Credit Snapshot: Ashtead Group

We summarize the credit fundamentals of Ashtead.

Credit Trend: Stable

Summary Credit Profile:

We have always been very comfortable with Ashtead credit quality since its BB tier days when it was a 2L bond issuer. Since those days, the #2 equipment leasing company continues its slow and steady rise up the credit tiers into IG with BBB3 composite credit ratings and an unsecured bond stack (only the ABL line is secured). Those credit ratings could easily be higher based on low leverage, impressive financial flexibility (notably in capex) and free cash flow generating ability, a stellar track record across multiple cycles including two crisis backdrops, and low overall business risk.

The favorable credit attributes are intertwined with intrinsic capital allocation flexibility of gross capex vs. net capex after sales of equipment and fleet management actions. The high EBITDA margins and favorable secular demand for leasing in the “lease vs. buy” decision has allowed Ashtead to grow faster than the equipment markets across the decades. The healthy free cash flow has been tested across some very extreme cyclical moves the past 25 years including a credit crisis and a pandemic. Ashtead pushed right through those cycles and kept on expanding.

The best comp for the overall credit story is industry leader United Rentals (see Credit Snapshot: United Rentals 4-1-25, Credit Crib Note: United Rentals 11-14-24) with the main differences between the two being URI’s much more aggressive, big-ticket acquisitions over the years than what was seen at Ashtead (Credit Crib Note: Ashtead Group plc 11-21-24). The distant #3 player making a push to close the gap is Herc Holdings (HRI), but HRI falls well short of Ashtead (Sunbelt) in scale and breadth of operations. HRI is materially riskier than United Rentals and Ashtead in credit quality as it makes a debt-financed push into transformative acquisitions (see Credit Snapshot: Herc Holdings 4-23-25, Credit Crib Note: Herc Rentals 12-6-24).

Relative Value:

Ashtead has 9 unsecured bonds in the BBB tier of the IG index that generally trades wide to the BBB tier industrial composite, so it has been a good credit value relative to BBB tier issuers with greater cash flow volatility and those that evidence more exposure to a high fixed cost base serving cyclical end markets. That includes autos and cap goods and multi-industry manufacturing issuers.

Ashtead presents lower business risk than companies with high commodity-based exposure (metals/mining, upstream oil and gas) and issuers that lack the demonstrated flexibility of Ashtead to make rapid adjustments during cyclical turns or a shifting macro backdrop. Numerous companies and industrial subsectors have materially lower profit margins, weaker balance sheets, and less cash flow resilience than Ashtead.

Some companies remain better known in the IG market, but Ashtead will get better name recognition as it keeps growing and changes its listing to the NYSE. Ashtead equity has returned almost 7x the S&P 500 since the start of 2006 and doubled the S&P 500 the past 10 years.

Business Risk:

We consider the business risk profile of the equipment leasing companies as low given the short lead time in fleet expansion (new equipment orders) or reduction (selling used equipment). The intrinsic cash flow resilience of the business is bolstered by some supportive attributes: broadly diversified exposure by region, location clusters generating a competitive edge in a highly fragmented industry (Ashtead cited 3600 rental companies), an extraordinarily diverse range of equipment types serving construction markets, and a wide range of industry verticals outside the core construction markets. The very broad array of individual customers minimizes counterparty risk.

Ashtead is the #2 player in an industry that demonstrated secular growth in equipment leasing vs. owning. The increasing complexity of equipment and challenges staffing personnel with the proper skill sets adds to the cost of ownership for its customers. Operational flexibility for customers is improved by leasing as equipment problems are immediately resolved and major mechanical problems quickly addressed whether equipment is replaced or repaired.

The branch geographic clustering strategy supports service quality and cross-selling strategies and especially with longer term mega projects. Equipment leasing consolidation has created an industry structure where the Big 2 (United Rentals and Ashtead) comprise over a quarter of the North American market.

Tariffs:

The primary threat from tariffs is the cost of capital goods equipment as prices could rise from material costs (steel, aluminum, copper, etc.) even if made in the US. Of course, tariffs on a wide range of equipment sold by US trading partners will also cost more to a US buyer. The blanket tariffs on entire nations and trading blocs, and the components used in manufacturing equipment could undermine demand if end market weakness and costs migrate higher.

The silver lining on equipment costs is that a potential customer might see equipment pricing as one more reason to look to leasing for their equipment needs in the “buy vs. own” decision process. That said, the tax bill offers incentives on capex with the trade-off being the use of balance sheet capacity or current cash flow that might not fit into financial planning – notably for small business lines.

The North American and US-centric operations offer some shelter from the supplier chain chaos. The UK operation is at least outside the EU trade clash risk. The more macro-based risk from tariffs is the fear of cyclical pressure on consumers and industries from tariff fallout and threats of economic contraction in fixed asset investment or stagflation that would dial back mega projects or undermine the reshoring theme. Impaired trade flows into the US for equipment also could have the effect of sustaining a robust used equipment market.

Profitability:

As highlighted in the charts below, Ashtead boasts extremely high EBITDA margins in the mid to upper 40% range for equipment rentals across the cycles. While those margins come with an asterisk for reinvestment needs to sustain the cash flow and revenue growth via replacement capex, the margins remain impressive after any historical and theoretical replacement capex. The high margins allow ample room for growth capex and shareholder enhancement from free cash flow. Ashtead has multiple pathways to sustain high margins as well as growth via bolt-on acquisitions and sustained growth capex.

