Retail Sales April 25: Shopping Spree Hangover

A mild April retail sales print follows a March boosted by pre-tariff buying — leaving a wait-and-see consumer in its wake.

Don’t look at the prices…

Last month’s retail surge reflected tariff anxiety and pull-forward effects. April, by contrast, reads as a wait-and-see period as the reality of new pricing begins to hit shelves. The increase to headline retail sales of +0.1% MoM is thus good news largely by omission of bad news in the consumer picture as the months ahead will provide clarity on the extent of tariff effects.

While the worst-case tariff fears have abated following a US-China truce and softer negotiation signals, the reality of 30% on China, 10% minimum globally, and a plethora of Section 232 targets still in play leaves uncertainty abound. The April NY Fed Household Survey showed a sharp rise in inflation expectations, alongside weaker labor and income outlooks — a combination that pressures spending decisions.

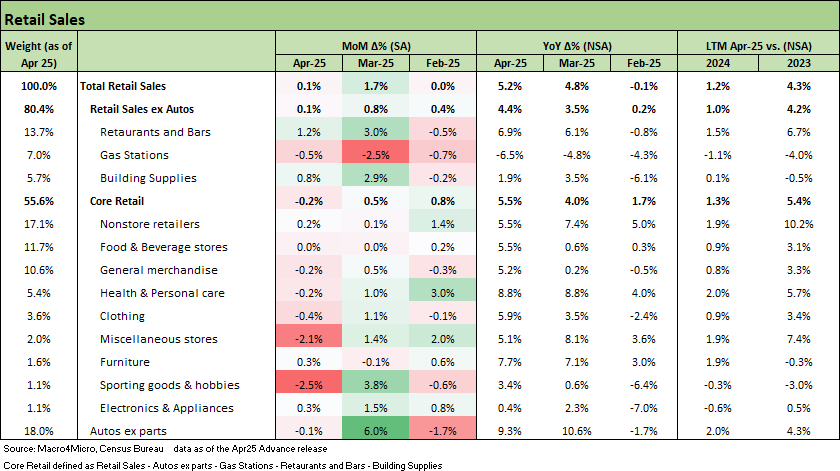

The core retail sales reading showed lowered demand at -0.2% MoM as much of the pull-forward of buying faded after surges in discretionary goods categories last month. Instead, the positive headline number this month was largely supported by another strong month of restaurant and bars spending, which grew +1.2% MoM.

The above chart shows the sharp deceleration from March retail sales as the +0.1% this month reads like a hangover from the pre-tariff spending sprees on larger discretionary purchases last month. This reading is still in the ‘too soon’ bucket for where tariffs have hit prices on shelves for consumers, even more so given the inventory building strategies to help moderate the near-term impacts. The CPI print this week was along the same vein as the April data is adding up to more anticipation for those awaiting real tariff impacts.

The good news is that the major threat of supply shock from what was effectively a freeze in US-China trade takes a lot of pressure off the consumer. However, a 30% tariff rate still leaves open questions about where that cost gets borne and what trade-offs consumers will have to make. We expect that sticker shock on larger purchases leads to divergences across discretionary and essential spending as consumers reprioritize amid renewed inflationary effects. Walmart’s clear signaling of upcoming price increases is a bad omen for who bears the cost of tariffs — and it’s clearly not the seller.

Even with an improving trade picture, the consumer is not likely to find much relief from tariff and stagflation driven anxiety. Though missing the major developments on trade deals and truces, the most recent NY Fed data echoes the well-documented decline in consumer sentiment from the UMich reports. That most recent survey shows concerns on inflation and labor market weakness. Headline driven chaos often leads to consumer pullbacks, as budgeting becomes a guessing game of “how much higher?” Resuming student loan payments earlier this month is another monthly expense that many will have to add to that budget calculus and dampen demand elsewhere.

The above chart covers the line item details for this morning’s release as well as the key ‘ex-Autos’ and Core aggregates. Only Restaurants and Bars (+1.2%) and Building Supplies (+0.8%) were strongly in the green this month, driving the overall headline to positive despite a negative core reading.

Down below in the lines for the core readings, the major movements are snapbacks in the smaller, discretionary categories that saw large bumps last month like Miscellaneous stores (office supplies, craft hobbies, specialty, etc.) and Sporting goods & hobbies. The largest categories of Nonstore retailers at +0.2% and Food & Beverage flat on the month continue a relatively stable trend, pointing already to signs of divergence in necessity and discretionary categories as consumer demand responds to new trade policy.

Today’s retail sales release does not carry major alarm bells yet and we will see how the paring back of severity around tariff implementation and trade policy impacts consumer behavior. Prices are slated to rise, and anxiety is already building. At a minimum, it is likely we will enter a phase of demand retrenchment and tighter consumer purse strings — a shift that will alter revenue outlooks. However, until then, the market has adopted a wait and see approach that does not yet see the consumer cracking.

See also:

CPI April 2025: 1st Inning for Tariffs and CPI 5-13-25

Credit Spreads: The Bounce is Back 5-13-25

Footnotes & Flashbacks: Credit Markets 5-12-25

Footnotes & Flashbacks: State of Yields 5-11-25

Footnotes & Flashbacks: Asset Returns 5-11-25

Mini Market Lookback: When in Doubt, Get Forcefully Ambiguous 5-11-25

Credit Snapshot: PulteGroup (PHM) 5-7-25

Credit Snapshot: Toll Brothers 5-5-25

Mini Market Lookback: Inflated Worry or Slow Train Wreck? 5-3-25

Payrolls April 2025: Into the Weeds 5-2-25

Payroll April 2025: Moods and Time Horizons 5-2-25

Construction: Singing the Blues or Tuning Up for Reshoring? 5-1-25\

Employment Cost Index 1Q25: Labor is Not the Main Worry 5-1-25

1Q25 GDP: Into the Investment Weeds 4-30-25

PCE March 2025: Personal Income and Outlays 4-30-25

1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25