Equitrans and Mountain Valley Pipeline’s Wild Ride

Excerpt from Footnotes and Flashbacks: Week Ending June 4, 2023

Equitrans and MVP’s not-so excellent adventure seems to be over (in a good way) with the debt ceiling resolution.

The “Fiscal Responsibility Act of 2023” discussed earlier in the MACRO section brought substantial benefits to a notable midstream operator (ETRN), whose stock roared when the language was released. The actions to support this single important pipeline project will also have some multiplier effect benefits for a number of upstream and downstream operators with interests in seeing higher volume out of the Appalachian natural gas reserve base.

As a rule of thumb, when a new project goes into operation, the movement of natural gas and ancillary product streams continues beyond the narrow project and thus volumes (fees or commodity revenues) climb on multiple fronts depending on the mix of hydrocarbons. In this case, the relief factor is high given the billions sunk into this project and the historical constraints plaguing the major Appalachian basis.

We cut and paste the very clear and specific (and brief) language of the bill at the end of this piece. In plain language the legislation could have said, “The $6+ bn pipeline is happening, and we are taking the decision out of the hands of the regulators who have held you back and the district court where you seem to keep losing.”

The legislation’s language greenlights the approval of the Mountain Valley Pipeline (“MVP”) joint venture for the last steps. Based on management comments even before this victory, ETRN had indicated MVP would be operational in 2023. The reaction of ETRN tells the story as the week posted a +49% return and ETRN zoomed to the head of the pack in YTD total returns as we detail below.

As noted in the language, the legislation mandates that any challenges will be heard in the Fifth Circuit Court in Washington. Basically, the Fourth Circuit Court (Richmond, VA) has been cut out. Joe Manchin had even accused “the same three judges” in the Fourth Circuit of targeting the pipeline and finding problems that various regulators have not agreed with.

It may be a sign of how much of a problem the permitting process is when it takes a UST default threat to get a pipeline that was almost completed to the finish line. On a “half full” note, it is also a reminder of the value of pipelines already in/on the ground. That said, it would be very hard to conclude that the barriers to entry have been lowered, and more legislation has been floating around for a while specific to that topic.

