GDP 4Q25 Second Estimate: Sharp Move Lower

A weak advance estimate for 4Q25 just got weaker on revisions with annual 2025 GDP now at 2.1% vs. 2.8% in 2024.

Step right up and see the greatest economy in history!

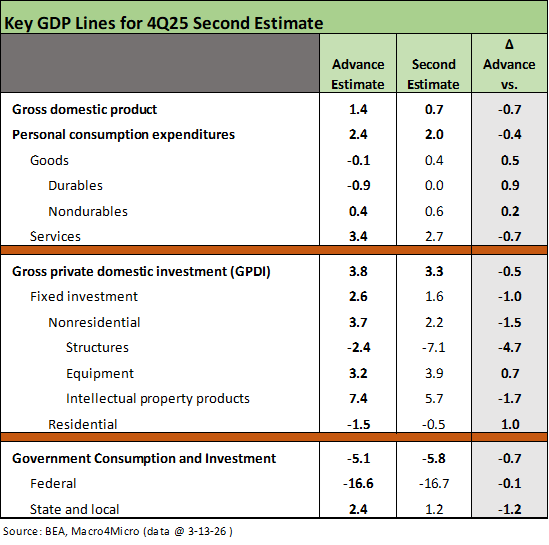

The decline in GDP for the 2nd estimate is tied to lower personal consumption expenditures (PCE), weaker fixed investment in structures, and another negative Government line. The unfavorable PCE delta vs. the advance estimate was in Services, but relative to 3Q25 the PCE weakening is evident in both Goods (+0.4% goods in 4Q25 vs. +3.0% in 3Q25) and Services (+3.6% in 3Q25 vs. +2.7% in 4Q25). PCE is 68% of GDP, so that is the main event (see 4Q25 GDP (Advance Est.): Less Distortion This Time 2-20-26).

The annual GDP growth rate for calendar 2025 was revised slightly lower to 2.1%, which is lower than the 2.8% GDP growth in calendar 2024. That is unlikely to come up in conversation around the “greatest first year of a Presidential term in history.” We look at the PCE inflation topic in a separate commentary later today.

The chaos of government budgets in an economic expansion has been a big story in 2025 with a -5.8% GDP line for 4Q25 including -16.7% for the Federal GDP line (Table 1 of the release). That brought an overall GDP contribution (Table 2 of the release) of -1.03% to 4Q25 GDP. We see 3 of the 4 quarters of 2025 for Government GDP posted negative contributions to GDP. That will change on defense in 2026.

The above table details the major GDP line deltas for the second 4Q25 estimate vs. the advance estimate. We see the major revisions in PCE and Fixed Investment as the most important moving parts for a read on the broader cycle and economic expansion. The downward revision of PCE and downward revision of Fixed Investment go in the “negative column” as incremental variables. Residential was revised upward but remains negative.

The Government GDP lines were also revised lower for Federal and State and Local, but that tends to be more about policy than the economic cycle. That said, those are real jobs with real consumption and are signaling “less” at the Federal level. The Iran War will make for more interesting reading on the Federal line in 2026.

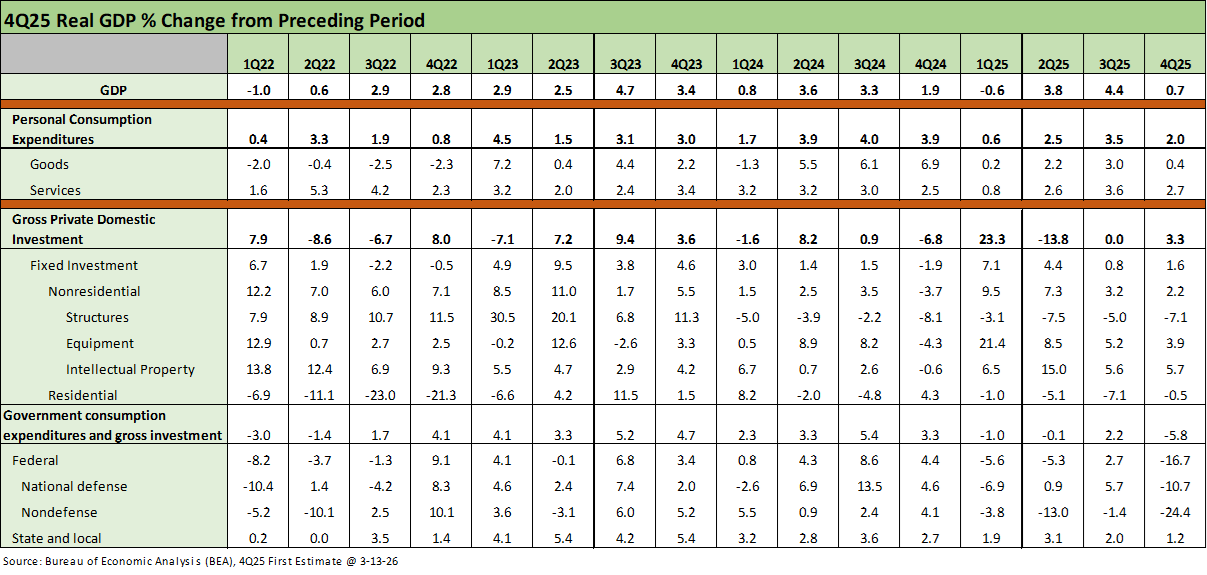

The above table updates the running quarters from the 1Q22 period when ZIRP ended and the tightening cycle began through 4Q25. The 1Q25 to 3Q25 periods have more than a few distortions to consider outside the critical PCE and Investment lines. We have looked at those moving parts in other commentaries. The “distortions” primarily tie into net export/import measurement and working capital swings around tariff phase-in dates (see 1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25, 2Q25 GDP Final Estimate: Big Upward Revision 9-25-25, 3Q25 GDP: Morning After Variables to Ponder 12-27-25).

We take the view that the PCE lines and Fixed investment lines are the main events for a read on the cycle. There are some other “noisy” lines that need to be looked at in context. For example, Net exports of Goods and Services posted a -0.22% contribution to the 4Q25 GDP line after +1.62% in 3Q25, +4.83% in 2Q25 and -4.68% in 1Q25.

For changes in private inventories, we see a +0.28% contribution to GDP in 4Q25 after -0.12% in 3Q25. The wild inventory distortions around tariffs drove a -3.44% contribution in 2Q25 (ties into the net export/import distortion) and +2.58% in 1Q25 ahead of the key tariff dates.

Overall, the 4Q25 GDP number was bad and the annual GDP number was unimpressive but competitive with the post-2000 US economic growth numbers. Compared to the 1980s and 1990s, the 2025 GDP numbers were poor. They were also much worse than 3 of 4 Carter years. “The numbers are the numbers,” and that makes them facts. Interpretation and analysis and cause-and-effect color is a separate drill.

See also:

4Q25 GDP (Advance Est.): Less Distortion This Time 2-20-26

3Q25 GDP: Updated Estimate 1-22-26

Cyclical Histories: Will Facts Be in Vogue in 2026? 1-2-26

3Q25 GDP: Morning After Variables to Ponder 12-27-25

2Q25 GDP Final Estimate: Big Upward Revision 9-25-25

1Q25 GDP: Final Estimate, Consumer Fade 6-26-25

1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25

Trump’s “Greatest Economy in History”: Not Even Close 3-5-25

Gut Checking Trump GDP Record 3-5-25