Trump's “Greatest Economy in History”: Not Even Close

We can’t help but revisit the past 50+ years of annual GDP growth when we hear Trump say, “greatest economy in history.”

Trump’s tariff policy-setting toolkit…

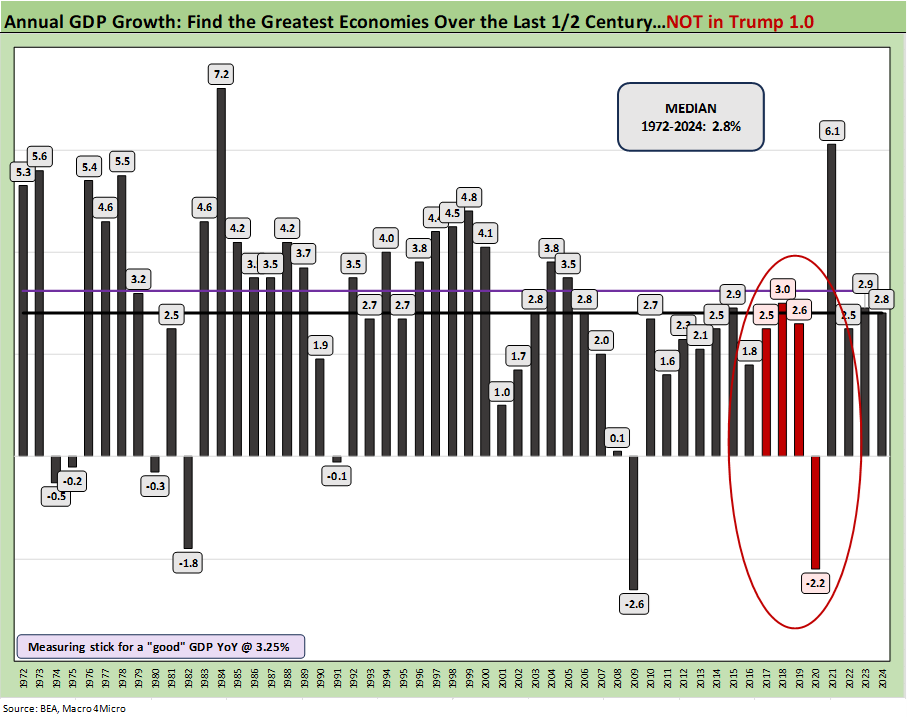

After a long speech before Congress by Trump, we look back at the annual GDP growth from Nixon/Ford through Biden and include Trump 1.0, which was once again billed as the “Greatest Economy in History”. That certainly sounds better than the truth: “Bottom quartile in the last half century.”

One of the morning shows called the Trump address to Congress a MAGA rally ChatGPT product, but software does not set records for longest speech since Clinton in 2000.

The median annual GDP growth since Nixon/Ford was +2.8%, so if we set an aspirational target of 3.25% as a bar to clear for annual GDP growth, the post-2000 years have been ugly and Trump 1.0 one of the worst. The 1970s, 1980s, and 1990s crush Trump 1.0. Fact.

When we hear that Trump 1.0 was the “greatest economy in history,” we worry that delusion and widespread ignorance combined with a basic lack of mental effort in a factual void can make “imaginary facts” real just by repetition. After all, it has worked so far. That worry ties into the false tariff story line and the Trump sales pitch that the “selling country” pays.

It is worth remembering that Trump 1.0 promised 4% GDP growth and elimination of the deficit in 8 years. Well, we can restart the game clock in 2025 and hope he does not seek to be President for Life or until he actually achieves those milestones (i.e. many terms or until a sovereign debt crisis – whichever comes first).

Even that “seller pays” nonsense is grounded in the idea that some mystical sovereign body decides what the buyer purchases. As the nonsense flies, that means transactions translate into the other sovereign nation receiving subsidies from the US. Those who actually believe that should stick with the Crayola box of 6. You are not ready for the Box of 64.

That said, the market needs to worry about policy and how disinformation on tariffs gets worked in as a tailwind for high taxes on the consumer and companies who have non-US supply chains. You can promise small and medium sized businesses tax relief if they in fact can be profitable once you have damaged them with tariffs on their expense line. Same thing goes for the relative impact on their revenue line after trade partner retaliation. The domestic supply chain competition will raise prices. Many already have just like the 2018-2019 tariff adventures.

Looking back across annual GDP growth…

We do not plan to revisit the Presidential story lines here (my first vote was in 1976), but we saw a lot of 5% GDP growth handles and 4% handles along the way as evident in the chart.

Trump had zero years above 3.0%. Biden had one. Carter had 3 years higher than Trump’s best (see Annual GDP Growth: Jimmy Carter v. Trump v. Biden…just for fun 1-6-25). We know there is more to life than GDP growth, but we easily rank that as #1. It tells a story of activity that leads to hiring, tax base growth (Government investment and consumption), and long-term investment.

We saw some wild times under Nixon and then Ford with post-Vietnam inflation and the structural challenges after the Arab Oil Embargo. The year 1974 was brutal, but it was followed by two 5% handle years and a 4% handle year.

In the case of “greatest economy,” you cannot lay claim to that title with subpar GDP growth numbers. It is like telling the diving judge “Come on, have you ever seen such a big splash. That was awesome.”

