Productivity: Takes the Edge off the 4% handle YoY ECI

Favorable productivity metrics add some more support to the inflation risk mitigation themes.

Coming on the heels of the Employment Cost Index (ECI) with its 4% handle YoY compensation increases but with a solid sequential 4Q23 trend, today’s Productivity and Cost report was favorable with a +3.2% increase (SAAR).

The productivity bump helps the inflation story somewhat in the FOMC recipe book as output per hour trumped labor cost per hour trends.

The 4% YoY headline numbers for ECI were tagged by Powell during his call as one of the more important metrics than using just the latest quarter, but the output per hour vs. unit cost numbers today goes into the positive column for the UST bulls.

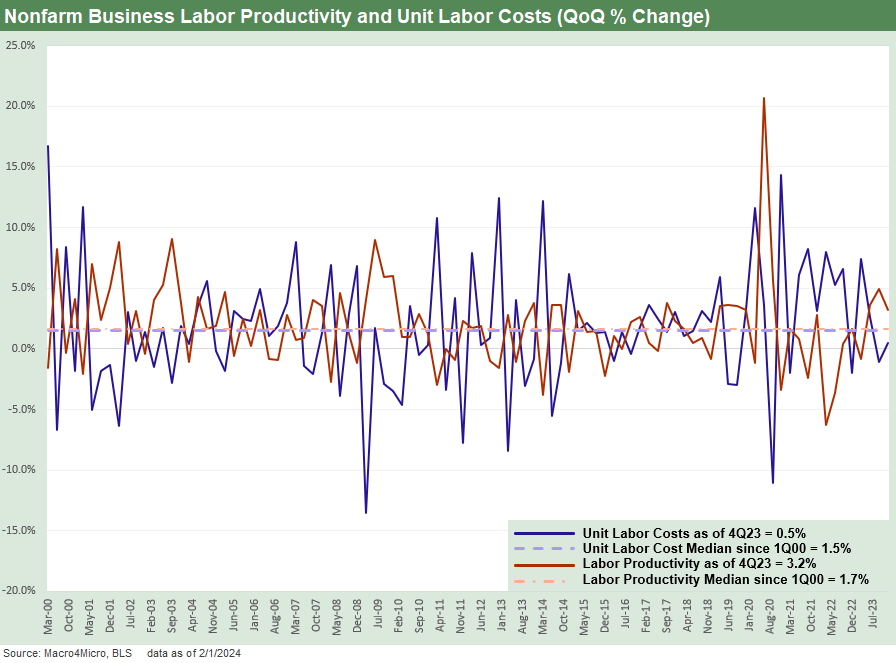

The above chart updates the labor costs and productivity metrics for 4Q23. For 4Q23, output increased by +3.7% and hours worked by +0.4%. For the full year, annual productivity for 2023 rose by +1.2%. This productivity release from the BLS shows a nonfarm business productivity increase at +3.2%, hourly compensation at +3.7%, and unit labor costs at +0.5% for the quarter.

Framing unit labor costs vs. a year ago translated into a +2.3% increase, which at least is in the right zone for a market posting lower inflation. The above chart looks at the numbers vs. the previous quarter and the chart below vs. a year ago levels.

As we cited in our ECI comments yesterday (see Employment Cost Index Dec 2023: Compensation Mixed Picture 1-31-23), something has to give when YoY compensation is rising whether that be rising productivity, contraction of profit margins, or cost pass-throughs by employers with pricing power. Higher productivity in 2023 and into 4Q23 helps flow into the lower inflation story without the fears of excessive margin risk. As you look back across time, the productivity metric comes with the asterisk of being very volatile.

On a day when ISM Manufacturing metrics improved modestly even if still below the 50 line, the news has been constructive for those framing fundamental risks along with handicapping inflation. The FOMC timeline on cuts (how soon and how many) is still the usual mindreading exercise.

|

|