US Trade with the World: Import-Export Mix

We break out the leading import/export lines for US trade with the world during 2025. The economics of “buyer writes the check” are still the same.

Like Kilroy, Trump’s tariffs are ubiquitous and will leave a mark everywhere.

The tariff rules of the game have not changed much in terms of the economics for trade partners and all-in tariff exposure. The potential for the EU and Canada to fight back still lurks. In particular, Canada faces major risks ahead in the USMCA review while Mexico tends to surrender. Canada is the largest export market for almost 3 dozen states, so macro risks are not small there if national pride causes resistance.

The behavioral dynamics and rules of engagement in tariff negotiations could certainly change. Limits on Trump’s typical behavior could narrow the tariff risks to legitimate trade gripes. For example, 50% tariffs on Brazil with a US-Brazil trade surplus should not - under non-IEEPA rules - allow a Trump reaction such as “I don’t like that you arrested my ‘coup bro’ so I am hitting you with 50% tariffs.” We assume Trump would lose the legal right to say, “France, you said mean things and did not kowtow, so here are 200% tariffs on wine.” Then again, Trump likes testing legal theories.

The legacy delegation of tariff authority by Congress to the Executive Branch is a well-travelled story, so we are surprised so many observers just seem to suddenly see that fact. Trump tried to turn IEEPA into an unbridled trade bludgeon he could use at his whim. The constitution is clear that taxes originate in the House of Representatives – not the White House. Tariffs were called “taxes” nonstop back in the Ryan/Brady “border adjusted tax” reform bill of 2017 (shot down by Trump and the Senate).

Trump tried to get around Congress with IEEPA to give himself maximum, unchecked control. He failed and now has less leverage to flare up and aim tariffs at whim. Laws and legal avenues are still available even if the tariff reality (effective rates in total) has not changed much.

Trump has already abused the clear intent of Section 232 “national security” tariffs (Upholstered furniture? Kitchen cabinets? Seriously?!). When some smart GOP Senators such as Corker and Toomey tried to reel in Section 232 abuse during Trump 1.0, they got crushed. The GOP Senate sheep got the message and started to imitate the House bobbleheads.

