Credit Snapshot: Taylor Morrison Home Corp (TMHC)

We summarize the credit fundamentals of Taylor Morrison Home Corp.

Credit Trend: Positive

Summary credit profile: TMHC is another builder where the credit rating agencies set the bar too high for a BBB tier rating and thus leave TMHC unsecured bonds at a high BB composite rating on its 3 index bonds. TMHC presents IG quality risk with stable mid 20% gross margins, materially lower gross homebuilding debt since 2021, inventory coverage at a multiple of total debt, and a favorably diversified profile across product tiers and by regional exposure.

TMHC is well positioned under any realistic macro scenario with solid working capital dynamics mitigating liquidity risk in a downturn as inventory liquidation promises healthy cash flow generation in a theoretical (and highly unlikely) steep downturn in volumes. TMHC has executed on a very successful expansion program since its 2013 IPO with successful M&A execution that broadened its geographic markets in both the upper and lower tier price segments (see Credit Crib Note: Taylor Morrison Home Corp (TMHC) 5-20-24).

Relative value: TMHC is a high BB composite bond issuer with favorable risk-reward symmetry vs. alternatives in the BBB and BB tier. Based on a review of recent data (7 Chord), the three TMHC 5% handle coupon bonds (5.875% of June 2027, 5.75% of Jan 2028, 5.125% of Aug 2030) trade on the tighter end of BB tier composites. Relative to that tier, we see TMHC bonds as low risk even if cyclical questions could lower the chances of the rating agencies moving more quickly to recognize the company’s investment grade caliber risk.

TMHC shows a better mix of consumer cycle risk variables than many comps in manufacturing and commodities with respect to tariff uncertainty and recession risk. The unpredictable yield curve clearly is important, but TMHC has very successfully navigated the post-COVID market, inflation pressures, and the tightening cycle with mortgage rates swinging within a 200 bps range since fall 2023. TMHC equity has materially outperformed the below-IG-rated homebuilders over the trailing 6 months and 1 year timeline and also outperformed the Homebuilder ETF (XHB).

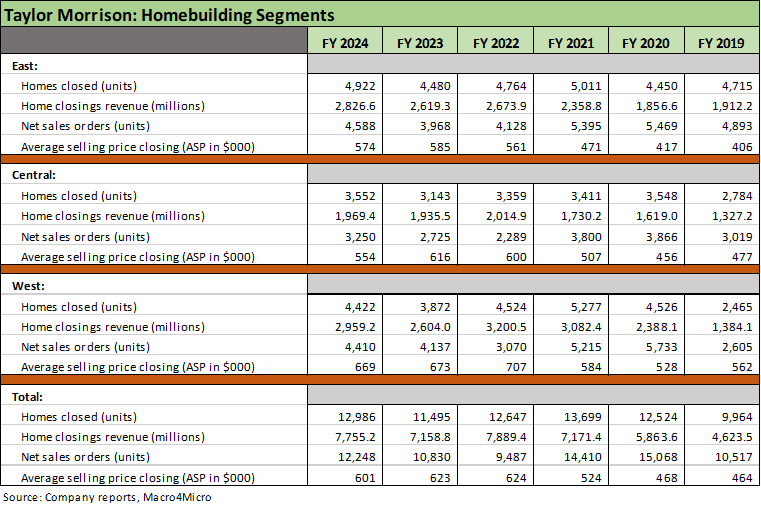

Business risk: TMHC offers a favorable product mix with Move Up product at 48% of total, Entry Level 32%, and Resort Lifestyle 20%. Before the IPO, TMHC was more of a second move-up and luxury operator. Later M&A actions and community planning broadened the mix. The mortgage squeeze has hit the lower price tiers harder, but the $601K ASP reflects a successful premium presence that has supported margin trends. The Yardly Build-to-Rent operations have been growing with TMHC ranked as the #1 national developer in this space. That business is still small in context of the consolidated TMHC.

Tariffs: The more recent threats of tariff impact on supplier chain costs and mass deportation threats to subcontractor labor cost can only be negative factors by definition. The potential for fallout on building cycle times from trade wars also cannot be ignored, but few are admitting to that yet with a focus on “working with trade partners” (code for sharing the pain). A heavy mix of sourcing from US suppliers helps ease some worries for builders, but the evolution of tariffs on lumber and copper together with high tariffs on steel and aluminum assure unit cost pressure on the building materials menu.

The world’s worst silver lining is if the trade war triggers a non-stagflation recession that could drive mortgage rates lower. Affordability would improve but consumers would struggle. That all adds up to a wider range of potential outcomes, but overall homebuilders have less exposure to the broader basket of tariff risks facing manufacturers.

Profitability: TMHC’s average selling price of $601K for FY 2024 ($608K 4Q24), 24.8% gross margins, and successful integration of its pre-COVID acquisitions (notably William Lyon, AV Homes) have improved its mix across regions and price tiers. Total closings are up 30% since 2019 and average selling prices are up 30%. The sale of two Build-to-Rent projects for over $88 mn boosted the corporate segment revenue line in FY 2024. Guidance calls for 23% to 24% gross margins in FY 2025, mid-single digit growth in closings and community count with slightly lower average prices.

Balance sheet: Balance sheet trends were sequentially weaker in FY 2024 vs. 2023 with leverage higher and inventory coverage of debt lower. However, we see material declines in gross homebuilder debt relative to the pre-2023 periods and notably since 2021. The debt % capitalization target range is 15% to 20% but expects 10% to 15% by the end of 2028. TMHC has a $1 bn revolver (undrawn, matures 3-11-27).

The rolling 3-year free cash flow of $2.1 bn (after $6 bn in land acquisition and development) was deployed to materially reduce debt and buy back shares. Since 2015, TMHC has bought back 55% of beginning shares with TMHC targeting another $300 to $350 mn in buybacks in 2025. Credit quality has improved, debt has been reduced, and shareholder enhancement was steady.

SELECT CHARTS

Solid revenue growth and higher margins across the post-COVID cycle.

Healthy regional balance and higher margin mix.

Solid growth in assets, total debt materially lower than 2020-2021.

Favorable leverage trends across the cycle, strong inventory coverage.

Health mix of buybacks and investment including rental operations.