United Rentals 4Q24: Strong Numbers Set the Table

We update the final FY 2024 numbers for URI ahead of a big H&E funding coming soon.

With 4Q24 earnings report and the filing of the 10-K this past week, URI’s FY 2024 final numbers set the stage for the H&E acquisition funding dead ahead. The latest URI 4Q24 and FY numbers and guidance for 2025 remind bondholders why URI bonds are a safe way to mitigate a range of cyclical and policy risk factors (see United Rentals: Bigger Meal, Same Recipe 1-14-25).

Investment incentives in a potential tax bill, less regulation, tailwinds for energy capex, and a “call option” of sorts on the pace of reshoring all make for a good overall story for equipment leasing companies even if you find the tariff plans ill conceived (which we do).

Trade clashes in fact make a risk-mitigation case for URI since the “fleet in hand” advantage supports using equipment rental in the lease vs. buy game plan.

Meanwhile, multiyear projects are still running strong even if some project categories may be at risk of getting dialed back. Many infrastructure projects and more energy programs are supported by the GOP even if EV faces a cloud. In other words, URI’s diversification helps as we await the final set of policies and legislation (see Credit Crib Note: United Rentals (URI) 11-14-24).

The tariff news hit on Saturday, and we see those as strong headwinds in broader cyclical context but more threatening to other industry groups with manufacturers and autos at the top of the list.

The above table updates the 4Q24 and FY 2024 operating results and line items including margins. The +9.7% on equipment rental revenue is strong. That’s the best YoY increase since 4Q23 at +13.5%. Gross margins and EBITDA margins narrowed modestly in 4Q24 and FY 2024.

As important as the overall reported numbers are for the stand-alone bond and stock story, United Rentals (URI) also serves as a valuable macro indicator with its extensive branch network and wide range of field teams who can help gauge customer sentiment from direct relationships and support their views with metrics in the trenches. The market color from the various customers is more than a qualitative sense since the customer activity flows into rental rates, utilization, fleet mix and demand, equipment returns, and forecasted incremental equipment needs (volume, mix) etc.

In other words, it is hard to find better color across such a wide array of end markets and verticals in more pockets of North America. The fleet size expectations (OER growth) and the gross capex across replacement vs. growth have a lot of empirical support for URI to make its decisions. When it increases its growth capex, that is a favorable signal.

The segment results (General Rentals, Specialty) show high margins as well as solid growth rates on the Specialty side of the business. Rising secular demand for leasing (vs. buy) and high secular growth rates for specialty equipment are important drivers of the URI stock and credit story. Specialty rental revenues was +25% in FY24 and over 30% in 4Q24.

More “cold starts” with a heavy weighting of specialty is part of the organic growth story. URI is not just about M&A and good integration execution. URI is also investing capex for growth.

As we have covered in past commentaries, URI takes pains to reinforce the point that lower margin GenRent equipment can deliver high returns relative to cost. The potential for high utilization rates and ability to deliver a wide range of equipment types on major projects all plays into the URI national scale and major customer advantage.

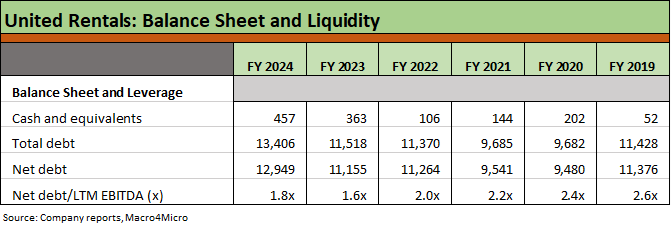

URI leverage (Net debt/Adj. EBITDA) remains low at 1.8x and is on the lower end of the company’s 1.5x to 2.5x range. URI posts the fiscal year end leverage in its quarterly presentations back to 2012, and the FY 2024 leverage is the second lowest across that timeline with only FY 2023 lower at 1.6x. URI even made a material acquisition in 2024 (Yak) (see United Rentals: Another Billion Out of the Gate 3-4-24, United Rentals: In the Market, Right on Cue 3-7-24).