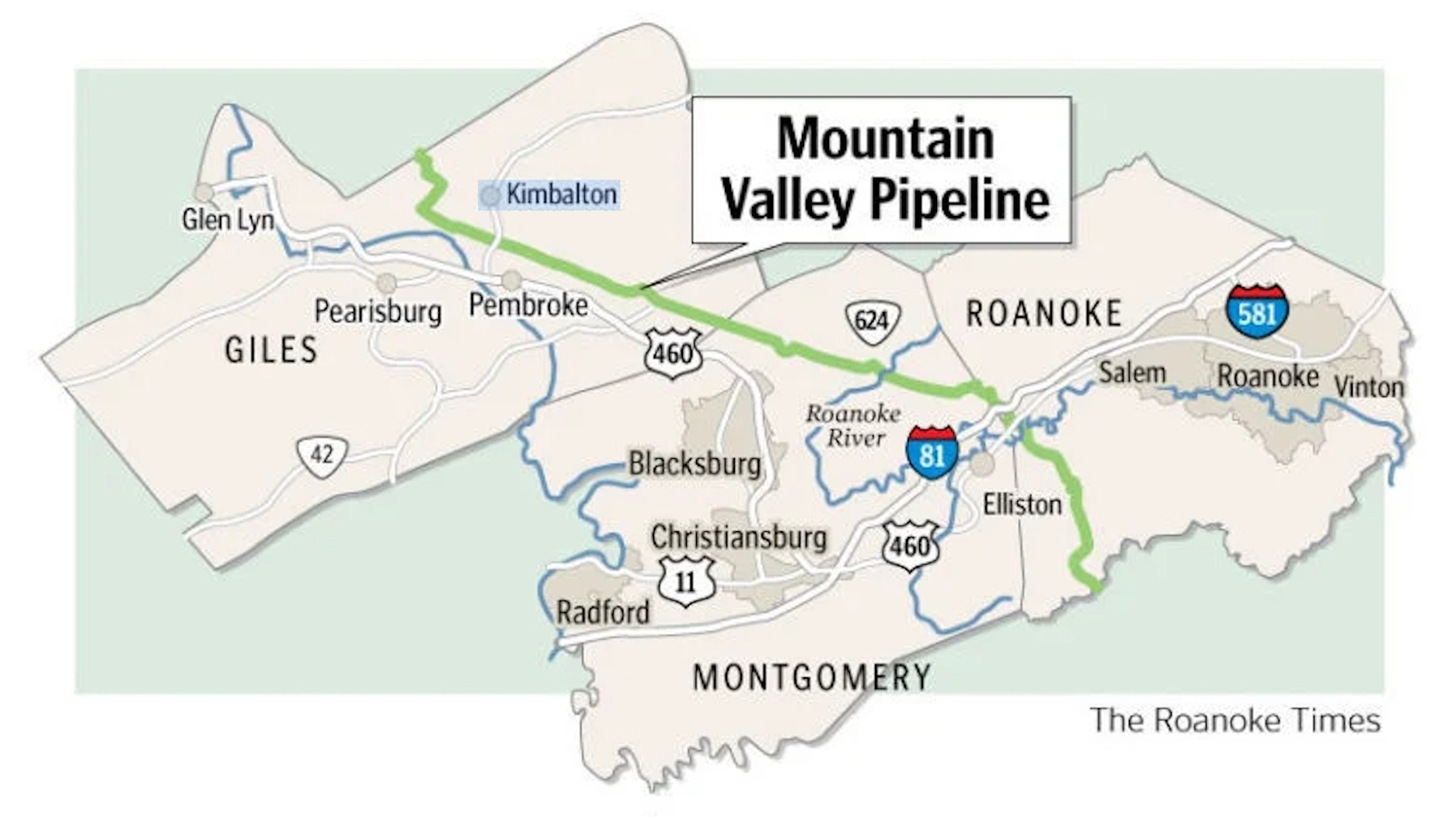

The Appalachian Basin (including the operations of EQT, ETRN’s former owner and by far largest customer) is called the “Saudi Arabia of natural gas” in some quarters, so the strained attempts to build more takeaway capacity was always a headline even beyond the trade rags. The target markets for various regional infrastructure gets tricky, but the MVP is targeting the mid-Atlantic and Southeast.

This corner of the E&P boom over the past decade has had challenges in supply-demand balances and distorted price differentials that got a lot of attention as takeaway lagged. The erratic process undermined the ability of the Marcellus and Utica shale formations to drive more organic growth in cash flow. With the area running short on takeaway capacity for select end markets, MVP became the focal point for what is wrong with the permitting system.

MVP in context…

MVP is 47% owned by ETRN and has been the poster child for problems in capex planning for major projects whether in the US or Canada with their own set of issues up north that deter capital investment. The MVP battle is not new and has ruled headlines as well as stock price action on the company as evident in the chart below.

ETRN is a major BB tier bond issuer even though it is small relative to the major BBB tier names in the space that have debt balance multiples the size of ETRN (e.g., ET, KMI, EPD). It is on the income stock list for many, but ETRN’s stock price action had been erratic around news flow. As a matter of disclosure, I had purchased ETRN stock in 2022 and traded out at a gain in 2022 after the news on MVP ebbed and flowed. It was too much guesswork on the workings of courts and Manchin’s ability to get it to the finish line.

ETRN and EQM fell into the HY index in early 2020 for a range of reasons, but the dependence on MVP for sustained organic growth in cash flow was an important variable. ETRN and its complex history needs a separate commentary, and the merger with EQM cuts across a range of entities some of which were created under the EQT umbrella prior to its spin-off of ETRN in Nov 2018.