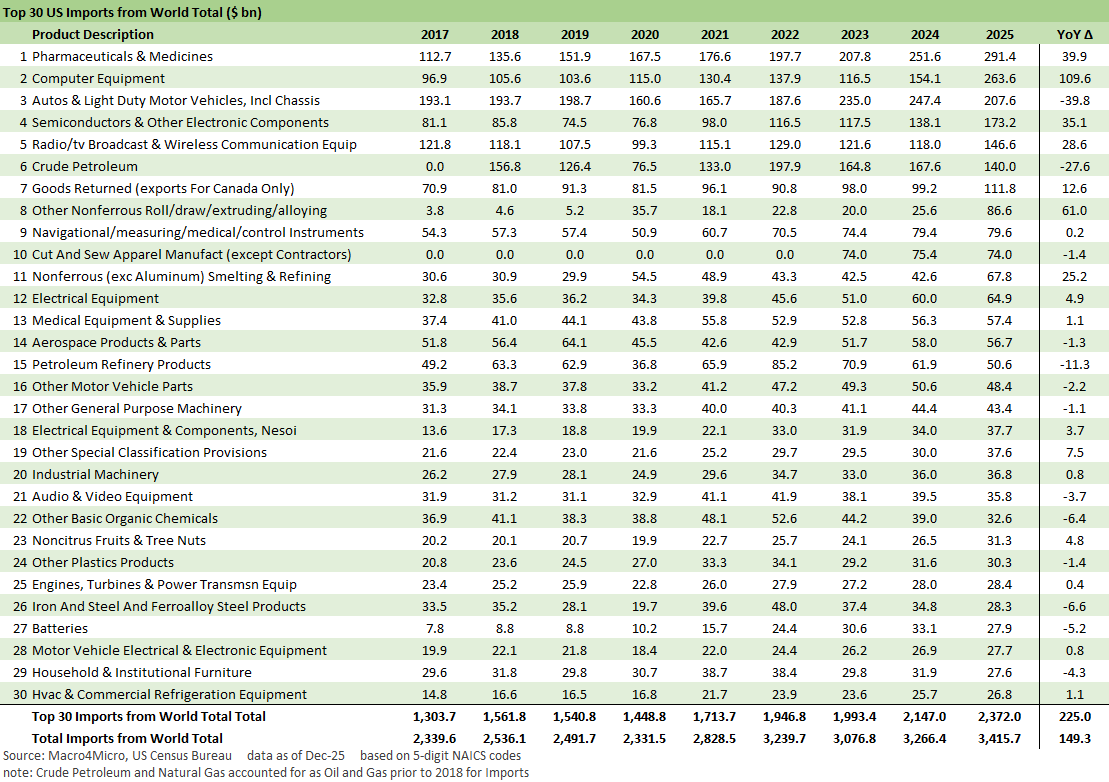

The above table updates the product line trends. We already addressed the record trade deficit in goods in earlier commentaries (see 2025 trade Deficits: Reality vs. Rhetoric 2-19-26, Trade Deficits: Math Challenge 1-30-26). The above just adds some useful granularity around major product lines. We line them up highest to lowest. We include YoY deltas in the column on the right.

The product groups with the largest moves in imports across 2025 have resulted from major moves in Switzerland (see US-Taiwan Trade: Risks Behind the Curtain 2-1-26) and Taiwan (see US-Taiwan Trade: Risks Behind the Curtain 2-1-26). Those two nations have some interesting story angles with Switzerland showing major variances in the two-way traffic of the gold trade (gold vs. refining vs. bullion). Given the erratic trade behavior of Trump and fears around UST and the dollar, it is no small irony that he made that US-Swiss trade deficit worse.

For Taiwan, the geopolitical stakes are very high given the “one China” priority of the PRC and tension over arms sales to Taiwan. This topic cuts across a lot of history. The tech boom has driven soaring demand for Taiwan-based products from semis to tech and electronics. We look at those issues in the country trade links below. China + Taiwan as a combined economic power would rattle some nerves in the GOP.