In the end, we all have to vote with our gut, and many of us come from families with split political views and MAGA vs. whoever, etc. The 1968 election was an especially colorful one around the dinner table. My Mother voting for Wallace was very Boston Irish working class at that time even if Humphrey took the state with 63% of the popular vote. Wallace was a firebrand segregationist who won 5 states in that election which are all MAGA states now (nope, not very subtle).

Voting with “your gut” is fine, and most of us do just that. However, it should not be done right after a heavy meal of utter falsehoods and outright lies. Doctors recommend waiting for half an hour before swimming in a sea of disinformation.

See also:

Payroll % Additions: Carter vs. Trump vs. Biden…just for fun 1-8-25

Annual GDP Growth: Jimmy Carter v. Trump v. Biden…just for fun 1-6-25

Presidential GDP Dance Off: Clinton vs. Trump 7-27-24

Presidential GDP Dance Off: Reagan vs. Trump 7-27-24

Totally agree. It all matters. I used GDP growth as the springboard for drilling into the lines from the consumer side to the fixed investment side and where the government fits in. Real GDP helps level the inflation issues somewhat, but PCE (including income and outlays) and CPI review line by line has to be a core activity.

I choose GDP as my favorite "equalizer" to take some of the BS out of it in the case of Trump's big mouth and adjective-heavy hype, but GDP is ground zero for radiating out into the big moving parts. If the consumer is the main driver with no balance in fixed investment, trouble is on the way and there are vulnerabilities.

The income disparity issues matter. I always think back to one of my professors in the 70s harping on "equity" in pareto optimality. I had slightly more colorful language on what that meant from my background in a working class fading industrial city! (Something about what the rich do to the poor.)

All helpful comments. We are breaking new ground in terms of the US being a high political risk environment with debt sustainability question marks. We have a President who has recommended default just last year in a CNN town hall meeting! What happens when he loses a slice of Congress? Brinkmanship on debt as a path to authoritarianism?! This is sure as hell not getting easier!

Wait until Musk and Trump start purging the economic research groups when they don't like the data that is coming out. We heard some of that from Commerce recently. Project 2025 was aiming at those econ data and analysis efforts for "like minded" staffing. "Propaganda 101 meets economics" is something worth worrying about.

Thanks for feedback.

The budget process will be a "cluster of circles."

1. Employment and Unemployment Rates Matter Too

GDP growth alone doesn’t account for the employment situation in the economy. High GDP growth could still coincide with high unemployment if the growth is not widely distributed across sectors or demographics. Conversely, low GDP growth could mask a significant drop in unemployment, which directly impacts people’s lives. Under Trump’s tenure, for example, unemployment reached historic lows before the pandemic struck, an indicator of the administration’s focus on job creation. Similarly, Biden’s economic policies, although facing challenges, have brought about the lowest unemployment rates in decades. Employment, rather than just GDP, should be a core consideration when evaluating economic success.

2. Inflation and Purchasing Power

GDP growth could be accompanied by high inflation, which diminishes the real purchasing power of consumers. If inflation rises faster than wages, even positive GDP growth might not translate into an improved standard of living for most people. Evaluating inflation alongside GDP gives a fuller picture of how economic growth impacts everyday life. The current inflationary pressures post-pandemic have presented challenges to many families, and these dynamics must be weighed when assessing the success of an economy under any administration.

3. Income Inequality and Wealth Distribution

GDP growth does not account for how wealth is distributed. A high GDP growth rate that disproportionately benefits the top 1% can obscure the fact that the majority of people aren’t seeing tangible improvements in their financial well-being. Economic success should not be evaluated in a vacuum, but in the context of how inclusive that growth is. The challenge of addressing income inequality is paramount to ensuring that economic growth benefits society as a whole, not just a select few. Policies that promote wage growth, access to quality jobs, and wealth redistribution through progressive taxation are just as important as raw GDP numbers.

4. Quality of Life and Social Metrics

Other factors such as healthcare access, education quality, housing affordability, and environmental sustainability matter significantly to a country’s long-term economic success. A nation can experience steady GDP growth while facing deteriorating infrastructure, poor health outcomes, or an unaffordable housing market. Quality of life indicators, including life expectancy, education attainment, and social mobility, provide a much richer picture of whether the economy is truly benefiting its people. Growth that is disconnected from improvements in these areas is ultimately hollow.

5. Sustainability of Growth

Sustainable economic growth, as opposed to short-term growth, is essential for ensuring that future generations inherit an economy that can continue to thrive. Economic policies that prioritize the environment, renewable energy, and long-term infrastructure investments are crucial for ensuring that growth doesn't come at the expense of future prosperity. GDP numbers alone do not speak to whether growth is happening in a way that is sustainable or beneficial for future generations.

6. A Holistic View of Economic Policy

The effectiveness of any administration’s policies must be evaluated with a more comprehensive lens. Trump’s economic policies, including tax cuts and deregulation, boosted certain sectors of the economy, but their long-term impact, particularly in terms of income inequality, environmental sustainability, and public services, requires further scrutiny. Biden’s policies, on the other hand, have focused on rebuilding after the pandemic with a heavy emphasis on infrastructure, healthcare, and climate change—issues that are equally important for the long-term health of the economy.