EQT had acquired Rice Energy in 2017 with its mix of E&P and infrastructure assets. As with many infrastructure relationships (in part or in whole), there has been a lot of action across the family tree over the years. ETRN and legacy companies are like numerous other names in the space with the juggling act of C Corps, MLPs, simplifications, and what sometimes seems like three card monte with legal entities and securities. That said, the main story for some time has been about MVP, and now that has been cleared up after years of battling.

The role of a key Senate swing vote in Joe Manchin (a well-known MVP advocate) increased the visibility of the issue and chance of success. The debt ceiling process thus gave Democrats something to horse trade to avoid disaster and the GOP the chance to take credit for the MVP approval with Manchin’s Senate seat up for grabs in 2024. The Democrats had stonewalled Manchin’s ambitions until he cut a deal on the IRA in exchange for MVP support from the Dems. Then GOP Senate minority leader McConnell blocked an MVP bill as punishment for Manchin reaching that agreement on the IRA. Now the GOP and Manchin can fight over credit for the approval, but for ETRN stockholders and bondholders the news is a relief.

The above chart then puts the Equitrans rebound this week in context with its YTD leap up the ranks. The updated trailing return charts for midstream equities shows mixed performance numbers YTD for total returns vs. the overall market. Cash dividends still carry ample weight even in a market where cash returns offer sound alternatives for many portfolios who might need a placeholder as major macro variables get worked through. At least now the short UST alternative does not have a default in its future until 2025.

What the legislation says on Mountain Valley Pipeline…

We excerpt some of the Fiscal Responsibility bill language below. There is not a lot of room to misconstrue the clear intent of the law:

“Congress hereby ratifies and approves all authorizations, permits, verifications, extensions, biological opinions, incidental take statements, and any other approvals or orders issued pursuant to Federal law necessary for the construction and initial operation at full capacity of the Mountain Valley Pipeline.”

“Notwithstanding any other provision of law, no court shall have jurisdiction to review any action taken by the Secretary of the Army, the Federal Energy Regulatory Commission, the Secretary of Agriculture, the Secretary of the Interior, or a State administrative agency acting pursuant to Federal law that grants an authorization, permit, verification, biological opinion, incidental take statement, or any other approval necessary for the construction and initial operation at full capacity of the Mountain Valley Pipeline, including the issuance of any authorization, permit, extension, verification, biological opinion, incidental take statement, or other approval described in subsection (c) or (d) of this section for the Mountain Valley Pipeline, whether issued prior to, on, or subsequent to the date of enactment of this section, and including any lawsuit pending in a court as of the date of enactment of this section.”

“The United States Court of Appeals for the District of Columbia Circuit shall have original and exclusive jurisdiction over any claim alleging the invalidity of this section or that an action is beyond the scope of authority conferred by this section.”

“This section supersedes any other provision of law (including any other section of this Act or other statute, any regulation, any judicial decision, or any agency guidance) that is inconsistent with the issuance of any authorization, permit, verification, biological opinion, incidental take statement, or other approval for the Mountain Valley Pipeline.”

From our standpoint, that pretty much covers it for a massive project that can now proceed to completion.

The capex planning and permitting are still murky…

While the MVP news was a major immediate positive for a subset of the midstream and upstream markets, the broader optimism around permitting and major new energy initiatives – especially on the infrastructure side, will still need to navigate Progressive anger and the vagaries of the court system. The Democrats will need to go into damage control mode with the hard-core climate constituency in its base.

The pro-carbon vs. anti-carbon heavyweight fight is still on, and the court battles are not going away any more than the FERC or the regulatory alphabet checklist cited in the legislation. The battle sure looks like it is going away for MVP and the massive-embedded investment held by its stakeholders with ETRN right at the top. The industry experts and lawyers for the warring factions will have plenty of follow-up color to watch around what this means for other challenges.