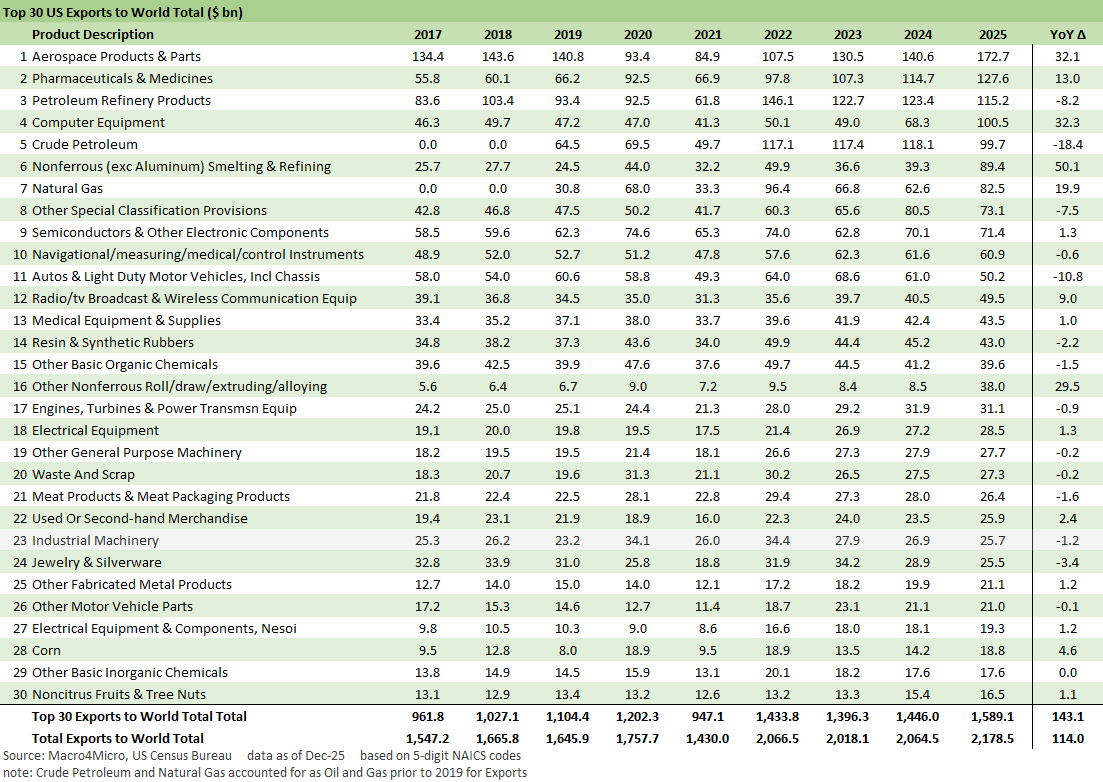

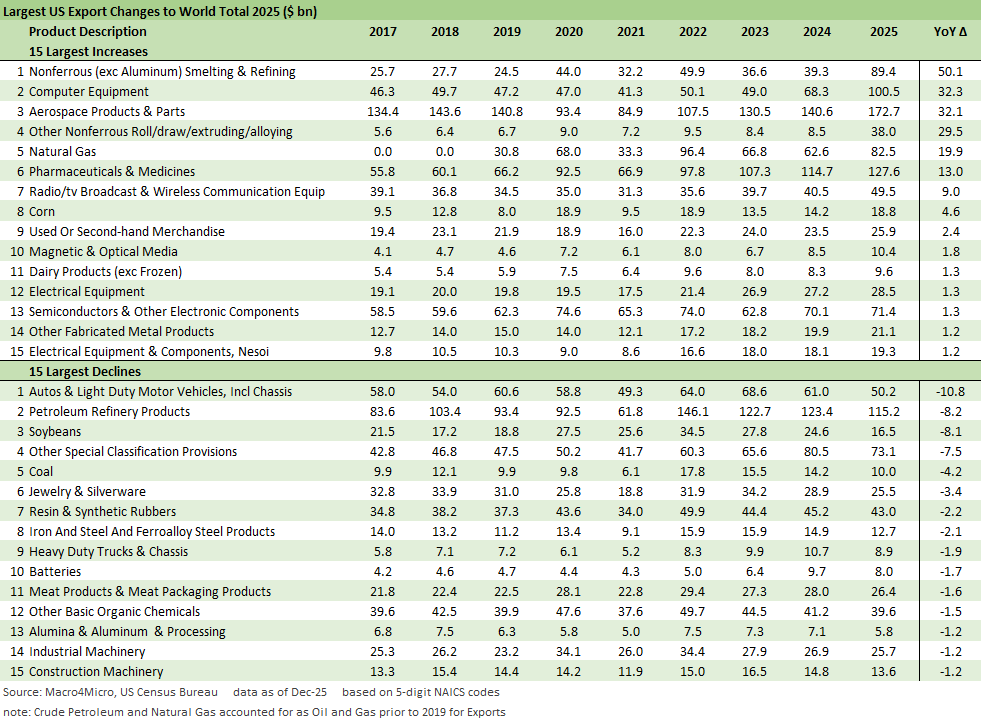

The export list shows the power of US aerospace with Boeing and US aerospace leaders always there near the top of the export lines. The strong presence in pharma and energy is routine as well. The table also shows some of the big swings in gold (in “nonferrous”) that we highlighted in the Switzerland trade commentary. The US is a major factor in the export of crude oil, natural gas, and petrochemicals (and resin and synthetic rubber).

