal is valued at 6.4x EBITDA and an “adjusted purchase multiple” of 5.2x net of tax benefits and cost synergies. Yak Access is a private company owned by Platinum Equity.

Unlike some of the deals that would be a heavy lift to bring margins up to URI standards, Yak EBITDA margins were reported at over 48% and are already in URI’s area. The deal will be “immediately accretive” to earnings and cash flow. Yak is a leader in hardwood mats and provides temporary access solutions across major project categories such as pipelines, power lines, wind, and solar.

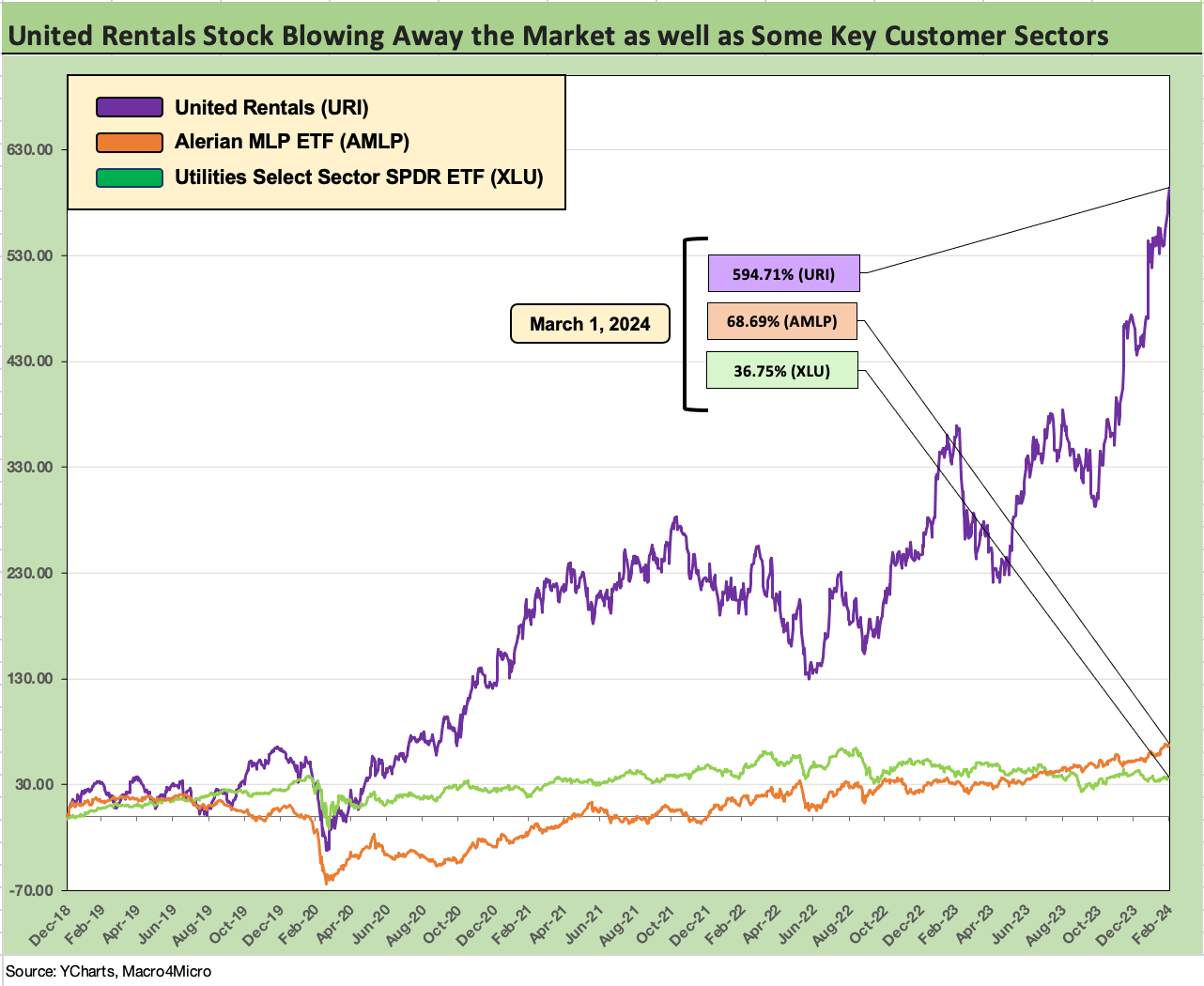

We frame URI equity in the chart above against the Midstream and Utility customer base it is serving.

As we detailed in earlier work on United Rentals (see links at bottom), the company has been an impressive outperformer with high margins, low leverage, and balanced capital allocation priorities. While the capital structure layers complicate the pace of credit rating upgrades, we see URI as an investment grade caliber risk (see United Rentals: Another Bellwether Supporting the Macro Health Story).

The acquisition marks a newer initiative for URI and comes at a time when so many major projects with longer timelines offer opportunities to deploy a wider range of equipment and services. These themes have been common ones on URI earnings calls with URIs involvement in various mega-projects in such areas as infrastructure, EVs, and LNG.

The size of the Yak deal does not rank high on the list for URI since it has had $1 billion or more in total detailed under “purchases of other companies” in its cash flow statement for 5 years since 2012, and this will make 6 years. We have seen fiscal year acquisition totals over $2 bn handles in 3 of the past 7 years with 2018 just shy of $3 bn. In other words, big ticket M&A acquisitions are a standard part of the URI business model. The company combines acquisitions with a heavy capex slate along the way.

The deals are easily financed from ABL lines and ready access to the unsecured debt markets. A current coupon URI bond would meet strong demand as a new issue. At upper 5+% handles based on current trading levels for the 2031s and 2032s around 5.6% (Source: 7Chord, ICE), this would be part of what will be a new set of coupons ahead in refinancing for many BB tier and BBB tier companies (see Coupon Climb: Phasing into Reality 12-12-23).

See also:

United Rentals: Another Bellwether Supporting the Macro Health Story 1-31-24

Rental Equipment: A Cyclical Confidence Booster 9-15-23

Credit Crib Notes: United Rentals (URI) 9-12-23

Ashtead 4Q23/FY 2023 - Company Comment 6-14-23

United Rentals: Investor Day Backs Up Bulls 6-11-23