Iron Mountain 4Q24: Performance Bar Gets Raised

IRM sees the bar get raised on recent equity valuations with data center multiples. Impressive credit stability remains a fact.

In the equity markets, IRM has moved up in weight class after an extraordinary run. However, in the credit markets the low BB tier composite fails to reflect the impressive asset protection, high margins, financial flexibility, and discretionary cash flow. IRM has strengthened its balance sheet while rewarding shareholders with a growth multiple and higher dividend.

The dazzling stock performance of IRM since 2022 has been compelling even with the recent sell-off that followed higher UST since the Sept easing. More recently, the DeepSeek headlines generated some second guessing around what the growth multiple should look like for data centers and how that rolls up into the IRM revenue and earning picture and what IRM’s heavy growth capex program will bring.

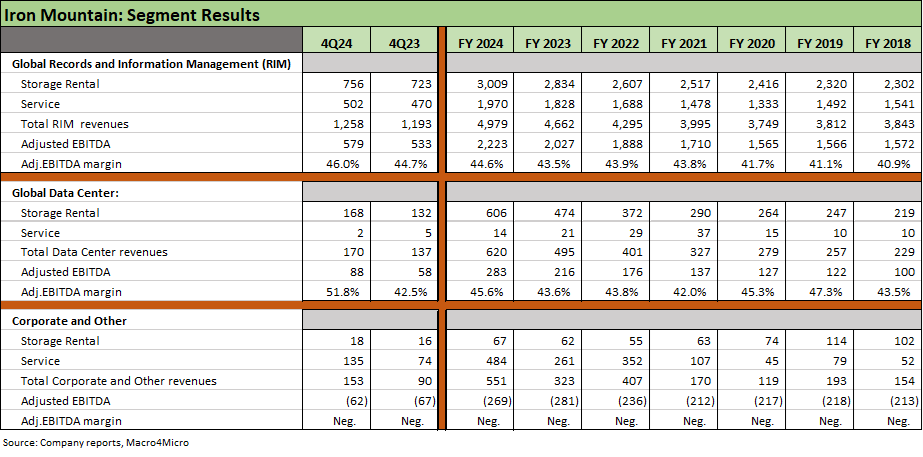

Record quarterly and annual revenue and record quarterly and full year adjusted EBITDA with higher EBITDA margins in 4Q24 and for full year were posed in both of the primary business segments, Records and Information Management (RIM) and Data Centers.

Generating strong earnings and lower leverage in the face of record growth capex is telling a very good story around credit quality and the ability of IRM to deliver on its investment strategy.

Overall storage gross margins of 70% and services gross margins of 34% support a sustained high rate of capex and a 10% quarterly dividend increase.

The stock story at Iron Mountain has been one that has not been told by enough sell side analysts. Numerous major firms have not rolled it up under their data center equity coverage team given IRM’s unusual hybrid operations. It is not a pureplay data center. In this case, that is a positive given the massive cash flow generated by its legacy business lines to fund growth in Data Centers and some other new business initiatives such as Asset Lifecycle Management housed (for now) in the Corporate segment.

The recent IRM stock selloffs are most likely a question of the valuation and the worry of “how much, how soon” as well as the bear steepener in the UST curve and how that typically flows into REITs. As detailed in the balance sheet section further down in this commentary, the soaring Enterprise Value multiple to around 20x for IRM since the “low teen” days comes even as leverage declined to multiyear lows at 5.0x. That is a lot of asset protection to lean on for bondholders.

More recently, the DeepSeek discussions have raised questions around how data center intensive the AI wave will prove to be and whether capex needs will be as enormous as expected. Those with a head start in new construction (such as IRM) are seeing some additional growth expectations built into their multiples. More activity and high capacity demand has driven revenue and margin expansion for IRM as detailed below. Meanwhile, growth capex is running at record levels.

The above chart adds more time horizons and market comps for frames of reference. We line up the comps in descending order of 1-year total returns for the benchmarks/ETFs and a selection of bellwether Data Centers (DLR, EQIX), REITS, and HY Services issuers (URI, ARMK, ADT). IRM stacks up very well for the trailing year and prior periods. The recent months have seen IRM getting reeled in after such a wildly positive run.

The consolidated income statement trends tell a story of revenue growth in both Storage Rental revenues and Services with EBITDA margins in the above chart reaching highs for the time horizon at over 36% for FY 2024 and over 38% in 4Q24. As we detail below in the segments and in the capex section, growth capex in data centers dominate the investment profile of IRM.