The fact that the US is a massive crude oil exporter while it has a goods trade surplus with Canada ex-crude is supposed to elicit a flicker of awareness in Trump on the nature of the import-export mix. A few years of record US energy exports can easily dovetail with Canadian imports of crude that drive a goods deficit. While Trump may look to Venezuela as a supplier of heavy crudes in the future, the heavily favored discounted heavy crudes from Canada make that trade partner a key supplier to sophisticated complex US refineries. Otherwise, refined product prices would be higher in the US.

Canada has the highest value-added export mix among leading trade partners (see Canada-US Trade: Trump Attack N+1 1-25-26). Despite what Trump says (“Canada has nothing we need”), the US arm’s length buyers would be inclined to disagree (they prove that in their independent free market decisions). The natural resource mix from Canada is critical (e.g. perhaps Trump has found some potash and uranium in Palm Beach).

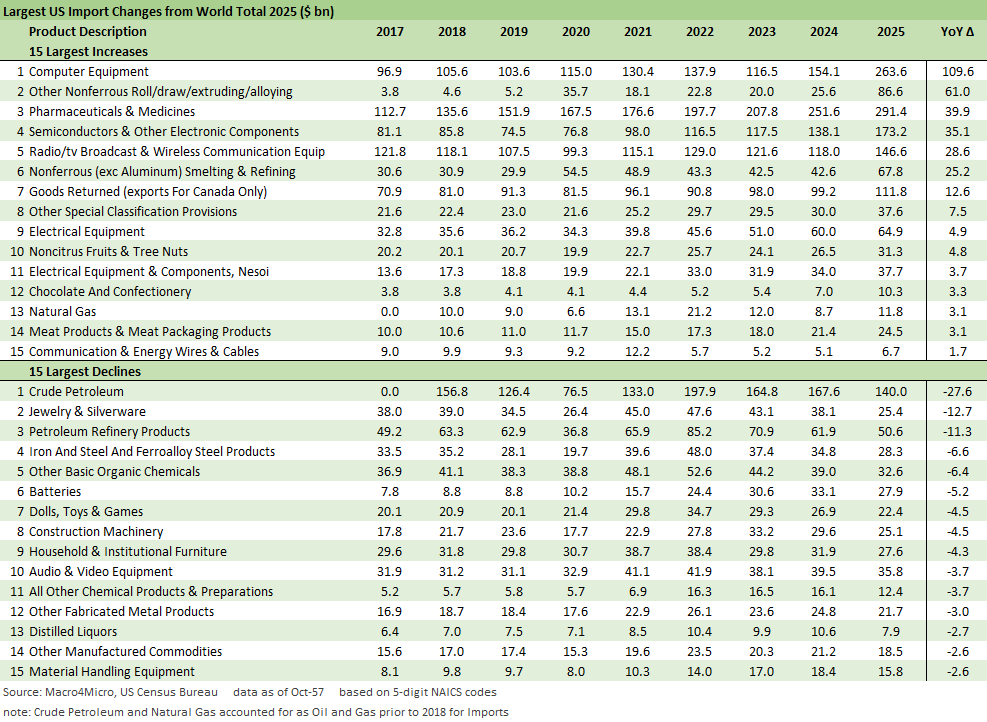

The above chart gives another angle on major import deltas into the US in 2025. We show the biggest import increases and decreases with the delta column on the right. Energy, Tech, Pharma and Gold ruled the headlines. There is not much drama in aerospace in 2025, but Trump seems determined to change that with Canada in 2026.

The above chart gives another angle on major export deltas from the US in 2025. We show the biggest increases and decreases with the deltas on the right. The spike in nonferrous is tied in part to increased demand for gold and higher shipments to refining centers (Switzerland). Soybeans took a beating on lower China volumes in 2025 as Trump delivered a very unsurprising bailout to the ag sector again (first one in his 1st term), raising the indirect costs of his tariff program even more.

See also:

2025 trade Deficits: Reality vs. Rhetoric 2-19-26

Switzerland-US Trade: A Deficit that Glitters 2-3-26

US-Taiwan Trade: Risks Behind the Curtain 2-1-26

Trade Deficits: Math Challenge 1-30-26

China Trade: Shrinkage Report 1-28-26

|

|