Coupon Climb: Phasing into Reality

We look at the corporate bond coupon mix across IG and HY as cash income levels and market yields materially diverged in the UST curve shift.

We look across IG and HY markets at the mix of coupons across a wide range as investors get used to a mix of accretion income and coupon cash flow in their return mix.

The coupon shock and slow grind to refinancing and extension over time is all part of the UST curve and spread handicapping drill for liability managers and their advisers.

In US HY, we are not fans of the frequent “maturity wall” overstatement, but there will be a time for borrowers to take a hard look at prudent refinancing and extension moves across 2024.

For most corporate financial execs, the menu will mix selective secondary buybacks or taking the coupon increase pain to make sure the maturity schedule works for various downside scenarios.

The coupon is about as basic as it gets around why an investor buys bonds. The cash income piece of the total return puzzle is still a mainstay in the return picture. Whether it be retirement funds who draw down income out of current portfolio cash flow or funds that pay a dividend, the portfolio structuring exercise still requires investors to keep an eye on portfolio cash flow.

During the ZIRP period, yield starvation and cash income desperation went hand in hand. That mix will be changing quickly with the repriced UST curve. The above chart shows the mix of coupons in IG and tells a story of how wide the coupon range is in the $8.7 trillion IG market.

In this market, sometimes 1990s and 2000s vintage high coupon legacy bonds that are inside 10 years are some of the most interesting for those who need a balancing act of income and call protection in their bond portfolio mix. With the UST market now running from 5% handles on the short end out to 4% handles in 2Y UST out to 30Y, the new waves of UST supply could and should find a ready-made retail market for those with more of a focus on current coupon and higher cash income returns for their portfolio.

3% to 5% coupons lead in IG share but new issue will shift the mix…

The above chart frames the mix of IG coupons in the market with the heaviest mix of face value in the two buckets from the 3% to 4% range and the 4% to 5% range. Those two ranges are evenly distributed and comprise almost half the IG index face value. Those two brackets are flanked by the 2% to 3% range and the 5% to 6% range that comprises another third of the index.

The call protection makes the story a simpler one for the IG borrower since IG issuers generally face punitive make-whole redemption provisions. For the liability managers and their advisors, the exercise is more about which discounted bonds to selectively buy back in the secondary market as the slow and steady adjustment to a new UST curve plays out in 2024.

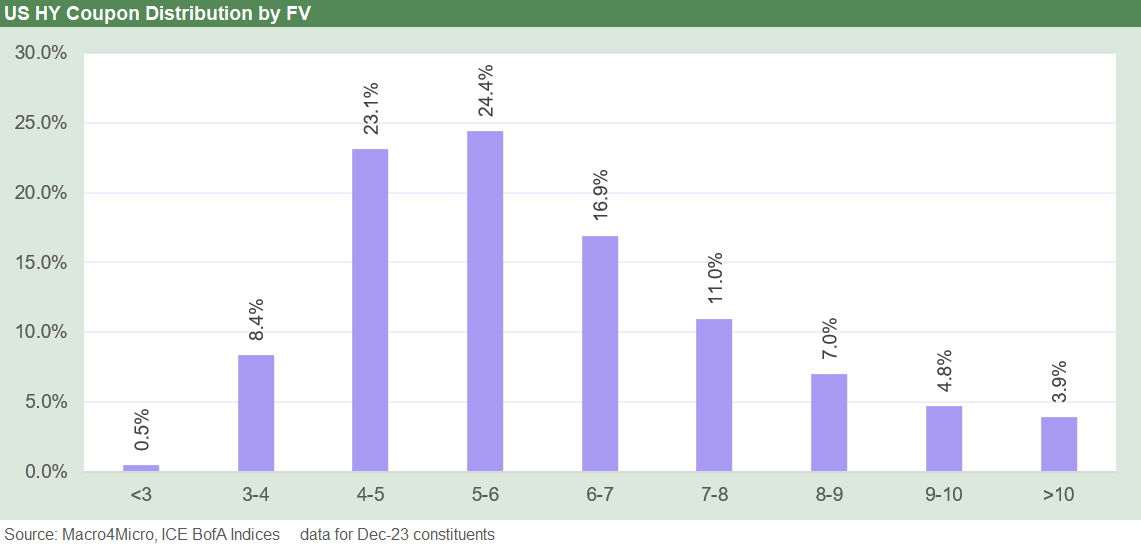

HY coupons: “who, when, and why” drive the refi and extension handicapping…

The more interesting challenge for investors and borrowers alike is on the HY side of the divide with a broader mix of make-whole and call structures. Reviewing names and their individual bonds is time consuming, but some issuers should get an asterisk or two as more likely to extend or buy back select layers along the way.

That refi handicapping exercise is notably the case with the quality BB and B tier names with very busy intermediate term maturity schedules. As we roll into 2024, reviews of issuers should include a look at how their liability management drill might shape up.

Below we break out the current coupon mix.

The mix of coupons broken out in the chart above gives a sense of the interest expense risks issuers in the market face with a par weighted yield in HY of 8.4% as of Monday 12-11-23 (vs. a 6.1% par weighed coupon), a 6.9% YTW for the BB tier (vs. a 5.4% coupon), 8.5% for the B tier (vs. a 6.4% coupon), and 14.2% for the CCC tier (vs. a 7.3% coupon). The par weighed coupons for the CCC tier is over 6.8 points below the prevailing yields, so that is one that makes for a tough refinancing story.

To refi or not to refi and when…

The rules of engagement in HY markets have always been to refi and extend “early and often” since you never quite know how the market events and risk appetites can trend based on history. You face the risk handicapping of the HY market crashing when you then might face banks who are not fond of refinancing short unsecured paper when the market is unfriendly to extension and new issuance on an unsecured basis for the name. You often see restrictions on short borrowing at maturities inside the bank lines further down the credit tier and such limitations also often show up in the definition of restricted payments.

There are also strategic issues in the liability management mix if an issuer might be planning a more aggressive slate of M&A ahead and would like to extend ahead of that action. Some industries are clearly consolidating, so planning ahead is part of the guesswork. If downgrades come out the other side, the clean-up of near term maturities would make more sense sooner rather than later.

After the COVID shock, the oil market swoon, and the financial crisis fallout, the willingness to be overconfident around assured, cost-effective market access is not a great idea for the prudent balance sheet manager. This set of conditions creates a need for critical decisions by the borrower.

The backdrop also presents some upside opportunities for investors who may have a view of which companies might step in to be more conservative in managing their maturity schedule risks. This comes at a time of discounted dollar prices on bonds after the UST curve shock of 2022-2023. Whether it be the coupon, maturity schedule, or concerns around cyclical or issuer-specific weakness (litigation, etc.) and evolving risks in their business, taking care of refinancing risk is an overriding priority for the typical HY name.

We assume the owners of those bonds with tight borrowing limits and potential cash coupon refi stress are under a microscope by bondholders and are being rolled into default models (e.g., distressed exchange risk or otherwise), but we were thinking also about the quality B and BB tier names that would be easily able to refi and extend in 2024. Those are the selective handicapping drills where the pull to par (or pull to call price) from discounted prices would offer the most incremental dollar price top-off opportunities in the market ahead under routine activities.

Watching the deltas from quarter to quarter in the debt footnotes or monitoring what the companies have to say about debt buybacks will be another routine exercise in earnings and reporting season in 2024.

Contributors:

Glenn Reynolds, CFA glenn@macro4micro.com

Kevin Chun, CFA kevin@macro4micro.com