Credit Spreads: The Bounce is Back

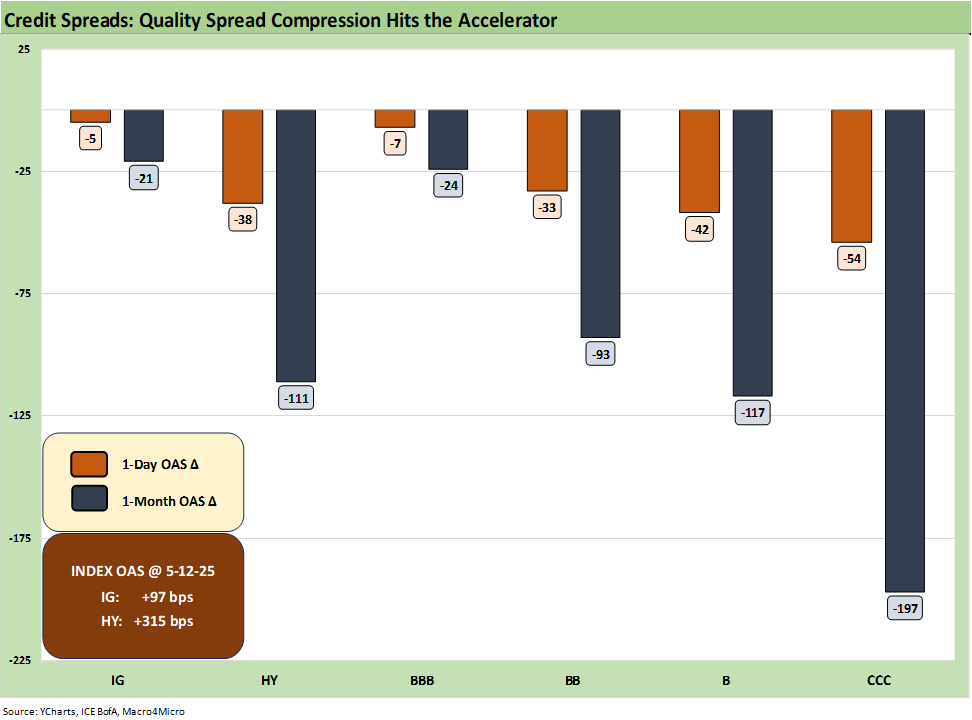

We plot the 1-day and 1-month post-China credit spread moves on the back end of a very volatile stretch.

At +315 bps, HY OAS just dipped below the early Oct 2018 cyclical lows (+316 bps) and further below the June 2014 lows (+335 bps). The quality spread compression makes a statement on the comfort the market has with lower HY bond issuer default risks. A full meltdown of China-US trade flows could easily have kicked a default cycle into gear (notably in retail, more leveraged manufacturing issuers with broken supply chains, and the small/mid business subsector broadly).

From here, a return to a June 2007 spread range would be irrational given the reality of the lineup of tariffs in process. Those tariff effects (autos, steel, aluminum, etc.) will start ticking into transactions in the summer with even more “national security” tariffs in the queue (notably pharma, semis, aircraft/parts, copper, lumber). It takes time to work through the working capital management cycle and purchase contracts once the tariffs go into effect.

IG spreads returned to double digits at last night’s close with 97 bps, and that takes IG spreads below the June 2014 lows (106 bps) and closer to the Feb 2018 lows (90 bps.

The equity rally and spread compression is not a late breaking news item at all, but we thought it was worth marking with a timestamp. That was the case with the initial spike in spreads after the reciprocal tariff insanity was first released with its “magical” (and embarrassing) math formula used to set tariffs (see Tariffs: Diminished Capacity…for Trade Volume that is… 4-3-25).

The above chart shows the latest bout of volatility in the tariff drama, but this one continues the compression story as various pauses, backtracks, and retreats have helped the market get some reassurance that Trump (or his advisors) see the scale of the problem that had unfolded since the initial Liberation Day shock (see Reciprocal Tariff Math: Hocus Pocus 4-3-25, Reciprocal Tariffs: Weird Science Blows up the Lab 4-2-25).

As a frame of reference for the latest rolling 1-month HY spread compression of -111 bps tighter, the reciprocal tariff “hell week” generated a rolling 1-month spread widening by the end of the week at +157 bps. That came alongside the 1-week move of +98 bps.

That rolling month to start April made the top 10 worst months of all time (see Mini Market Lookback: A Week for the History Books 4-5-25, Footnotes & Flashbacks: Credit Markets 4-6-25). That “honor” was usually reserved for periods such as the TMT meltdown, the systemic credit crisis, the sovereign stress peak, and COVID. That is not good company for Trump in historical context.

The compression from the April peak is around -146 bps tighter from the OAS wide point in one of the wilder rides to occur. That is especially impressive with healthy major banks, a BB heavy HY index, an economic expansion still underway, and payrolls that effectively constitute full employment. Anyone outside the world of MAGA (even then a smaller subset of MAGA) would come away with the view that tariffs as a tool for tantrums and a de facto embargo of the #2 economy in the world goes in the “extremely stupid” category. Many would not say it with their outside voices, but that is obvious at this point. China has a lot more “supply side” weapons it has not pulled out yet – fortunately.

Many have also learned what most should have known. That is, China does not back down. History has shown that too many times. China is not the spineless US Senate or the partisan House. Trump ranting does not impress them and is a sign of cultural ignorance as much as it highlights a deficiency in historical perspective (note: Korean War, WWII).

Whether that lesson will be exported to the threat of a potential escalatory tariff nightmare with our #1 trade partner – the EU – remains to be seen. The EU as a group lacks the China resolve, but they have a lot of US targets including services. The #2 and #3 trade partners (#1 and #2 by nation) are in the USMCA, so we are not clear on whether the appetite for self-inflicted wounds has been satisfied yet for Trump.

Canada has the “province problem” impacting its arsenal for retaliation. Mexico has been remarkably muted in tone as a strategy. Political risks domestically in Canada and Mexico will be rising as the current tariffs take their toll and employment takes a serious hit.

An update on the Gang of Four trade partners…

The above chart just updates a visual we often use. It highlights where the broader equity proxies stand in the clash of the US, EU, China, and Canada. We typically leave Mexico off this comp chart for reasons already cited with its “EM” asterisk that China does not get from our vantage point. With everyone rallying off this news, the US is still in last place YTD but at least edged back into positive range. That is not insignificant as a metric that in theory is forward-looking.

See also:

Footnotes & Flashbacks: State of Yields 5-11-25

Footnotes & Flashbacks: Asset Returns 5-11-25

Mini Market Lookback: When in Doubt, Get Forcefully Ambiguous 5-11-25

Credit Snapshot: PulteGroup (PHM) 5-7-25

Credit Snapshot: Toll Brothers 5-5-25

Mini Market Lookback: Inflated Worry or Slow Train Wreck? 5-3-25

Payrolls April 2025: Into the Weeds 5-2-25

Payroll April 2025: Moods and Time Horizons 5-2-25

Construction: Singing the Blues or Tuning Up for Reshoring? 5-1-25\

Employment Cost Index 1Q25: Labor is Not the Main Worry 5-1-25

1Q25 GDP: Into the Investment Weeds 4-30-25

PCE March 2025: Personal Income and Outlays 4-30-25

1Q25 GDP Advance Estimate: Roll Your Own Distortions 4-30-25