The growth has been very strong across the post-COVID cycle with stimulus and a wide range of infrastructure programs and targeted project development with fiscal support (notably EVs, alternative energy) driving multiyear megaprojects with extensive equipment needs. Some projects such as power, LNG, semis, and data centers will have longer tails than others that are getting dialed back (EVs). Key drivers of secular growth include expansion of specialty equipment while general tools remain an anchor for revenue and cash flow.

We have looked at these moving parts in our commentaries on United Rentals as the industry leader along with Ashtead and Herc. Those three are expected to control as much as 50% of the market in the future. The lead players have also cited pricing and fleet size discipline as a strength. The nonresidential real estate and industrial verticals are extensively covered on conference calls and the same for construction market macro data, but the growth is tailing off as we saw in 4Q25 and FY 2025 capex guidance for spending in FY 2026.

Revenue and profitability are steady, but the next leg up in revenues awaits clarity on the pace of some fading mega projects (e.g. EVs) and to what extent those are offset in other major categories (data centers, government infrastructure, reshoring and onshoring). Bolt-on acquisitions are the more obvious path to growth if organic growth slows down.

Balance Sheet:

The basic realities of high EBITDA margins and steadily growing revenue is that the growth allows Ashtead (like URI) to keep growing both sides of its balance sheet while keeping leverage very low on an historical basis and relative to EV multiple valuations. That is a very attractive luxury for bondholders and shareholders alike in preserving credit quality while rewarding shareholders.

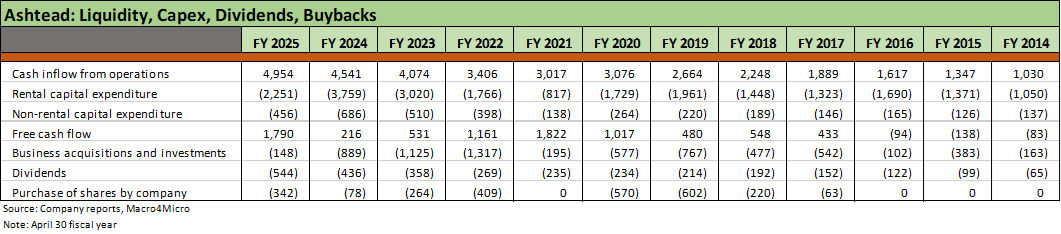

The high EBITDA run rates, high margins, and healthy free cash flow also allow Ashtead to shift capital allocation strategies over to bolt-on acquisitions and buybacks when less growth capex is more appropriate. Tapping the brakes is where Ashtead is now as fiscal 2026 unfolds. Typically, with Ashtead and United Rentals we see redeployments of discretionary cash flow in such markets to share buybacks and tactical acquisitions. We saw that in 2020-2021 as detailed in the charts. Then the post-COVID boom kicked in and the array of “mega projects” drove soaring rental capex in FY 2023 (note: FY 2023 with April 30 FY is mostly calendar 2022) and FY 2024.

SELECT TABLES

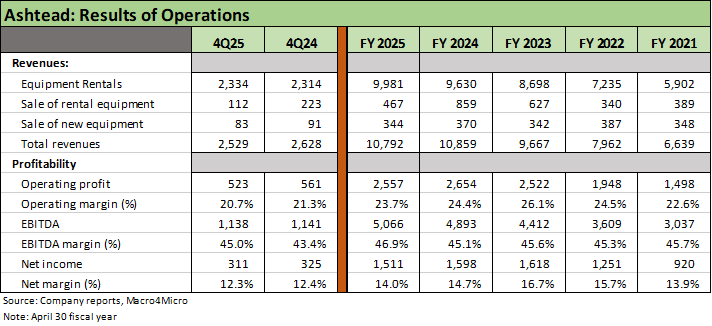

Rental revenue in a temporary plateau, margins steady.

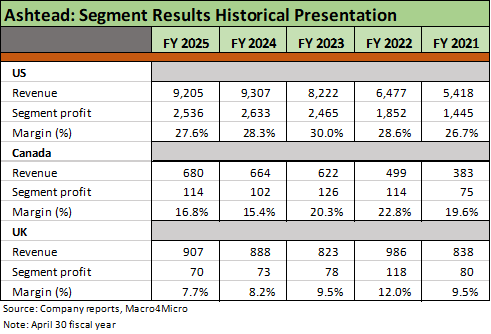

Historical segment format shows growth, segment margins down from peak.

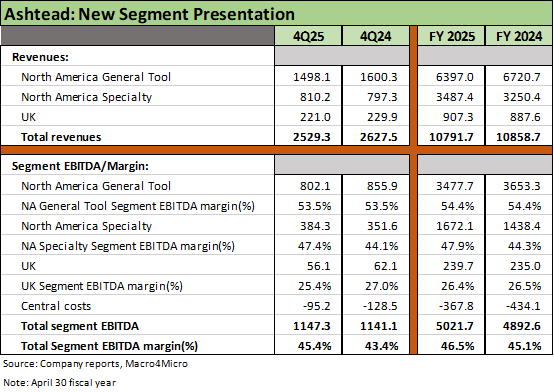

New segment format adopted in 2025 reflects equipment categories.

Capex planning and free cash flow drive shareholder rewards as swing factor.

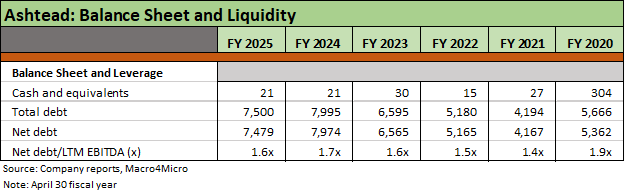

Very strong balance relative to free cash flow, capex flex, and EV multiples.