Credit Spreads Join the Party

Spreads spike from a very compressed level. We look at the 1-day and 1-month credit spread deltas.

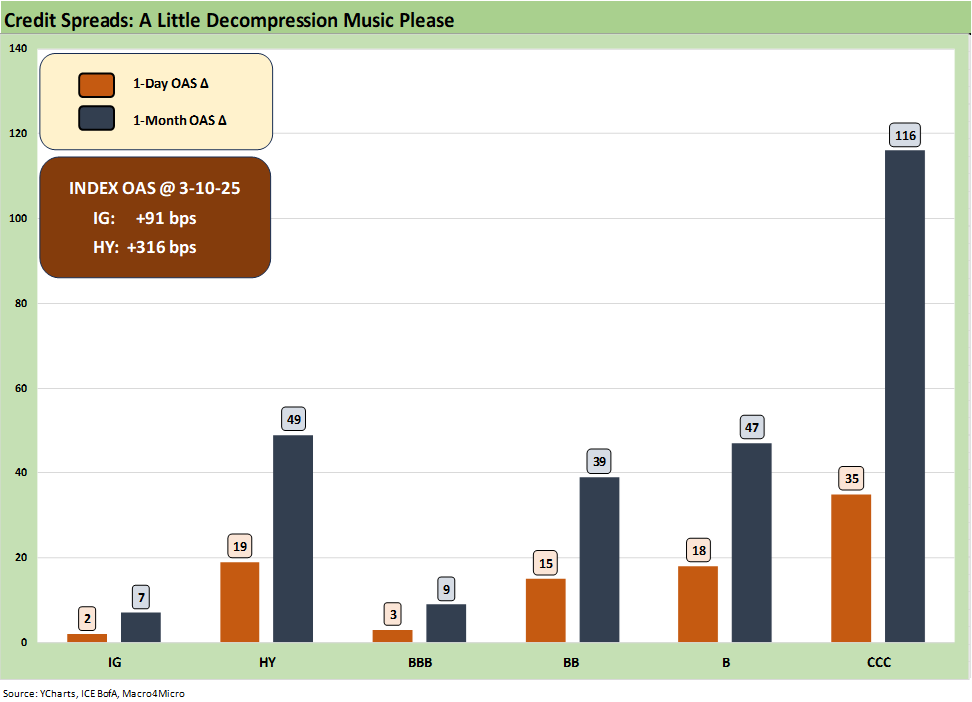

You guys are not invited to the credit party…yet

The equity markets were clearly very rattled while credit spreads saw a decompression wave from the bottom up that gets well outside the June 2007 range with HY at +316 bps.

IG spreads hold tight at +91 bps and remain similar with past IG spreads cyclical lows.

The HY OAS is sitting right on top of the early Oct 2018 HY credit cyclical lows even if they are +56 bps wider than the recent Nov 2024 lows (see Footnotes & Flashbacks: Credit Markets 3-10-25).

The above chart highlights the OAS delta moves for the 1-day and trailing 1-month time horizons. From its very compressed starting point, the spread wave still leaves HY and IG spreads tight in historical context. We break out IG and HY OAS deltas in the chart, and then we run down from the BBB tier to the CCC tier.

This was one of those days where credit markets did in fact follow the equity beatdown with a decompression wave. The CCC tier gapped by +35 bps on the day and +116 bps for the trailing 1-month. The decompression on up through the tiers is not a new pattern by any stretch. The CCC vs. B tier quality spread differential of +508 bps is only slightly wide to the long-term median of around +482 bps and slightly wider than the Friday close of +491 bps (see Footnotes & Flashbacks: Credit Markets 3-10-25).

Whether one views this economic “transition period” as “nothing to worry about” as Trump keeps saying, you just cannot keep blaming the “globalists” for dumping positions. More investors are likely some derisking of portfolios for better values later. It strikes us as fairly normal. It is about rising fundamental risks, some weaker economic numbers, and the erosion of faith in the economic strategy of tariffs and trade wars. Maybe Trump can just tell the market that the “seller pays” the tariff again, and the US Treasury will be bursting with imaginary revenues from trade partners.

The treasury will in fact be getting a lot of payments from US buyers/importers who will need to offset those tariff costs with price increases or other cost cuts to offset margin erosion (DOGE goes to the private sector, only with a rational plan and analysis).

The market awaits CPI on Wednesday, but the reality is that price actions would just be getting warmed up as tariffs work their way through the system at a lag. Most have not arrived yet, but Trump seems very excited to roll out the reciprocal tariff concept in style across April.

Tonight, we saw some reports in the Globe & Mail (Canada) that Trump will back off the oil tariffs on Canadian crude oil. There is also the school of thought that he will do some more moonwalking on the EU trade wars and offer more exemptions to domestic interests.

It is hard for investors to trade off erratic shifts in policy when private sector companies need to plan inventory, capex, place orders with suppliers, and enter into contracts. There will undoubtedly be more gamesmanship from here on tariff timing and magnitude.

You cannot “will away” double entry accounting and economic facts (“buyer pays”) with a hostile rejoinder to a question (and the media questions are typically weak from the cowed reporters).

See also:

Footnotes & Flashbacks: Credit Markets 3-10-25

Footnotes & Flashbacks: State of Yields 3-9-25

Footnotes & Flashbacks: Asset Returns 3-9-25

Mini Market Lookback: Tariffs Dominate, Geopolitics Agitate 3-8-25

Tariffs: Enemies List 3-6-25

Happy War on Allies Day 3-4-25