The segment results show revenue and EBITDA growth as well as margin expansion for 4Q24 and FY 2024. The sustained growth in Data Center revenue is an extremely important part of both the equity and credit story. RIM is still the dominant part of the business mix in revenue and earnings, but that business feeds the expansion in Data Centers.

Capex and expansion of the real estate asset base is a core part of any REIT operation. For IRM, the heavy capex in the Data Center segment serves as a critical driver of the equity valuation and reinforces confidence in the quality of asset protection and forward expectations around revenue and cash flow. The rating agencies have been standing still on this name for a very long stretch, and IRM deserves higher credit ratings.

The chart shows Data Centers comprise 80% of growth capex in 2024 and 76% of total growth + recurring capex. Growth capex as a line item was 92% of total, and that makes for a good source of credit quality support if growth capex gets dialed back over the intermediate time horizon (note: there are no signs of that yet).

For now, IRM offers a growth theme, but that is funded by a combination of a major, mature cash cow legacy business and higher debt levels that still show organic declines in leverage on higher EBITDA/EBITDAR. That is a nice combination of mature cash flow generation and growth opportunities. That combination is rare in the BB tier issuer base.

The balance sheet trend line has been materially favorable since 2019’s leverage of 5.7x. Leverage has slightly improved across the tightening cycle in 2022 to 2024 with the current 5.0x marking a low point. That 5.0x leverage frames up well vs. the Enterprise Value/Adjusted EBITDA (LTM) multiple to end 2024 at 19.9x.

As the business mix has shifted and the commitment to data center expansion is clear in the capex scale and focus, the higher EV multiple is a long way from the IRM EV multiple under its legacy business mix. The valuation of the company’s asset base and growing franchise are bullish for credit quality via any rational asset protection metric that also flows into its equity market performance.

Even if one concludes that the IRM equity has run “too far, too fast” across the AI and data center buzz, the low BB tier composite rating on the unsecured bonds seems to be lagging badly. IRM has routinely made the point that there are BBB tier data centers with similar leverage and IG ratings.

The interesting twist on the legacy business is the extraordinarily high gross margins and high free cash flow generated from the “old” business lines that feed into the growth capex of the “new” business. That is a rare combination and one that fortifies confidence of equity investors in the ability of IRM to keep up an aggressive, forward-looking investment pace.

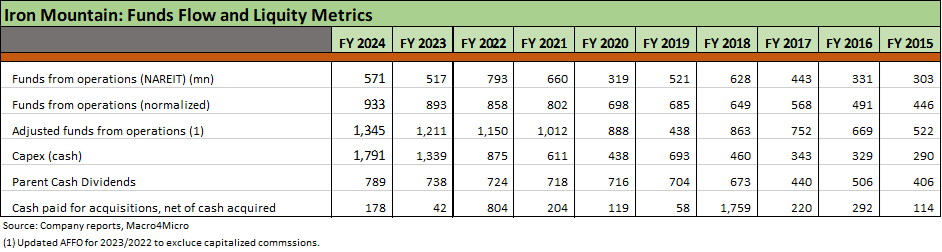

The above table updates the running funds from operations trend line that the REIT watchers value. We see record highs. Looking back over a longer timeline from 2015 (reminder: the inception of REIT status was effective Jan 1, 2014). The adjusted funds from operations has multiplied 2.5 fold.

As a REIT, dividend payouts are a priority line item. That makes for an interesting “mental twist” on how to frame the cash flows and incremental borrowing. The company runs an aggressive capex program and will continue to grow both sides of its balance sheet.

The easy way to look at a REIT such as IRM that is in rapid growth mode is that the dividend gets set around its current earnings power and then the company executes on incremental borrowing to fund higher growth capex.

REITs are income products and typically suffer when rates rise. In the case of IRM, the growth pattern has driven multiple expansion. IRM pushed through the tightening cycle based on the business mix shift and demonstrated its ability to execute and prove its business strategy.

A conversation we had long ago with an investor centered around the idea that “IRM is borrowing to pay its dividend” which of course implies financial stress. That was not the case since that was out of sequence even if that is how you would look at the cash flow lines for a typical “business services” enterprise. The dividend is set on current earnings power. Forward capex and any related borrowing are set by accretive capex programs. IRM incurs more debt to grow – and in a high margin growth business. As the years have gone by, that balance sheet growth policy has seen success demonstrated in results and certainly in IRM’s stock performance.

See also:

Credit Crib Note: Iron Mountain (IRM) 12-18-24

Iron Mountain: Good Climb, Summit Unknown 11-10-23

Iron Mountain: The Quiet Man 4-16-23

Iron Mountain: Credit Profile 4-15-23