The pro forma estimate provided by URI on the H&E Equipment acquisition calls for a 2.3x ratio that will be back to 2.0x within 12 months or right in the middle of its target leverage range and below the median leverage of more than a dozen prior FY periods.

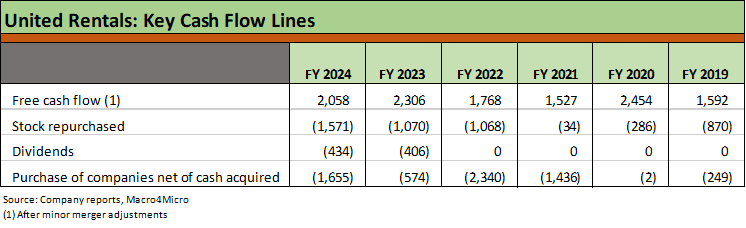

The above table details the history of free cash flow since 2019 along with the distributions to shareholders via buybacks and dividends. With a pause expected on buybacks wrapped around the H&E acquisition, the numbers tell a favorable story around how resilient URI’s credit metrics have proven to be even with around $6 bn of acquisitions from FY 2021 to FY 2024.

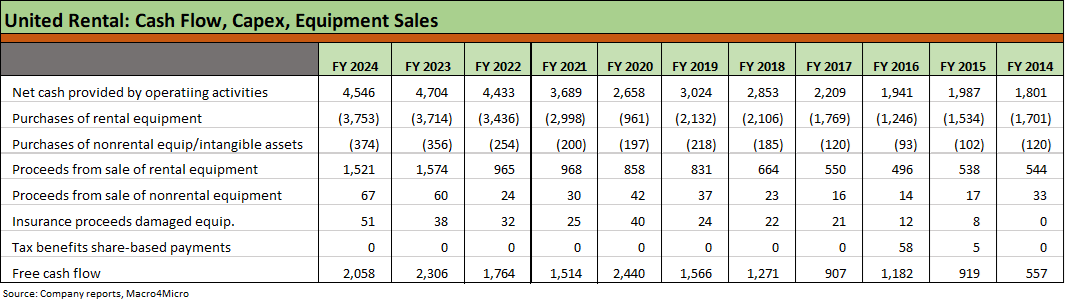

The above table is a historical update that URI routinely provides to show the moving parts of its operating cash flow history since 2014. The table shows gross capex and the active management of its fleet with planned used equipment sales supporting the financial flexibility profile of URI. The record revenue and EBITDA in 2024 supported the generation of over $2.0 bn in free cash flow after all the moving parts in the table above.

For 2025, URI expects a midpoint capex range of around $3.3 bn for maintenance capex and another $500 million for growth capex. An important factor in looking at the very high EBITDA margins is that URI needs to reinvest in capex to sustain that run rate. That has some similarities to the very high margins in upstream energy and its need to replace reserves via capex in what is a “depletion industry.” In the case of equipment rental, however, the underlying variables are far more predictable and the industry much less volatile. That is easily demonstrated in the revenues and cash flow trends across time.

The short lead time on new equipment purchase and the very active and transparent used equipment market has long been a reassuring part of the URI credit profile. That profile of capex and equipment sales allows URI to manage risks across different economic backdrops and more than a few crises along the way in the US and global markets. We have been watching URI directly or indirectly in our research roles since the late 1990s back when URI burst on the scene as a major, aggressive consolidator. They have a history of delivering to equity and credit quality alike.

See also:

United Rentals: Bigger Meal, Same Recipe 1-14-25

Credit Crib Note: Herc Rentals (HRI) 12-6-24

Credit Crib Note: Ashtead Group plc (AHT) 11-21-24

Credit Crib Note: United Rentals (URI) 11-14-24

United Rentals: Finetuning Strong Run Rates on Equipment Demand 4-27-24

United Rentals: In the Market, Right on Cue 3-7-24

United Rentals: Another Billion Out of the Gate 3-4-24

United Rentals: Another Bellwether Supporting the Macro Health Story 1-31-24